Dollar remains firmly on the defensive as markets head into the US session, with selling pressure picking up once again. Despite a busy geopolitical backdrop, the greenback is being weighed down by a strong risk-on environment that continues to dominate market thinking.

April delivered a powerful signal for equities. US stock markets closed the month on a strong note, with even the underperforming DOW registering its best performance since November 2024. A robust earnings season has reinforced the narrative that corporate profits remain resilient, helping to sustain the rally into May.

Crucially, investors are showing a growing willingness to ignore geopolitical risks. The ongoing tensions surrounding the Iran conflict have done little to dent sentiment, as markets focus instead on growth prospects and the durability of the tech-driven expansion story.

The political backdrop remains complex, however. US President Donald Trump is facing a key 60-day deadline under the War Powers Resolution related to the Iran conflict. While the timeline technically expires today, the administration has argued that a ceasefire reached in early April effectively ended hostilities, removing the need for further Congressional approval.

Officials have emphasized that the lack of direct military engagement since April 7 means the legal framework no longer applies. While this interpretation leaves room for prolonged tension, markets are treating it as a sign that escalation risks are contained for now.

Oil markets reflect that view. Brent crude, while still elevated, has retreated toward $115, suggesting that traders are not positioning for a near-term escalation. The easing in oil prices has also reduced one of the key pillars of recent Dollar strength, contributing to the currency’s ongoing weakness.

In FX markets, the divergence is clear. Yen remains the standout performer, supported by intervention dynamics and a sharp reversal in positioning. Loonie is holding firm on oil support, while Aussie benefits from improving risk sentiment.

Dollar, by contrast, is lagging across the board, with Euro and Kiwi also underperforming. Sterling and Swiss Franc are sitting in the middle of the pack, reflecting a more mixed set of influences.

UK Manufacturing PMI Finalized at Near Four-Year High, but Cost Pressures Surge

UK manufacturing is rebounding—but rising costs are a warning sign. Supply disruptions are pushing inflation pressures higher. Read More

Tokyo Inflation Cools to Multi-Year Low, but Energy Risks Point to Rebound Ahead

Tokyo inflation is cooling—but not for long. Subsidies are masking price pressures as energy costs threaten a rebound. Read More.

Japan Manufacturing PMI Jumps to 55.1, but Supply Strains Raise Sustainability Concerns

Japan’s factory sector is booming—but cracks are forming. Supply delays and rising costs could quickly reverse the gains. Read More.

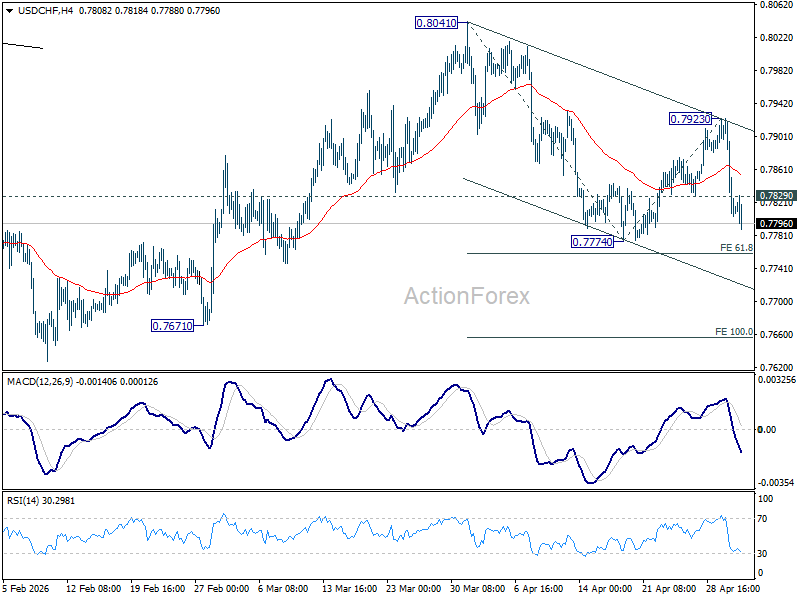

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7773; (P) 0.7848; (R1) 0.7891; More….

Intraday bias in USD/CHF remains on the downside for 0.7774 and then 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758. Firm break there will target 100% projection at 0.7656. On the upside, above 0.7829 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.7923 resistance holds, in case of recovery.

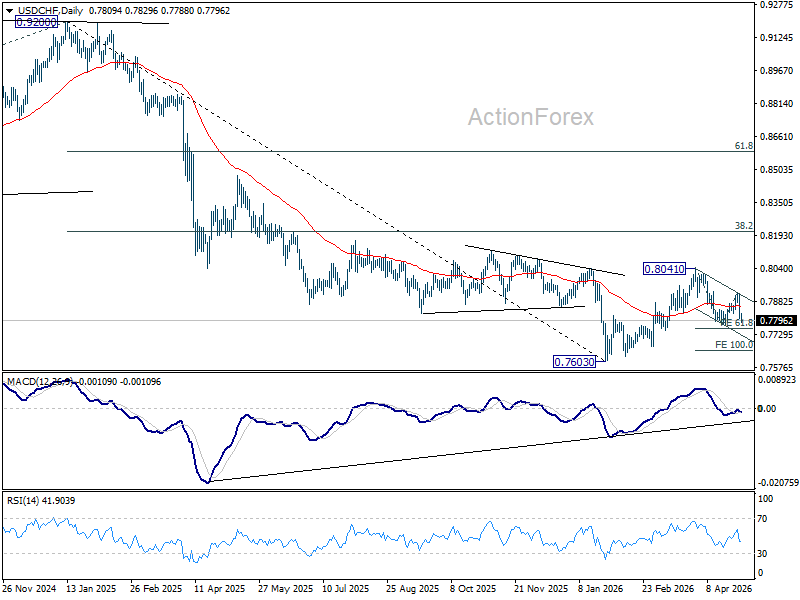

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8053) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high).

{kind=link}