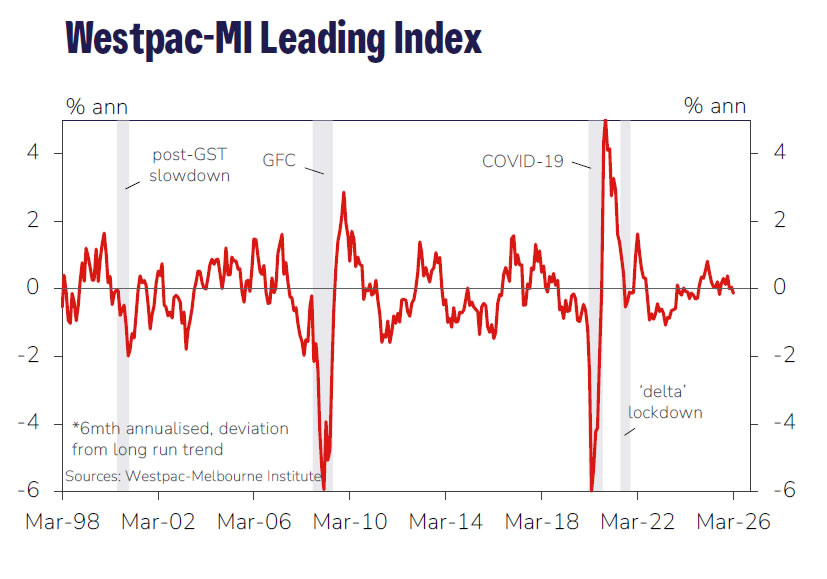

Australia’s Westpac Leading Index slipped from 0.05% to -0.13% in March, signaling a shift to below-trend growth for the remainder of 2026. The reading marks the first negative signal since August last year, indicating that momentum is softening, though not yet deteriorating sharply.

The weakness reflects a combination of domestic and external pressures. Consumer expectations have fallen sharply, equity markets declined in March, and the yield curve has flattened as short-term rates moved higher. According to Westpac, around 60% of the recent drag can be linked to the Middle East conflict, which has weighed on sentiment and driven higher fuel costs.

Despite the softer growth outlook, RBA’s policy focus remains firmly on inflation. Rising energy prices are expected to push underlying inflation higher, increasing the risk of elevated inflation expectations. As a result, the RBA is still expected by Westpac to raise rates by 25bps at its May meeting, with further tightening likely as policymakers prioritize price stability over modest growth concerns.

{kind=link}