Sample Category Title

How Will Traders Respond To Dip In US Stocks?

- Buy the dip mentality put to the test on Thursday;

- Madrid prepares to trigger article 155;

- Softer Chinese data partially blamed for profit taking;

- UK retail sales miss should be warning to BoE.

US futures are coming under a little pressure on Thursday, a day after the Dow closed above 23,000 for the first time ever, in what appears to be some profit taking following an impressive run for stocks.

While there were no major triggers for this morning's decline, the finger is being pointed at the softer Chinese economic data and unrest in Spain, where the government announced its intention to trigger article 155 and suspend Catalonia's autonomy. While neither of these are reason for traders to be bearish stocks right now, it has been pounced upon as reason to take some money off the table and await further opportunities.

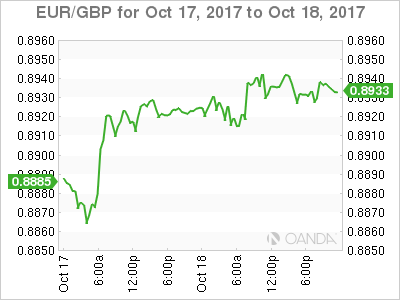

The situation in Spain is having a greater impact on the wider European markets, particularly in the IBEX which is down around 1% as investors prepare for more unrest in Catalonia. The euro has been very unresponsive to the developments in Spain so far and the same is true again today, with the single currency trading higher against the dollar, pound and yen. This is clearly seen as being a risk unique to Spain, rather than a problem that could develop elsewhere, although the Italian FTSE MIB has shown some vulnerability to it throughout the process.

It will be interesting to see how US traders respond to the dip at the open. Sentiment has been extremely positive recently, despite the significant amount of political and geopolitical risk lingering beneath the surface. The global growth story is giving people great confidence that the rally has legs to it and earnings for the third quarter of likely to support that.

The Chinese economic data released overnight was broadly in line with expectations but did highlight the fact that the economy is slowing a little in the second half of the year. This was widely expected though as the government has reined in spending and focused more on cooling the housing market and reforms. We can expect more of the same in the fourth quarter although as we saw in the third, the improved global economic environment is likely to support the Chinese economy through this transition.

In the UK, retail sales wrapped up a week of important economic releases and left us with a bitter taste. Perhaps expectations were too high and a larger decline should have been expected following the strong showing in August but instead the data fell well short of forecasts. The numbers further highlighted what we already know, the UK consumer is feeling the strain of negative real wage growth and this will take its toll on spending. While the inflation and jobs data may be seen as justifying a rate hike from the Bank of England, today's data should be a warning to policy makers that the economy is not in a good position to take it.

While the focus today is likely to be how US markets respond to early weakness, we will also get some manufacturing and jobless claims data from the world's largest economy. We'll also get third quarter earnings reports from 20 S&P 500 companies including Verizon, Paypal and Travelers. Esther George of the Federal Reserve is also scheduled to appear while Chair Janet Yellen is also believed to be meeting with President Donald Trump, who is understood to be making a decision on her successor in the coming days

DAX Drops As Catalan Tensions Worsen

The DAX has recorded losses in the Thursday session. Currently, the index is at 12,958.50 down 0.65% on the day. On the release front, there are no major indicators out of the eurozone. On Friday, Germany releases PPI and the eurozone will publish its current account surplus.

The Spanish stock market is down 1.0% on the day, and this has dragged down other European stock markets, including the DAX. The crisis over Catalan independence has worsened, as the Catalan government ignored a deadline to withdraw its independence bid, prompting Madrid to threaten it would impose direct control on the region on Saturday. Analysts continue to digest European corporate earnings for the third quarter, and the results will likely have a strong impact on the stock markets next week.

All eyes are on Spain, as investors are nervously monitoring the constitutional crisis in Catalonia. The Catalan government has refused to comply with a demand by Madrid to withdraw its declaration of independence, and the central government has responded harshly, saying it will invoke Article 155 of the Spanish Constitution and impose direct control over Catalonia. However, the government must first receive approval from the Senate before it implements this measure, and the Senate is expected to approve the move on Saturday. Madrid has said that it will not invoke this measure if the Catalan parliament calls new elections, but so far there has been no response from Catalan leaders. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and send the euro lower.

Euro Quiet, Catalonia Crisis Deepens

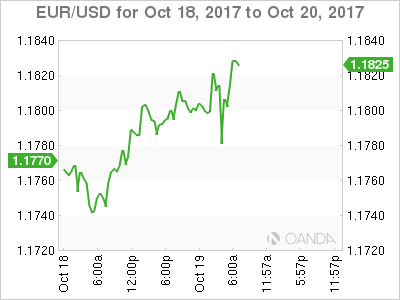

The euro has edged higher in the Thursday session, as EUR/USD stays close to the 1.18 line. Currently, EUR/USD is trading at 1.1812, up 0.22% on the day. On the release front, there are no major indicators out of the eurozone. In the US, unemployment claims are expected to dip to 240 thousand, while the Philly Fed Manufacturing Index is forecast to slow to 21.9 points. On Friday, Germany releases PPI and the eurozone will publish its current account surplus. The US will release Existing Home Sales and Fed Chair Janet Yellen speaks at an event in Washington.

The crisis in Catalonia continues, as the Spanish and Catalan governments remain entrenched in their positions. The Catalan government has refused to comply with a demand by Madrid to withdraw its declaration of independence, and the central government has responded harshly, saying it will invoke Article 155 of the Spanish Constitution and impose direct control over Catalonia. However, the government must first receive approval from the Senate before it implements this measure, and the Senate is expected to approve the move on Saturday. Madrid has said that it will not invoke this measure if the Catalan parliament calls new elections, but so far there has been no response from Catalan leaders. The deepening constitutional crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor’s rating agency has said that the region could face a recession if the situation is not resolve. Investment projects are at a standstill in the region, and if the situation worsens, investors could get nervous and send the euro lower.

European Union leaders will gather in Brussels on Thursday and Friday. The meeting was expected to focus on Brexit, but with talks with Britain floundering, Brexit will likely take a back step. The EU may do little more than declare that trade talks with London will not begin until there is more progress on other issues, such as the amount Britain will pay when it leaves the club. There are a number of other topics on the agenda, including the crisis in Catalonia, the Iran nuclear agreement, and a proposal to deepen integration among EU members.

Spain To Trigger Suspension Of Catalan Autonomy On Saturday

Spain's government will trigger on Saturday the Article 155 of the constitution, which allows it to suspend Catalonia's political autonomy.

This mornings special cabinet meeting was called after Catalan leader Carles Puigdemont said the regional parliament could vote on a formal declaration of independence from Spain if the central government failed to agree to talks.

Bond Spreads

Eurozone periphery government bond spreads have widened as Catalan President Carles Puigdemont says he might formally declare independence if Madrid refuses dialogue.

Moves are limited, however. Ten-year Spanish, Italian and Portuguese bond yield spreads over equivalent German bunds are by up to +2 bps wider, with the most widening in Portuguese spreads and the least in Spanish spreads. The 10-year Spanish-German spread trades at +124 bps, up +1.2 bps.

The Spanish government have confirmed to hold an emergency Cabinet meeting on Sat, Oct 21st to begin process of suspending Catalan autonomy under Article 155

The EUR (€1.1804) is currently off its intraday Euro highs and is straddling the psychological €1.18 handle

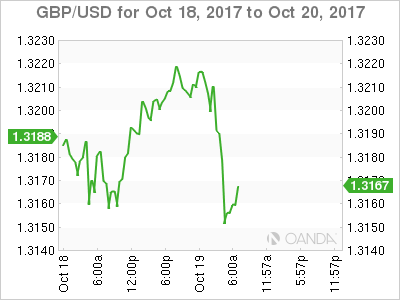

U.K Retail Sales Weak In Q3, Pound Falls

Data from the Office for National Statistics this morning showed that U.K retail sales fell by more than expected in the month of September and points to weakness in the broader economy during Q3.

Retail sales were -0.8% lower than in August, and were just +1.2% higher than a year earlier. The consensus had expected monthly sales volumes to remain flat.

The decline was driven largely by a fall in sales of non-essential items, such as spectacles, souvenirs, weapons and collectables.

The weak performance means retail sales will contribute just +0.03% to third-quarter economic growth, roughly a third the contribution in the second quarter, the ONS says.

Today's figures would suggest that the British consumer might be retrenching amid meager wage growth and high inflation.

Sterling (£1.3156) has dropped to a one-week low outright and against the EUR (€0.8980).

NZD Tumbles Amid Labour Coalition Government

NZD tumbles as New Zealand shifts to the left

The New Zealand dollar took a hit on Thursday, falling more than 1.70% against the US dollar as investors reacted to the outcome of the coalition government. The Kiwi started to tumble around mid-day local time following rumours that the Labour Party was about to form a coalition government. The official announcement came a few hours later as Winston Peter, leader of NZ First, announced his party will now back the Labour Party rather than the National Party. The Kiwi’s fall accelerated. Jacinda Ardern, leader of the Labour Party, is taking over William English’s seat as New Zealand’s Prime Minister. Winston Peters will most likely become Deputy Prime Minister.

Without surprise, the market did not welcome the news as investors expect more expansionist policies from the new government, such as an increase in living allowances and free tertiary education, which will led to an increase in expense.

There is plenty of room for further Kiwie depreciation as speculators have built massive long position over the summer. They already started to unwind their bullish bets starting in August as they felt the wind was shifting. As of last week, net long non-commercial future positions accounted for roughly 15.7 % of total open interest, compared to over 63% in July. The Kiwi has broken all of its supports and the road is now wide open towards $0.6818 (low from May 11th).

Catalonia fails to clarity and Spain suspend autonomy

The deadline for Catalonia to provide clarity on independence declarations has come and gone. In the eyes of Madrid the lack of a response was the same as maintained Catalonia demand for independence. Rajoy and the Spanish government have been unwilling to take their feet off the petal. The prime minister office stated that would meet to activate Article 155 of the constitution regardless. Article 155, although untested is expected to suspect Catalonia autonomy. EURUSD dropped immediately to 1.1770 before rallying right back. Despite the growing political crisis in Catalonia, as the regional feels even more directionless, market expect that Spain and EU will prevail. The faith in a dominate federalist system has limited political risk spillover into FX, yields or volatility. The situation remains fluid, with the next move likely to come from Catalonia regional government. However, we remain skeptical of any contagion given the strength of Europe and would fade headlines.

Market Update – European Session: Political Events Dominate Trading Sentiment

Notes/Observations

New Zealand puts together a new govt; highlighting political shift toward protectionism

Catalan leader gives another vague response to Spanish govt over the independence referendum; Central govt to meet on Sat to begin the Article 155 procedure to strip the region of its powers as Catalonia's leader defied an ultimatum to renounce his push for independence

Overnight

Asia:

China Q3 GDP data in-line (Q/Q: 1.7% v 1.7%e; Y/Y: 6.8% v 6.8%e) with back quarters revised higher

China Sept Industrial Production Y/Y: 6.6% v 6.5%e

China Sept Retail sales Y/Y: 10.3% v 10.2%e

(AU) Australia Sept Employment Change: +19.8K v +15.0Ke; Unemployment Rate: 5.5% v 5.6%e

(KR) Bank of Korea (BOK) left its 7-Day Repo Rate unchanged at 1.25% (as expected). Decision was not unanimous (1 member, Lee Il-Houng, called for a rate hike). Staff forecasts raised 2017 growth and inflation outlook)

Europe:

EU's Tusk stated that saw promising progress in the Brexit negotiations and would recommend start of internal preparations for phase two of Brexit talks. Did not expect any breakthrough in Brexit talks on Thursday, Oct 19th as needed more concrete proposals from British side to have sufficient progress in Dec

Catalan leader Puigdemont reportedly would announce independence if Spain govt suspended regional autonomy

Americas:

Fed’s Beige Book: Wage pressures remain modest to moderate despite labor market tightness. Economy expanded at a modest to moderate pace in Sept through early Oct in all 12 districts

Sen Cornyn (R-TX): GOP has sufficient votes to pass the budget measure which advances tax reform effort

Economic Data

(NL) Netherlands Sept Unemployment Rate: 4.7% v 4.6%e

(CH) Swiss Sept Trade Balance (CHF): 2.9B v 2.2B prior; Real Exports M/m: -0.9% v +3.4% prior; Real Imports M/M: -3.2% v +3.3% prior

(NO) Norway Q3 House Price Index Q/Q-1.0% v -0.4% prior

(JP) Japan Sept Final Machine Tool Orders Y/Y: 45.0% v 45.3% prelim

(SE) Sweden Sept Unemployment Rate: 6.2% v 6.0%e; Unemployment Rate (Seasonally adj): 6.8% v 6.5%e

(UK) Sept Retail Sales Ex Auto Fuel M/M: -0.7% v -0.2%e; Y/Y: 1.6% v 2.2%e

(UK) Sept Retail Sales (including Auto Fuel) M/M: -0.8% v -0.1%e; Y/Y: 1.2% v 2.1%e

(HK) Hong Kong Sept Unemployment Rate: 3.1% v 3.1%e

Fixed Income Issuance:

(ES) Spain Agency (Tesoro) sold total €4.53B vs. €4.0-5.0B indicated range in 2021, 2025, 2027 and 2046 bonds

Sold €1.81B in Jan 0.05% 2021 SPGB bond; Avg yield: +0.043% v -0.027% prior, Bid-to-cover: 1.38x v 2.6x prior

Sold €965M in 4.65% Oct 2025 SPGB; Avg Yield: 1.124% v 1.061% prior; Bid-to-cover: 1.48x v 1.8x prior

Sold €1.02B in 1.45% Oct 2027 SPGB; Avg yield: 1.627% v 1.54% prior; Bid-to-cover: 1.79x v 1.97x prior

Sold €740M in 2.90% Oct 2046 SPGB; Avg Yield: 2.874% v 2.904% prior; Bid-to-cover: 1.55x v 1.25x prior

(FR) France Debt Agency (AFT) sold total €6.996B vs. €6.0-7.0B indicated range in 2021, 2023 and 2024 Oats

Sold €1.801B in 0.00% 2021 Oat; Avg Yield: -0.39% v -0.37% prior; Bid-to-cover: 2.07x v 2.72x prior

Sold €2.57B in 0% 2023 Oat; Avg Yield: -0.07% v 0.00% prior; bid-to-cover: 1.10x v 1.65x prior

Sold €2.625B in 1.75% 2024 Oat;Avg Yield: 0.18% v 0.28% prior; bid-to-cover: 2.03x v 2.12x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.6% at 389.4, FTSE -0.3% at 7521, DAX -0.5% at 12977, CAC-40 -0.4% at 5361, IBEX-35 -0.7% at 10200, FTSE MIB -0.8% at 22177, SMI -0.4% at 9271, S&P 500 Futures -0.4%]

Market Focal Points/Key Themes:

European stocks drop over concerns in Catalonia, with peripherals under performing; oil drop putting pressure on energy stocks; geopolitical situation driving muted risk sentiment; upcoming earnings in US session include Verizon, Danaher, Bank of New York and Textron

Equities

Consumer discretionary [Unilever [UNA.NL] -4.7% (Earnings), Pernod Ricard [RI.FR] +2.8% (Earnings), Publicis [PUB.FR] -5.7% (Earnings)]

-Consumer Staples [ Carrefour [CA.FR] +1.8% (Earnings)]

Industrials: [Thales [HO.FR] -2.4% (Earnings), Philips Lighting [LIGHT.NL] -4.3% (Earnings), Kion Group [KGX.UK] -8.8% (Trading update), Interserve [IRV.UK] -30% (Trading update)]

Technology: [ SAP [SAP.DE] -2.0% (Earnings)]

Speakers

ECB's Nowotny (Austria): Cannot stop asset purchases 'abruptly', decision how to proceed must be made in Oct, sees arguments for slowing purchases. Saw inflation below 2% in 2017 and even lower in 2018 (**Note: in-line with ECB staff forecasts)

BOE's Haldane: Mixed jobs and wage data brings all sorts of questions regarding the future inflation pressures

UK Brexit Min Davis: 'Hard Brexit' was remote possibility. Wished that EU chief negotiator Barnier's mandate was more flexible

Catalonia leader clarified his stance on independence and noted that the suspension of the referendum remained in place. Parliament could vote for a formal declaration of independence if central govt does not hold talks

Spain PP (ruling party) Senate Spokesperson: Catalan response more of the same. Poised to use constitutional powers to strip Catalonia of some autonomy (**Note: Spain central govt Cabinet to meet on sat, Oct 21st to begin process of article 155 to strip the Catalan region of its powers)

Spain central govt confirmed to hold an emergency Cabinet meeting on Sat, Oct 21st to begin process of suspending Catalan autonomy under Article 155

Italy PM Gentiloni said to be keen on guaranteeing the Bank of Italy independence

Bank of International Settlements (BIS) Q2 Global cross-border lending lower by $91B q/q; led by Euro

Germany’s DIHK chamber of commerce raised its 2017 GDP from 1.8% to 2.0%. The domestic economy continued to run on high tours and expected 650,000 workers more this year, and a further increase of 600,000 in the next twelve months

Russia Foreign Min Lavrov: Concerned by growing NATO presence in Baltics

New Zealand puts together a working govt after First Party (opposition) reached a coalition agreement with Labour/Green party.

OPEC Sec Gen Barkindo: Oil market is re-balancing at an accelerating pace. balanced oil market fully in sight. Saw no peak of oil demand in the foreseeable future; global demand at 100M bpd in 2020 and at 111M bpd in 2040

Currencies

EUR/USD was holding below the 1.18 level as Catalonia's leader defied an ultimatum from Madrid by failing to renounce his push for independence

Softer UK retail sales data for Sept weighed upon the GBP currency.

The USD/JPY initially hit a 2-week high above the 113 level. Dealers noted that the outcome of this weekend’s General Election would likely to bring little surprise potential and reconfirm the commitment to Abenomics (continuity of current loose monetary policy and an expectation of keeping the yen weak). However, some weakness in global equity market provided some safe-haven flows and helped to strengthen the yen from its work levels

The NZD/USD was broadly lower as concerns simmered that the new Labour-led government would amend legislation on how the central bank operated. Some analysts believe a change to the RBNZ’'s mandate from solely targeting inflation could occur and add full employment to its existing sole mandate of price stability

Fixed Income

Bund futures trade 4 ticks higher at 162.22 off the highs of 162.56 with risk off sentiment the overriding theme. Continued upside past highs targets 162.78 while downside support seen at 162.13.

Thursday's liquidity report showed Wednesday's excess liquidity fell to €1.808T from €1.813T prior, use of the marginal lending facility rose to €341M v €320M prior.

Corporate issuance saw $9.75B come to market via 4 issuers lead by United Health $4B 5 part offering and RBC $2.5B 2 part offering. This bring weekly issuance to $15.4B and monthly issuance to $61.2B.

Looking Ahead

(EU) European Union Leaders begin 2-day Summit in Brussels

(ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave 7-Day Reverse Repo Rate unchanged at 4.25%

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

05:30 (UK) DMO to sell £2.5B in 1.25% 2027 Gilts

05:50 (FR) France Debt Agency (AFT) to sell €1.25-1.75B in 2025, 2027 and 2032 I/L Bonds (Oatei)

06:00 (IL) Israel Sept Consumer Confidence: No est v 124 prior

06:00 (PT) Portugal Sept PPI M/M: No est v 0.1% prior; Y/Y: No est v 2.5% prior

06:45 (US) Daily Libor Fixing

08:00 (PL) Poland Central Bank (NBP) Oct Minutes

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 240Ke v 243K prior; Continuing Claims: 1.89Me v 1.889M prior

08:30 (US) Oct Philadelphia Fed Business Outlook: 22.0e v 23.8 prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (IT) Italy Fin Min Padoan in Brussels

09:00 (BE) Belgium Oct Consumer Confidence: No est v 3 prior

09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

09:00 (RU) Russia Gold and Forex Reserve w/e Oct 13th: No est v $423.3B prior

09:30 (US) Fed’s George(hawk, non-voter)

10:00 (US) Sept Leading Index: 0.1%e v 0.4% prior

10:00 (BR) Brazil to sell 2023 LFT

10:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Treasury announcement on upcoming 2-year, 5-year and 7-year issuance

13:00 (US) Treasuries to sell $5.0B in 30-Year TIPS Reopening

17:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.50%

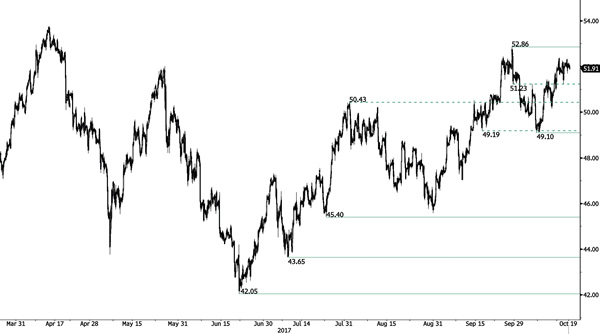

CRUDE OIL Consolidating Below Resistance At 52.86.

Crude oil is consolidating in range defined by the support at 50.43 and the strong resistance lies at 52.86 (28/09/2017). Expected to show continued increase within this range.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

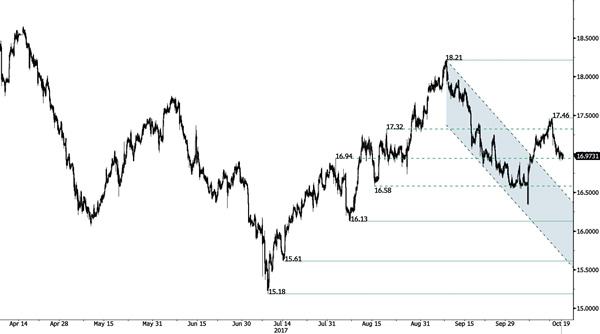

SILVER Sitting On Support At 16.94

Silver is weakening and is now resting on support at 16.94. Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low). Hourly resistance can be found at 17.10 (intraday high).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Off The Edge

Gold has broken the support at 1284 confirming an underlying bearish trend. Strong support lies at a distance at 1204 (10/07/2017 high). Resistance is located at 1288 (intraday high).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).