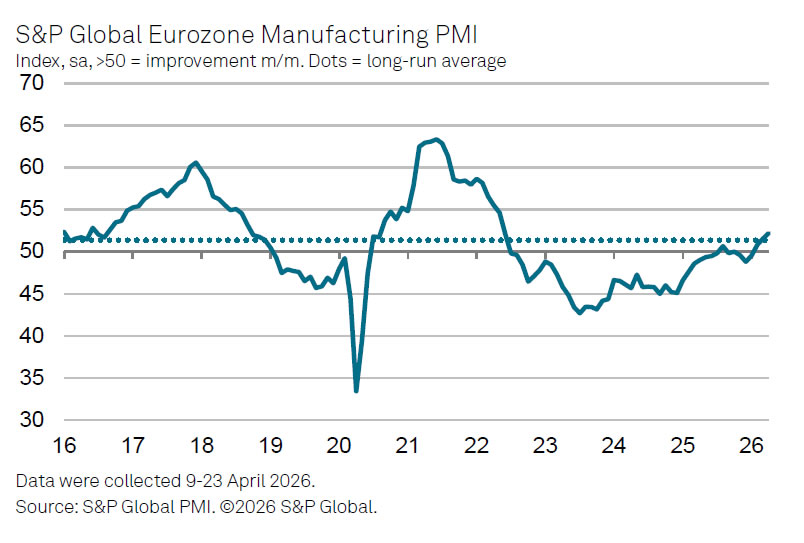

Eurozone Manufacturing PMI was finalized at 52.2 in April, rising from March’s 51.6 and marking a 47-month high, signaling a broad-based expansion across the bloc. Notably, all eight countries covered in the survey registered readings above the 50 threshold for the first time since June 2022.

The improvement was also reflected in output, with the Manufacturing PMI Output Index climbing from 52.0 to 52.3, an eight-month high. However, the underlying drivers of this growth raise concerns. Survey evidence suggests that production and new orders are being supported by precautionary stockpiling, as firms build inventories amid fears of supply disruptions linked to the Middle East conflict.

At the same time, inflation pressures are intensifying sharply. Input price inflation surged to its highest level in nearly four years, with firms passing on these costs at the fastest pace since January 2023. The scale of the increase is historically significant, with selling price inflation recording its strongest jump since the survey began in 1997, highlighting the severity of the cost shock.

According to S&P Global’s Chris Williamson, the data present a troubling mix for policymakers. While headline PMI figures appear robust, forward-looking indicators show deteriorating confidence, with future output expectations falling to a one-and-a-half-year low. The combination of slowing demand outlook and escalating cost pressures suggests that current growth may prove short-lived.

{kind=link}