Sample Category Title

Trade Idea Wrap-up: GBP/USD – Sell at 1.3285

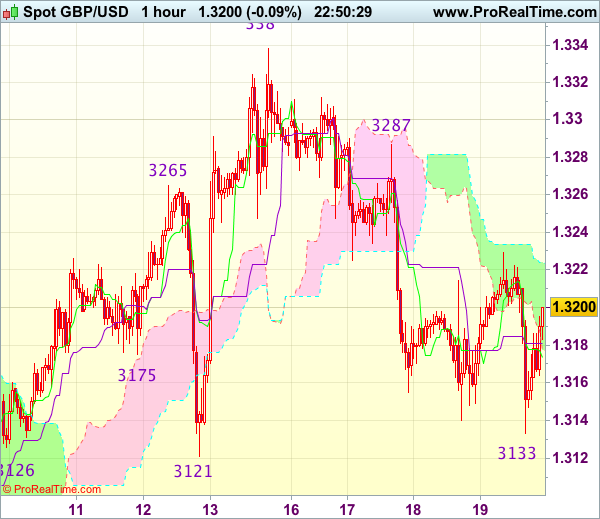

GBP/USD - 1.3205

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3172

Kijun-Sen level : 1.3181

Ichimoku cloud top : 1.3224

Ichimoku cloud bottom : 1.3177

Original strategy :

Sell at 1.3265, Target: 1.3145, Stop: 1.3300

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3285, Target: 1.3165, Stop: 1.3320

Position : -

Target : -

Stop : -

Although cable fell briefly to 1.3133 in London morning, lack of follow through selling and current rebound suggest consolidation would be seen and recovery to 1.3220-25 cannot be ruled out, however, reckon upside would be limited to 1.3255-65 and resistance at 1.3287 should hold, bring another decline later, below said support at 1.3133 would extend the fall from 1.3338 to support at 1.3121, however, break there is needed to retain bearishness and bring further subsequent decline to 1.3090-00.

In view of this, wee are looking to sell cable on further subsequent recovery as resistance at 1.3287 should cap upside, bring another decline later. Only a firm break above said resistance at 1.3287 would abort and signal low is formed instead, bring rebound to 1.3300 and possibly test of resistance at 1.3312.

Kiwi Bears Take Charge on New Government Announcement; Pound Slips after Retail Sales Slump

The kiwi posted additional long red candles during the European session after the kingmaker New Zealand First party backed the opposition party early today, forming a new coalition government. The pound fully reversed yesterday's gains in the wake of worse-than-expected retail sales.

September's British retail sales tumbled by 0.8% from August, surprising analysts who had projected a smaller contraction of 0.1% as the pound's weakness raised import costs and hence hit consumers' wallets. The previous reading was also revised downwards from 1.0% to 0.9%. On an annual basis, retail sales grew at a slower pace at 1.2%, missing the forecast of a growth of 2.1%. The three-month average growth also narrowed, slowing to 1.5% y/y – a four-year low. Excluding auto sales and fuel, consumers' spending declined by 0.7% m/m, driving the yearly gauge lower to 1.6%.

Meanwhile in Brussels, the UK Prime Minister is preparing to address EU leaders in a bid to unlock Brexit talks and move negotiations to the next stage of UK's future relationship with the block. Yet, rumors are for the negotiations to remain deadlocked until December, with a senior EU diplomat claiming early today that trade talks have a 50-50 chance to start by year-end.

The pound pulled back by 0.15% to $1.3184 as the data pared the odds for further rate hikes in 2018. Still, chances for a rate rise at the BOE's meeting in November stood around 80%.

The Catalan leader, Charles Puigdemont, missed the second deadline today imposed by the Spanish government, refusing to renounce independence and eventually having to face the consequences. Instead, he sent a letter to the Spanish Prime Minister, Mariano Rajoy, early on Thursday, warning a declaration of a unilateral independence if Madrid keeps blocking dialogue. In response, Rajoy said that he would hold a cabinet meeting on Saturday to activate Article 155 which has never invoked before, allowing the Spanish government to impose direct rule over Catalonia.

With markets having already priced in Catalonia's story, with risks remaining if situations escalate, the euro jumped to a one-week high of $1.1849 as Reuters poll of economists showed that the ECB will announce on October 26 its decision to trim monthly asset purchases from 60 billion euros to 40 billion in January.

While US stocks were weakening, upbeat readings on US initial jobless claims and business conditions measured by the Philadelphia Fed survey did little for the dollar. The number of Americans applying for unemployment benefits for the week ending October 14 reached the lowest in more than 44 years at 222,000 – probably affected by the Columbus Day holiday on Monday of that week. Projections were for claims to rise by 244,00 from the downwardly revised 244,000recorded in the week before. The four-week average measure which wipes out weekly volatility dropped by 19,500 to 248,250.

In another report, the Philadelphia Fed Manufacturing index jumped by 4.1 points to a five-month high of +27.9, beating the forecast of +22.0.

Back in Washington, the Senate is expected to vote on the 2018 budget resolution, which if approved would allow the Republicans to pass their proposed tax overhaul through the chamber without support from the Democrats.

The dollar index was down by 0.21% on the day at 93.16. Dollar/yen declined by 0.44% to 112.40 after reaching a two-week high of 113.14 earlier in the day.

The kiwi dipped further into losses, touching a fresh five-month low of $0.7014 and being 1.8% down on the day on the news that the leader of the Labour Party, Jacinda Ardern, would enter into a coalition with the First Partyto govern for the next three years, succeeding Prime Minister Bill English of the National Party. Markets are also nervous on what this would mean for the country's monetary policy.

In energy markets, investors engaged in profit-taking amid tensions in the Middle East, sending oil prices to one-week low levels despite OPEC Secretary General Mohammad Barkido saying on Thursday that oil markets are rebalancing at an "accelerating pace". WTI crude slipped by 1.40% to $51.31 per barrel and Brent fell by 1.40% to $57.33.

Gold surged by 0.55% to an intra-day high of $1,289.56 per ounce before it slipped back to $1,287.45.

Trade Idea Wrap-up: EUR/USD – Exit short entered at 1.1850

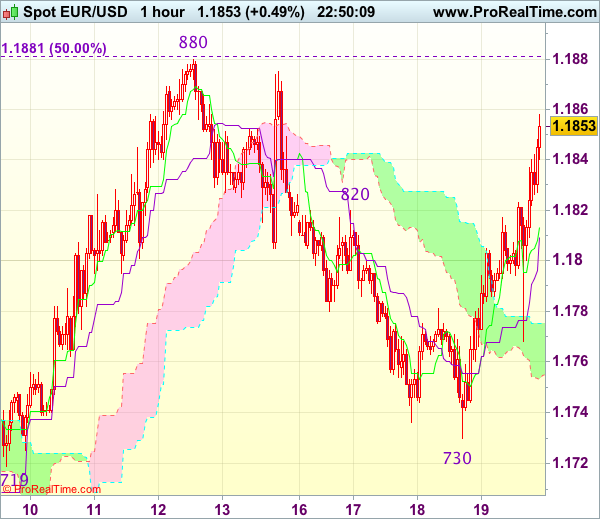

EUR/USD - 1.1848

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1813

Kijun-Sen level : 1.1809

Ichimoku cloud top : 1.1775

Ichimoku cloud bottom : 1.1755

Original strategy :

Sold at 1.1850, Target: 1.1750, Stop: 1.1885

Position : - Short at 1.1850,

Target : - 1.1750

Stop : - 1.1885

New strategy :

Exit short entered at 1.1850,

Position : - Short at 1.1850

Target : -

Stop : -

As the single currency found renewed buying interest at 1.1768 earlier today in European session and has rallied, dampening our bearishness and near term upside risk remains for the rebound from 1.1730 to extend gain to resistance at 1.1880 but break there is needed to retain bullishness and signal another leg of erratic upmove from 1.1669 low is underway for gain to 1.1900-10 first.

In view of this, would be prudent to exit short entered at 1.1850 and stand aside for now. Below 1.1820 would bring weakness to 1.1800 but said support at 1.1768 should remain intact, bring another rise later. Only a drop below this support would revive bearishness for weakness to 1.1730-40, break there would extend fall to 1.1700 but said recent low at 1.1669 should remain intact.

Yen Improves Despite Strong US Data

The Japanese yen has gained ground on Thursday, erasing most of the losses which marked the Wednesday session. In the North American session, USD/JPY is trading at 112.41, down 0.45% on the day. In economic news, unemployment claims plunged to 222 thousand, well below the estimate of 240 thousand. There was more good news, as the Philly Fed Manufacturing Index jumped to 27.9, crushing the estimate of 21.9 points. On Friday, the US will release Existing Home Sales and Fed Chair Janet Yellen speaks at an event in Washington.

Who will replace Janet? The markets are keeping a close eye on who will replace Janet Yellen as head of the powerful Federal Reserve. Yellen is due to finish her 3-year term in February 2018. Yellen is apparently interested in serving a second term, but President Trump likely has other ideas. Trump has not been complimentary towards Yellen, although it's hard to argue that Yellen has done an admirable job. Yellen has ended quantitative easing, raised interest rates and started to unwind the Fed's balance sheet. Trump's shortlist includes Jerome Powell, Kevin Warsh and John Taylor. Trump may lean towards Taylor, an economist who is considered more hawkish on policy than Yellen. Under Taylor, interest rates would likely move substantially higher than the current 1.25%, and a rate hike early in 2018 could strengthen the US dollar.

Japan's economy has impressed in 2017, and an important reason for the rebound has been the manufacturing sector. Manufacturing indicators are pointing upwards and recent polls are pointing to strong optimism among manufacturers. A Reuters poll released on Tuesday showed that manufacturer confidence in October was at its highest level since 2007, echoing a Bank of Japan survey taken earlier in October. Automobile and electric machinery exports remain strong and have helped boost the manufacturing sector. The BOJ holds a policy meeting on October 30-31, at which time it will set interest rates and will also publish its long-term economic and price forecasts. We can expect the economic forecasts to be more positive than the inflation projection. With the BoJ forecasting that inflation will not reach 2 percent until fiscal year 2020, it's a safe bet that the bank's accommodative policy will not be tightened any time soon.

Economic Growth in China Remains Largely Unchanged in Q3

Chinese real GDP growth met expectations in Q3, rising 6.8 percent year-over-year. The deceleration in fixed investment spending in China continued, however, as a result of both secular and cyclical trends.

Chinese GDP Growth Slows Slightly in Q3

Data released today showed the Chinese economy growing 6.8 percent on a year-ago basis in Q3, matching the Bloomberg consensus forecast (top chart). The print marks a 0.1 percentage point slowdown from the 6.9 percent pace registered through the first two quarters of the year.

Although a breakdown of GDP into its demand components is not yet available, sector level data indicate that growth was largely steady in the key sectors of the Chinese economy. Growth in the secondary industry, which includes mining/quarrying, manufacturing, construction and utilities production, ticked lower by 0.1 percentage point to 6.3 percent on a year-over-year, year-to-date basis. The momentum may have reversed course late in the quarter, however, as Chinese industrial production data released in a separate report today showed output climbing 6.6 percent year-over-year in September, a marked improvement from the 2017 low of 6.0 percent growth in August. Growth in the tertiary industry, or the service sector, was modestly stronger, as was output in the primary sector, which includes agriculture, forestry and fishing.

Economic growth in China has firmed in 2017 relative to last year's pace amid the stronger global growth environment. At present, we expect real global GDP to accelerate about half a percentage point in 2017 from the growth rate registered in 2016. Even with the faster growth at home and abroad, fixed investment spending in China has continued to decelerate (middle chart). Some of the slowdown has been the continuation of a secular trend; investment spending has decelerated for most of this cycle as the Chinese economy continues the steady transition towards a more consumption-oriented growth model. To that point, retail sales data released today showed continued double-digit year-to-date growth through the month of September. More recently, investment spending growth has continued to slow as Chinese policymakers have moved to tighten policy amid concerns that the credit expansion, that occurred when the economy was slowing, might lead to debt imbalances.

Outlook Is for Modestly Slower Growth in China in 2018

As we have highlighted in previous reports, the leverage in the nonfinancial corporate sector in China, particularly for state-owned enterprises (SOEs) is an area we have identified as a potential risk to the outlook (bottom chart).* At the ongoing 19th Party Congress, the signals from leaders have suggested that policymakers will not move anytime soon to scale back the SOEs. We do not believe the corporate leverage/SOE challenges are likely to cause an implosion in the Chinese economy anytime soon, but they do represent both a downside risk to the outlook and a secular drag on the economy's potential growth rate. We continue to expect real GDP in China to decelerate modestly in 2018 to a 6.3 percent pace.

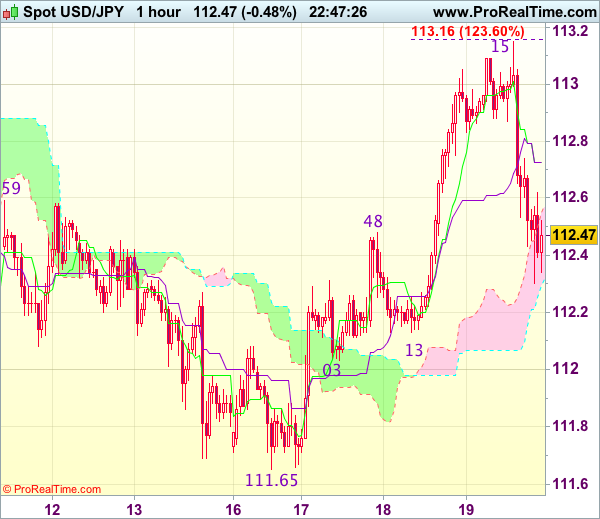

Trade Idea Wrap-up: USD/JPY -Stand aside

USD/JPY - 112.54

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.73

Kijun-Sen level : 112.73

Ichimoku cloud top : 112.55

Ichimoku cloud bottom : 112.30

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day brief rise to 113.15, the subsequent much deeper than expected retreat has dampened our bullishness and signals a temporary top has been formed there, hence consolidation with mild downside bias is seen for test of indicated strong support area at 112.03-13 but break there is needed to add credence to this view and signal the rebound from 111.65 has ended, bring another fall towards this level later.

On the upside, whilst recovery to the Kijun-Sen (now at 112.73) cannot be ruled out, price should falter well below said resistance at 113.15 and bring another retreat later. Only break of said resistance at 113.15 would revive bullishness for retest of recent high at 113.44 which is likely to hold on first testing.

Chinese Economic Activity Weakens in the Third Quarter, In Line With Expectations

Chinese real gross domestic product (GDP) rose by 6.8% (year-on-year) in the third quarter, in line with consensus expectations. On a quarter-over-quarter basis, growth slowed a touch to a 1.7% pace in the third quarter, also in line with consensus. Growth in 17Q1 was revised up to 1.4% q/q from 1.3%, while growth in 17Q2 was revised up to 1.8% q/q from 1.7%. Altogether, the data released overnight puts China's economy on pace to expand at a 6.8% pace in 2017.

Nominal GDP grew 11.2% (y/y) in the third quarter, on par with the 11.1% pace recorded in the second quarter. Producer prices rose an average of 6.3% y/y, extending the streak of strong producer price gains that began at the start of this year. Consumer prices rose an average of 1.6% y/y in the quarter, the strongest pace of advance seen this year.

Economic activity on an industry basis was broad-based, with all major sectors expanding on a year-on-year basis. Secondary industry performance slowed a touch in the third quarter, likely a reflection of slower construction activity. Growth in tertiary (services) industries ticked up a bit from the previous quarter and recorded the strongest gain yet this year at 8.0% y/y. Service industries comprise the largest share of economic activity in China at just over half.

Fixed asset investment (excluding rural areas) slowed to a sub-8.0% trend pace in the third quarter after advancing at almost a 9.0% trend pace in the second quarter (reported on a year-over-year, year-to-date basis). It should be noted that fixed asset investment has been slowing consistently since early-2013 when it was rising by around 20% per year, reflecting the shift toward services.

Industrial production rose 6.6% (y/y) in September, a touch firmer than the consensus call for a 6.5% gain. However, industrial production in the third quarter as a whole slowed to its slowest pace of advance year-to-date at 6.3% y/y, suggesting slower economic activity in the fourth quarter.

Key Implications

Once again Chinese economic activity did not disappoint market expectations. But, monthly indicator data suggests that growth is likely to slow a bit further in the fourth quarter, reminiscent of the trend of strong mid-year growth giving way to weaker activity at year-end and at the start of the next year observed since 2015.

Concerns remain about the rapid pace of credit growth in China, particularly in the years following the Great Recession. Total social financing credit growth ticked up a touch in the third quarter, but remained well below the strong pace recorded in the first quarter. Slower credit growth is consistent with weaker trend growth of fixed asset investment. Chinese authorities have made some gains in reining in excess credit growth, but remain sensitive to historically high and rising levels of debt across all sectors (consisting of corporate, household, and government) in light of the risks that this poses to its domestic banking sector, particularly in an environment of slowing economic growth. As such, we anticipate policymakers will continue to maintain a tightening bias in domestic credit conditions at least for the remainder of this year.

The 19th National Congress of the Communist Party of China kicked off yesterday, and is expected to last until October 24th. Over the next few days we anticipate Chinese officials to outline an updated five-year economic plan for China, as well as announce new political appointments. Some of the most notable announcements thus far include ambitions for China to become a globally influential leader by 2050, and plans to continue to pursue market-oriented reforms that help to assure foreigners that China will open up to more foreign investment. We plan on releasing a summary of the major announcements after the conclusion of the congress.

Brent Oil Plunges

The price dropped sharply and erased the last two day's gains. It could drop much deeper in the upcoming days if will close the day below the $57.30 per barrel. Brent is very heavy right now and seems poised to turn to the downside again in the upcoming period. The rate is pressuring an important dynamic support, a valid breakdown will signal a further drop in the upcoming period.

I've said in the previous weeks that the rate could start a larger drop if will stabilize somewhere below the 57.00 psychological level. Price increased in the last weeks, but I've said that this could be only temporary and the bears could take the lead again on the short term.

Brent drops even if the United States Crude Oil Inventories have dropped to -5.7 million barrels in the previous week, much below the -4.7M estimate and versus the -2.7M in the former reading period.

Price edges lower on the Daily chart and looks determined to take out the dynamic support from the median line (ML) of the major ascending pitchfork and the horizontal support from the 57.72 static support.

Will drop much deeper if will close below the median line (ML) of the ascending pitchfork. Technically, it is expected to drop much deeper after the failure to reach and retest the upside line of the ascending channel and the 59.50 previous high. Only a valid breakdown from the up channel will signal a further drop.

EUR/CHF Setting Up For Further Gains

The rate dropped significantly today and recovered after the yesterday's impressive rally. Is retesting the broken fifth waring line (wl5) of the former descending pitchfork, the 1.1536 broken horizontal resistance (resistance turned into support) and the upper median line (uml) of the minor descending pitchfork.

A rejection from here will send the rate much higher in the upcoming period, the next target will be at the 1.1621 previous high.

EUR/GBP Testing A Confluence Area

EUR/GBP increased sharply and resumed the minor rebound. Is pressuring the confluence between the minor downtrend with the median line (ML) of the major ascending pitchfork. A valid breakout through the confluence area and above the 0.9000 psychological level will accelerate the bullish momentum. Another drop will be confirmed by a rejection, followed by a minor drop.