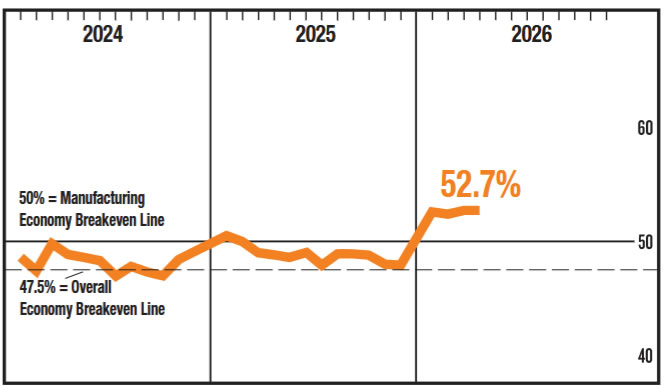

US ISM Manufacturing PMI held steady at 52.7 in April, signaling continued expansion in the sector and broadly aligning with a moderate growth outlook. Based on historical relationships, the reading corresponds to around 1.8% annualized GDP growth, suggesting that manufacturing is still contributing positively to overall economic activity.

Beneath the headline, the details were mixed. New orders improved from 53.5 to 54.1, indicating firm demand conditions, while production eased from 55.1 to 53.4, pointing to some moderation in output momentum. The labor market remains a weak spot, with the employment index falling further from 48.7 to 46.4, highlighting ongoing softness in hiring within the sector.

The most notable development was the sharp rise in price pressures. The Prices Index surged from 78.3 to 84.6, extending a three-month increase of 25.6 points and reaching its highest level since April 2022. This reflects intensifying cost pressures, driven in part by supply disruptions and higher energy prices linked to the ongoing Middle East conflict.

Sentiment among manufacturers remains cautious. During the second month of the Iran War, 69% of comments were negative compared to 31% positive, with nearly half referencing the conflict and others highlighting tariffs.

| Indicator | March | April | Change |

|---|---|---|---|

| PMI | 52.7 | 52.7 | — |

| New Orders | 53.5 | 54.1 | ↑ +0.6 |

| Production | 55.1 | 53.4 | ↓ -1.7 |

| Employment | 48.7 | 46.4 | ↓ -2.3 |

| Prices | 78.3 | 84.6 | ↑ +6.3 |

{kind=link}