Markets are broadly steady today as traders hold back from taking directional positions, waiting for clarity on whether a second round of US–Iran talks will take place in Islamabad before the April 22 ceasefire deadline. Despite rising geopolitical tension, price action across assets suggests a clear lack of conviction.

The ceasefire is visibly fraying, with multiple escalations in recent days, yet markets are not reacting decisively. The key reason is simple: there is still no confirmation on whether talks will proceed. Until there is a definitive “go” or “no-go” signal, the situation remains unresolved from a trading perspective.

This leaves markets stuck in a holding pattern. Dollar strength seen earlier on geopolitical headlines has faded without follow-through, reflecting hesitation rather than conviction. Traders are unwilling to chase moves that could quickly reverse depending on diplomatic developments.

Equities tell a similar story. Major European indices are trading lower and US futures are in the red, but losses remain limited. The absence of aggressive selling suggests that investors are adjusting to rising risks, rather than pricing in a full escalation scenario.

Oil remains the clearest signal—and it is not confirming escalation. Prices jumped as the “peace trade” receded, but remain below the critical $100 level. As long as that threshold holds, markets are reluctant to shift into full risk-off positioning.

In currency markets, positioning reflects caution rather than conviction. Swiss Franc leads gains, followed by Dollar, while risk-sensitive currencies like Aussie and Kiwi lag. The distribution suggests a mild defensive bias, but not a full shift into risk aversion.

While geopolitics dominates the immediate outlook, a second catalyst is approaching from the policy side. Kevin Warsh is set to appear before the Senate Banking Committee on April 21 for his nomination hearing to become the next Federal Reserve Chair, succeeding Jerome Powell when his term ends on May 15. The timing is tight, and the process is far from straightforward.

Warsh is widely seen as a credible candidate with deep ties to financial markets and the Republican establishment. However, his confirmation path is complicated by political dynamics that go beyond standard nomination procedures. The Senate Banking Committee remains narrowly divided, meaning even a single Republican defection could derail the process.

The most immediate obstacle is Thom Tillis, who has publicly stated he will block any Federal Reserve nominations until the Department of Justice investigation into Powell is dropped. In a 13–11 committee split, Tillis effectively holds a deciding vote. Without his support, Warsh’s nomination may not even reach the full Senate floor.

On the other side, Democrats led by Elizabeth Warren have called for a delay in the hearing, arguing it is inappropriate to confirm a successor while the sitting Chair is under active investigation. Combined with earlier procedural delays, the risk is that the confirmation timeline slips dangerously close to Powell’s May 15 exit, raising the prospect of leadership uncertainty at the Fed—an issue that markets are not yet pricing, but cannot ignore for long.

For now, markets are waiting. Without confirmation on US–Iran talks, there is little incentive to commit. But if geopolitical signals remain inconclusive, attention may quickly shift toward policy uncertainty as the next driver.

Canada Inflation Jumps to 2.4% yoy in March, Gasoline Prices Up Record 21.2% mom

Canada inflation jumped to 2.4% in March as gasoline prices surged a record 21.2% on the month. The spike highlights how energy shocks are pushing headline inflation higher—even as underlying pressures remain more contained. Read More.

NZD/USD Eyes CPI as RBNZ Assess Pre-Shock Inflation Pressures

NZ CPI may show cooling inflation—but the real question is whether it was already sticky before the oil shock. With core inflation in focus, the data could shift RBNZ rate expectations and drive the next move in NZD/USD. Read More.

China Holds LPR Steady for 11th Month, Signals Stability Amid Global Risks

China kept its benchmark lending rates unchanged for an 11th straight month, reinforcing a cautious stance as policymakers balance growth support against rising global risks. With the PBoC signaling a “moderately loose” policy bias but prioritizing currency stability, markets are watching how Beijing navigates geopolitical and trade tensions. Read More.

New Zealand Posts NZD 698M Trade Surplus as China, Australia Drive Export Growth

New Zealand’s trade surplus held at NZD 698M in March as exports climbed on strong demand from China and Australia, but a faster surge in imports signals rising domestic demand and cost pressures. Read More.

Gold Drops as Ceasefire Cracks, But Oil Says Markets Aren’t Pricing War Yet

Gold drops as US–Iran ceasefire cracks, but oil below $100 signals markets aren’t pricing war. Fading momentum leaves gold vulnerable to a deeper move toward the 4,000 level if tension turns into conflicts. Read More.

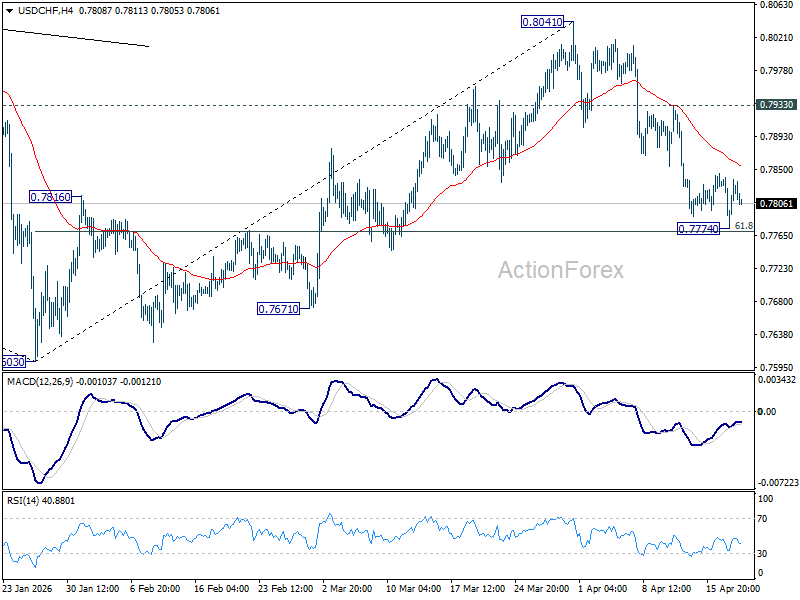

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7780; (P) 0.7811; (R1) 0.7847; More….

USD/CHF is staying consolidations above 0.7774 temporary low and intraday bias remains neutral. Upside of recovery should be limited below 0.7933 resistance to bring another fall. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low.

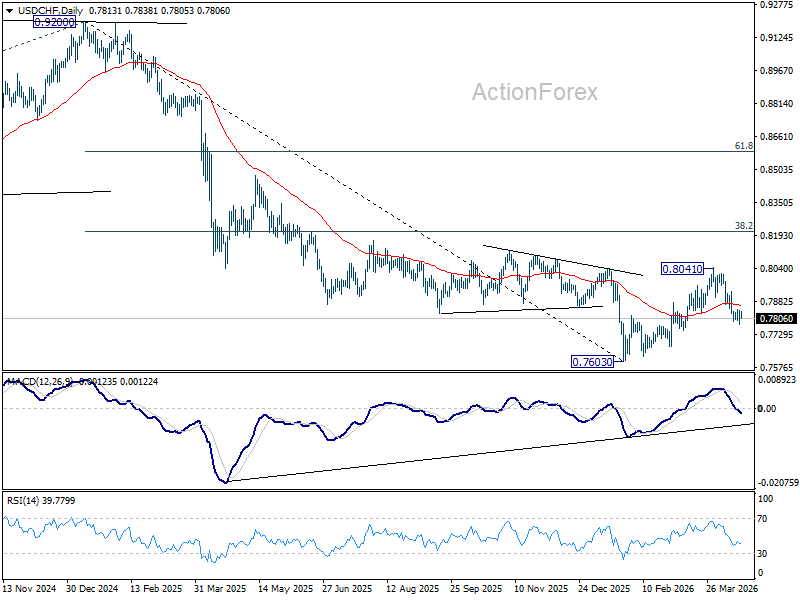

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high).

{kind=link}