Dollar is starting the week on a soft footing, and even a strong US non-farm payroll report this week may not be enough to reverse that trend. Markets are increasingly positioned around a counterintuitive dynamic where solid economic data supports risk appetite rather than the greenback, limiting the traditional upside response.

Last week’s weakness in Dollar was driven by a confluence of factors, including firm risk sentiment, expectations that other major central banks may tighten further, and a temporary surge in Yen strength linked to suspected intervention. The impact of Yen is likely to fade unless Dollar attempts another push toward the 160 level during Japan’s Golden Week holidays.

Geopolitical tensions, while still present, have taken a back seat for now. The focus is turning firmly toward risk markets and monetary policy expectations, both of which are set to be heavily influenced by this week’s April NFP report.

The key question for markets is whether March’s strong payroll gain was an outlier or the beginning of a renewed growth in hiring. Any downward revision to prior data, alongside developments in wage growth and unemployment, will be closely scrutinized for signals on underlying labor market momentum.

However, even a strong NFP print may not deliver sustained support to the Dollar. Solid job growth would reinforce the view that the Fed will remain on hold, delaying rate cuts further. But with inflation risks still tied to external factors like energy, a stronger labor market alone is unlikely to shift expectations toward renewed tightening.

Instead, stronger data could reinforce risk-on sentiment, particularly in equities, as it signals resilience in growth despite elevated rates and geopolitical uncertainty. In that scenario, capital may continue to flow into higher-yielding and risk-sensitive assets, limiting upside for the Dollar.

This dynamic creates a clear asymmetry in Dollar reaction. Markets are currently biased to sell the greenback, meaning that weak data is likely to trigger a sharper downside move than any upside generated by strong data. The reaction function is no longer balanced.

A downside surprise in payrolls, or a rise in the unemployment rate toward the 4.4%–4.5% range, would likely accelerate Dollar losses. In such a scenario, markets could quickly shift toward concerns that the Fed is behind the curve, raising fears of a harder economic landing and prompting broad USD selling.

Conversely, a strong NFP outcome may simply reinforce the current equilibrium: no cuts, but no hikes either. That outcome would support risk sentiment rather than the Dollar itself, leaving USD gains limited and potentially short-lived.

For now, the Dollar is stuck in a “heads you win, tails I lose” setup. Weak data undermines confidence and drives selling, while strong data fuels risk appetite that diverts flows away from the greenback. Unless there is a major shift in geopolitics or Fed signaling, this asymmetric risk profile is likely to keep Dollar under pressure in the near term.

For the day so far, Dollar is currently the worst performer, followed by Aussie, and then Loonie. Kiwi the strongest, followed by Yen, and then Swiss Franc. Euro and Sterling are positioning in the middle.

Bitcoin Tests $80K as ETF Flows, Options Expiry, and Supply Wall Collide

Bitcoin’s rally is hitting a decisive moment at $80K, where ETF demand, options positioning, and a major supply wall are all converging. While Nasdaq-driven liquidity is pushing prices higher, fading ETF inflows and heavy derivatives resistance could cap gains. A clean breakout would open the path toward $85K, but failure risks a deeper pullback. Read More.

Fed’s Kashkari, Hammack and Logan Reject Easing Bias, Say Next Move Could Be Hike or Cut

Three Fed officials are pushing back against expectations of further rate cuts, warning that policy is no longer on a one-way path. Dissenters at last week’s FOMC meeting argue the next move could be either a hike or a cut as inflation risks from geopolitical tensions rise. The shift signals growing uncertainty and could force markets to reprice Fed expectations. Read More.

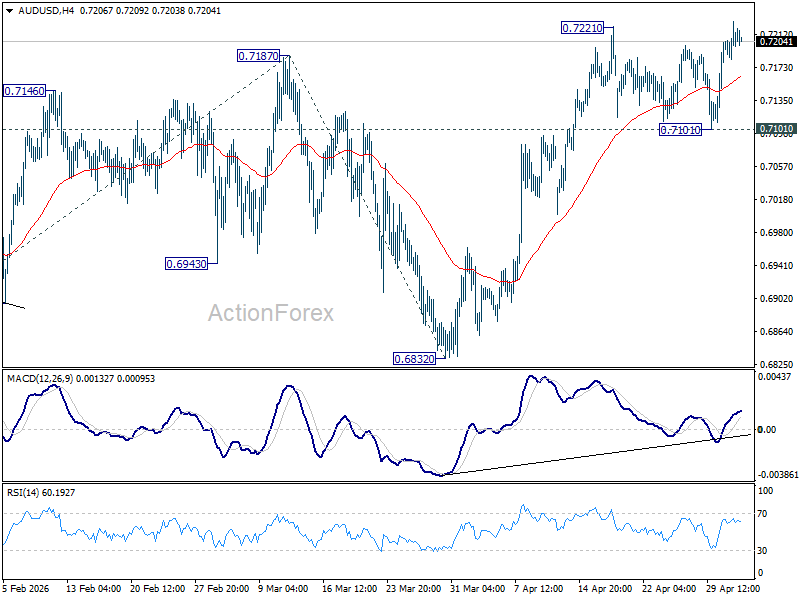

AUD/USD Daily Report

Daily Pivots: (S1) 0.7180; (P) 0.7204; (R1) 0.7225; More…

Intraday bias in AUD/USD remains mildly on the upside for the moment. Recent up trend should be resuming for 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. Outlook will now remain bullish as long as 0.7101 support holds, in case of retreat.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

{kind=link}