US Dollar

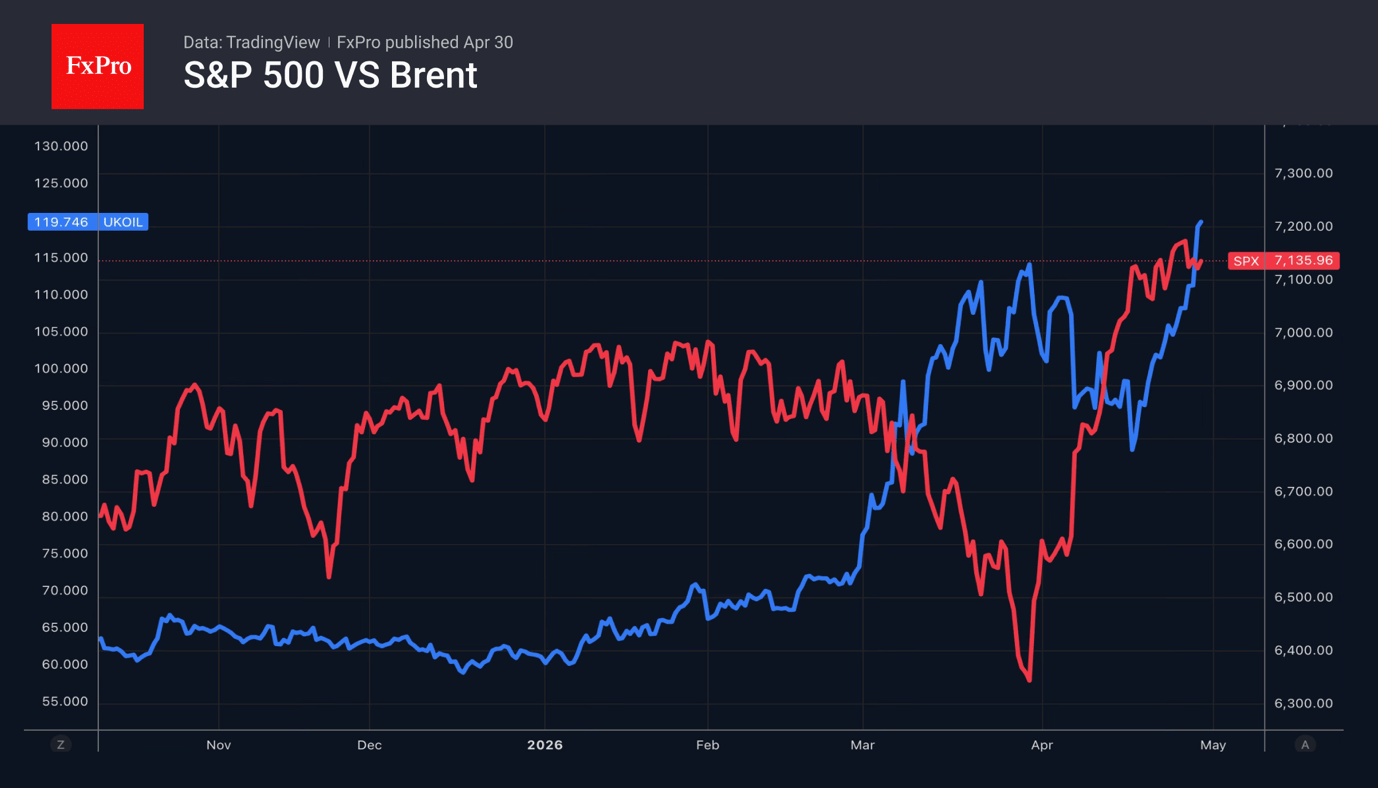

The US dollar has received positive news from the Fed, the oil market and the US economy. Jerome Powell is staying in the FOMC, Brent crude has surpassed $120 per barrel, and orders for durable goods excluding aircraft and military equipment jumped by 3.3% in March. This was the best reading for the leading indicator in the last six years.

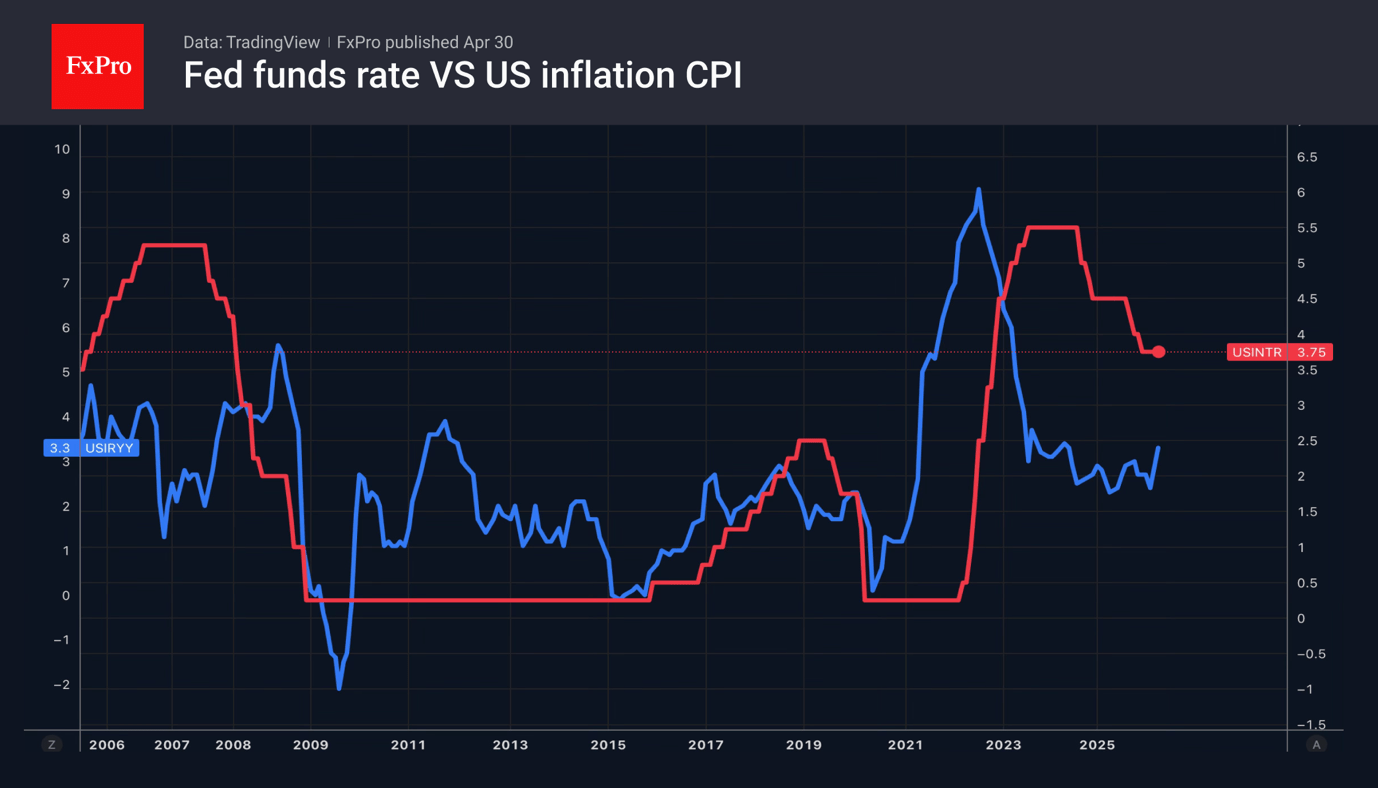

Powell believes that the US labour market is stabilising, while inflation is set to accelerate due to the conflict in the Middle East. This combination provides a strong case for a rate hike. The futures market has raised the odds of such an outcome in 2026, playing into the hands of EURUSD bears.

He also says he will remain at the Fed as Governor, with Kevin Warsh taking over as Chairman. Powell is prepared to defend the Fed’s independence, which has been threatened by the White House, undermining investor confidence in the US dollar and contributing to its decline. The task facing Kevin Warsh, recently appointed by Congress to reform the Federal Reserve, is becoming more complicated.

Stock indices

US stock indices continue to ignore geopolitics. Had someone said at the start of the conflict in the Middle East that the Strait of Hormuz would be closed until the end of April, there would have been no shortage of bearish forecasts for shares. Currently, Polymarket puts the odds at 52% that the world’s main oil artery will remain blocked until the end of June, while the S&P 500 is trading near its record highs.

Investors believe that a recession may not materialise, but they cannot afford to miss out on a strong corporate earnings season. From March lows, the Magnificent Seven has risen by 21% on expectations of higher first- and second-quarter profits. The earnings-per-share forecast for the information technology sector stands at 41%, double that of the materials sector, which ranks second.

Investors are once again captivated by artificial intelligence. However, the same fears that were present in the market before the conflict resurface from time to time. For instance, news that OpenAI had failed to meet its profit and user growth forecasts led to the share prices of related companies plummeting. Investors feared that the colossal investments in AI would fail to generate decent financial returns.

Gold

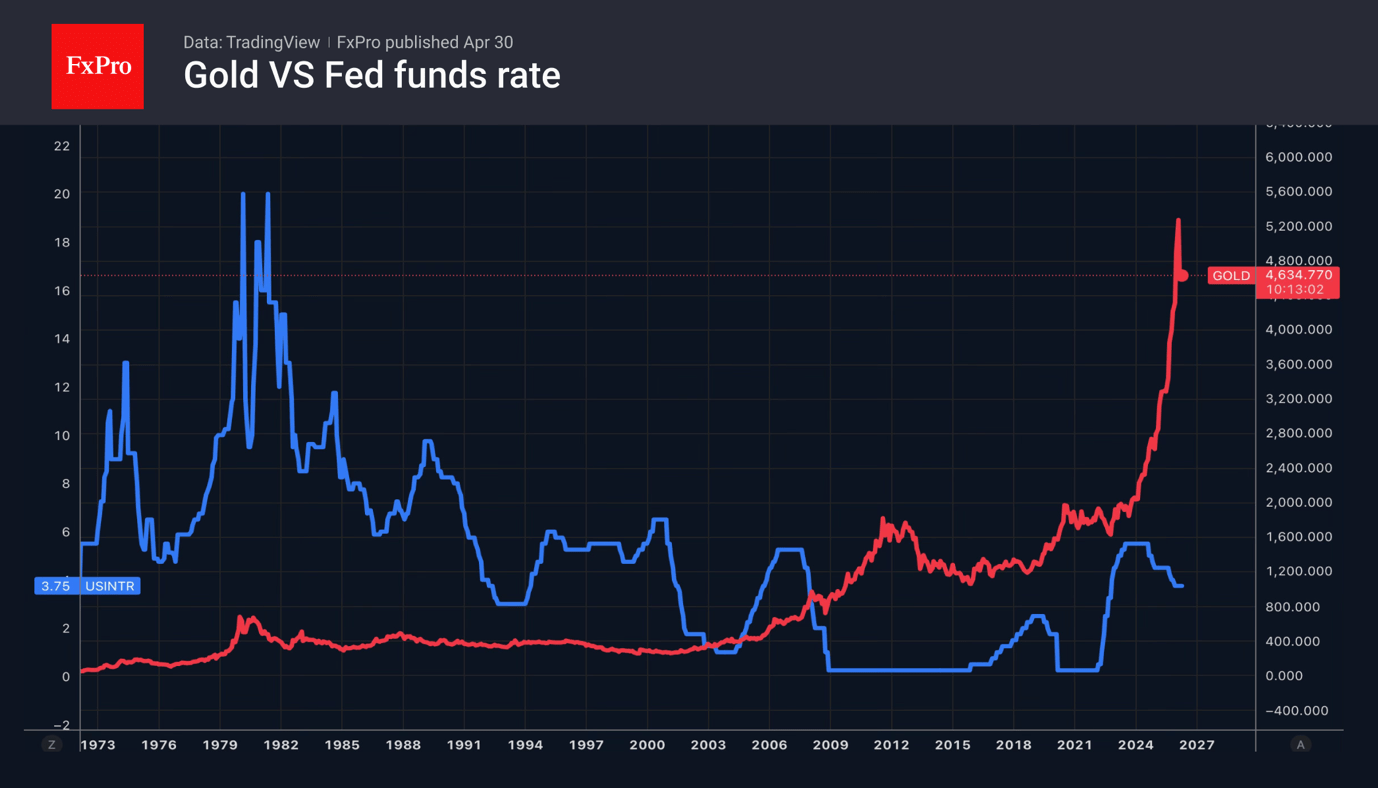

Soaring oil prices, the sharpest rise in 2-year Treasury yields since the April 2022 FOMC meeting, and a strengthening US dollar are forcing gold to retreat. The precious metal is concerned about the threat of central banks, led by the Fed, keeping rates high for an extended period, and the growing risks of further hikes amid rising inflationary pressures against the backdrop of the Middle East conflict.

Jerome Powell maintains that the US labour market is gradually stabilising, while inflation risks rising further due to geopolitical factors. Three of his FOMC colleagues dissented, arguing that rates are more likely to fall than rise. The result was a rally in Treasury bond yields and a strengthening of the US dollar. A combination that creates headwinds for Gold.

Gold might have fallen even further had it not been for renewed central bank interest in bullion. According to the World Gold Council, their purchases rose from 208 tonnes to 240 tonnes in the first quarter. Poland, Uzbekistan and China were particularly active. In contrast, Turkey, Russia and Azerbaijan became net sellers.

Cryptocurrency

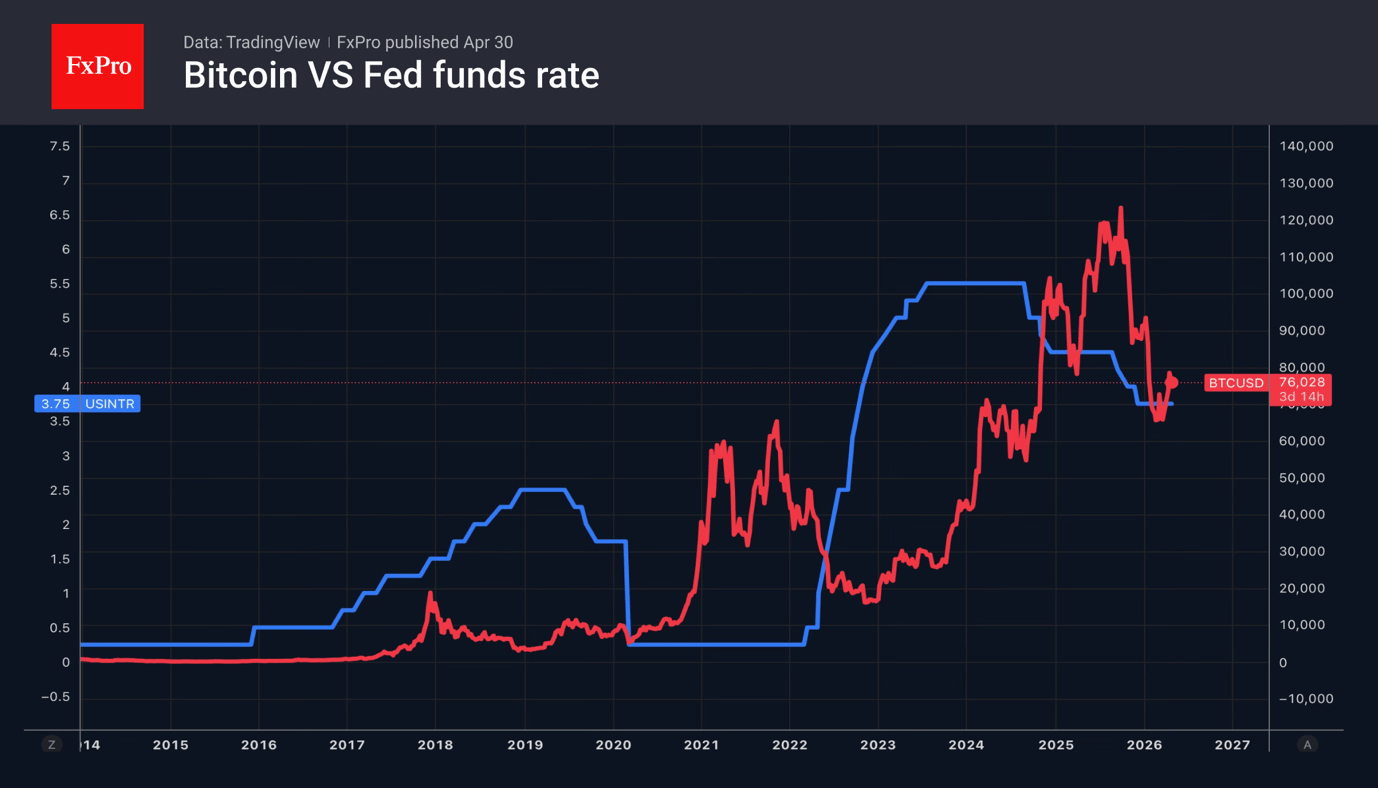

Bitcoin is not seeing the same bullish momentum as the stock market. A key barrier around 80,000 is holding the price back, prompting investors to take profits.

Strong demand for derivatives at this level is forcing market makers to hedge by selling as Bitcoin approaches it. As a result, each attempt to extend the rally is quickly capped.

Also, the macroeconomic backdrop is not conducive to a resumption of the uptrend. Galaxy Digital notes that when Bitcoin was trading near record highs in the autumn of 2025, the Fed was cutting rates. Doing so now would be problematic, as rising oil prices stemming from the conflict in the Middle East are forcing central banks to maintain tight monetary policy.

What next?

The key event on the economic calendar for the first full five-day week of May will be the US April jobs report. The data will either confirm or refute Jerome Powell’s suggestion that the labour market is stabilising. If this is indeed the case, accelerating US inflation driven by rising energy prices and second-order effects will pave the way for a federal funds rate hike in 2026, which would be good news for the dollar.

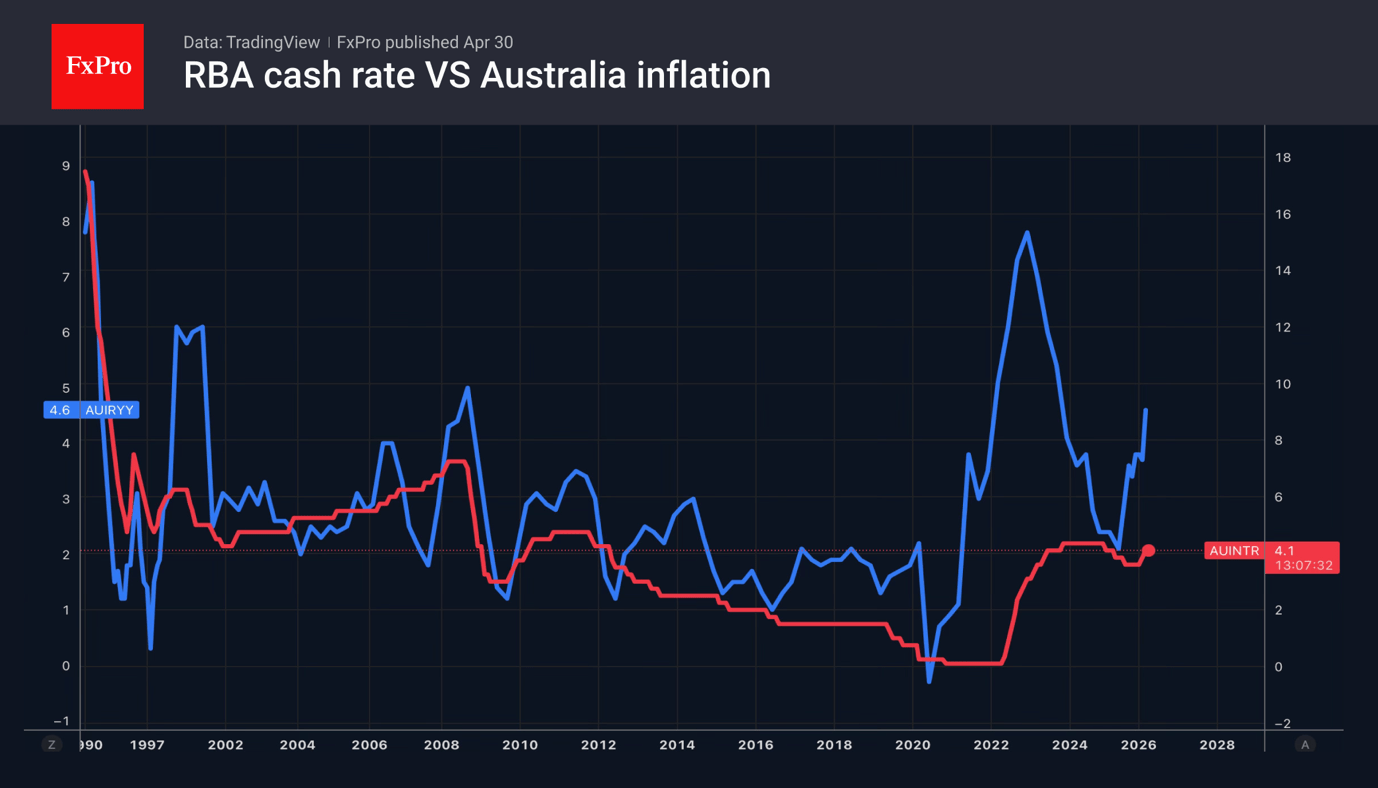

Other key events this week include the Reserve Bank of Australia meeting, where markets are pricing in the risk of another 25-basis point rate hike to 4.35 per cent, which could support AUDUSD. In the US, attention will be on the March trade balance data and the April ISM services figures. Meanwhile, New Zealand will release its first-quarter employment data.

Investors will continue to monitor developments in the Middle East. The current lack of major updates may suggest a period of calm before potential volatility returns. The longer this lasts, the higher the risks of conflict escalation, including a return to hostilities between the US and Iran.

{kind=link}