New Zealand inflation data will be a major focus in the upcoming Asian session. Q1 CPI may show modest cooling, but the real question is whether inflation was already sticky before the oil shock hit. With the Iran conflict only beginning to impact energy prices late in the quarter, Q1 data will offer a relatively clean read on underlying inflation dynamics before the full effect of recent supply shocks.

Forecasts are narrowly split. Headline CPI is expected to ease from 3.1% yoy to around 2.9–3.1% yoy, but that range masks uncertainty beneath the surface. Markets are less focused on the headline print and more on non-tradables inflation, which captures domestic price pressures tied to wages and services.

This is where the policy implications become more significant. The Reserve Bank of New Zealand has already shifted toward a more cautious, hawkish stance, signaling it will “look through” direct fuel price impacts but not tolerate “second-round effects”. If underlying inflation is already proving sticky in Q1, it would raise the risk that the upcoming energy shock feeds more aggressively into broader pricing.

“Q1 is signal, Q2 is confirmation.” That framework is central to how markets are approaching this release. Q1 sets the baseline for underlying inflation, while Q2 will reveal how much of the energy-driven price pressure is transmitted through the economy. A firm Q1 print would therefore amplify concerns about inflation persistence rather than alleviate them.

If non-tradables inflation remains elevated, the RBNZ may be pushed closer to resuming tightening, potentially bringing forward expectations for a rate hike in Q3. Even without a headline surprise, underlying stickiness would be enough to shift the policy outlook.

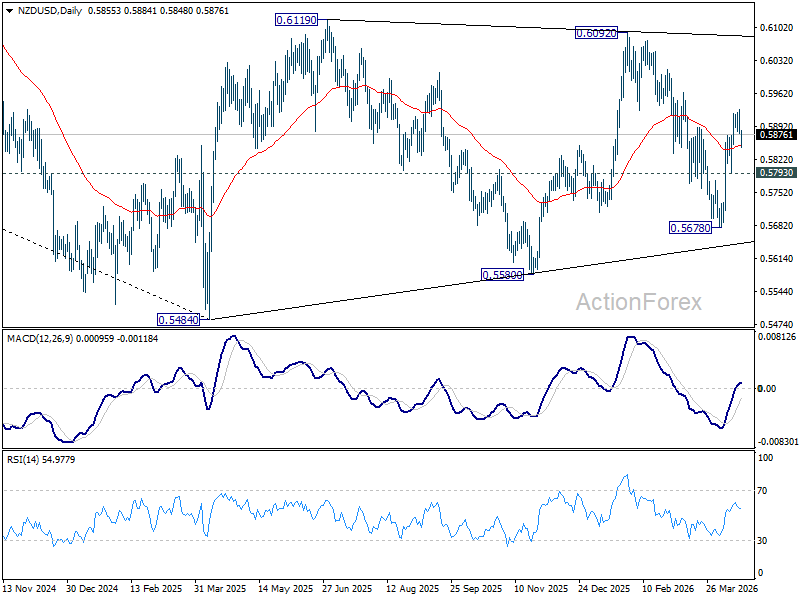

For NZD/USD, the rebound from 0.5678 suggests the prior decline from 0.6092 has completed in the near term. Yet, the broader structure remains one of consolidation (from 0.5484) within a larger downtrend. While gains may extend as long as 0.5793 holds, resistance at 0.6092–0.6119 is likely to cap upside.

On the downside, break of 0.5793 will bring deeper fall to 0.5678 support first. Further break there will argue that the down trend from 0.7463 (2021 high) is ready to resume through 0.5484 (2025 low).

{kind=link}