Sample Category Title

Technical Outlook: USDJPY Pulls Back On Safe-Haven Buying

The pair was sharply lower on Thursday, pulling back after renewed probe above 113.00 barrier, which was dented on Wednesday’s strong rally.

Fresh weakness comes in reaction on sharp fall of Japanese stocks, triggered by latest rising uncertainty over Catalonia, which sparked fresh safe-haven buying.

Pullback found footstep at 112.57 (Fibo 38.2% of 111.65/113.14 upleg) but deeper pullback cannot be ruled out if situation in Catalonia deteriorates.

Break below 112.57 and converged 10/20SMA’s at 112.43 would generate stronger bearish signal and risk further downside.

Wednesday’s low at 112.13 marks next pivotal support, loss of which would risk fresh attack at key 200SMA support (111.74).

Conversely, extended consolidation ahead of final attack at key 113.25/43 barriers could be expected while pullback stays limited.

Res: 113.14, 113.25, 113.43, 114.00

Sup: 112.57, 112.43, 112.13, 111.85

The 19th CCP Congress – A Summit For Xi To Crown Himself

Predominantly the most important political event in China, the twice-in-a-decade National Congress of the Chinese Communist Party began on October 18. As a kick start, President Xi delivered a Party Work Report which reviewed the achievements in his first five years and outlined the challenges and goals for the next five years and beyond. Xi outlined his thoughts on the 'new era of socialism with Chinese characteristics' On the economic reform, he suggested further developments in the "advanced manufacturing industry", which includes medium and high end consumption, green and low carbon industry, sharing economy, modern logistics and human capital services. He has also pledged to deepen interest rate and exchange rate reforms, develop a comprehensive financial regulation system and reduce systematic financial risk. These are nothing new as the key aspects of the monetary and fiscal policies have already been lain down at the National Financial Work Conference in July.

Xi's Power Consolidation

There are several events that worth attention in the following days. Yet, we believe the focus of the week-long Congress is on consolidation of Xi Jinping's power. The Central Committee would be elected at the end of the Congress, likely on October 24. This would be followed by the first Central Committee Plenary session for election of the Politburo members (25 members) and the 7-member Politburo Standing Committee (the top leadership for the coming 5 years). The name list would be announced on October 25. Since he has become the General Secretary of the Central Committee of CCP in 2012 and the 7th Chinese President in 2013, Xi has been removing personnel he deemed disloyal using the reason of cracking down corruption. Undoubtedly, Xi's cabinet would be composed of his loyalists so that he would cling to absolute power. To further cement his power, the authoritarian party would discuss amendment of the constitution at the summit. This is expected to incorporate 'Xi's thought' in the constitution and Xi would be named the 'party chairman', a title never been used after Mao Zedong.

Dataflow Surprisingly Strong During Sensitive Moment

The macroeconomic data released over the past weeks have been positive. GDP expanded +6.8% y/y in 3Q17, in line with expectations but decelerated from +6.9% in the prior quarter. For the month of September, retail sales grew +10.3% y/y, beating consensus of +1.2% and August's +10.1%. Urban fixed asset investment grew +7.5% y/y in the first 9 months of the year, moderating from +7.8% in the year through to August. The market had anticipated a growth of +7.7%. IP growth accelerated to +6.6% y/y in September, from +6% in the prior month. This came in better than expectations of +6.4%. During the weekend, the government released the inflation data. CPI eased to +1.6% y/y in September from +1.6% a month ago. This came in line with expectations. PPI, however, accelerated to +6.9% y/y, from +6.3% in August. The market had anticipated a mild improvement to +6.4%. The set of data is of particular political importance during this period of time. A strong set of data allows Xi to cement his power and claim that his thoughts/ theories are at work to building a 'strong' and 'new era' of China.

Technical Outlook: Kiwi Dollar Falls Sharply On Political Uncertainty

The Kiwi dollar fell sharply on Thursday in reaction on political uncertainty after New Zealand First Party joined a coalition with Labor and Greens to form government.

Traders reacted on such decision with strong selling of New Zealand dollar, which fell over 1.5% against the greenback in late Asian trading.

Fresh bearish acceleration broke below previous low of 10 Oct at 0.7055 and left lower top at 0.7146 (17 Oct high), signaling continuation of broader downtrend from 2017 high at 0.7558 (posted on 27 July).

Bears returned below cracked Fibo support at 0.7100 and pressuring psychological support at 0.7000.

Close below 0.7100 (Fibo 61.8% of 0.6817/0.7558, May/July rally) is needed to generate strong bearish signal, with sustained break below 0.7000 handle to open way towards key med-term support at 0.6817 (2017 low, posted on 11 May).

Daily indicators are in full bearish setup (20/200 SMA Death-Cross is forming) and supportive for further weakness.

Broken 10SMA (0.7114) is expected to cap upticks and keep fresh bears intact.

Res: 0.7055, 0.7073, 0.7114, 0.7160

Sup: 0.7037, 0.7000, 0.6950, 0.6910

Technical Outlook: GBPUSD – Recovery Attempts Stalled Ahead Of UK Retail Sales

Cable fell back below 1.3200 after recovery attempts from Wednesday's downside rejection at 1.3140 (55SMA) stalled at 1.3228 on Thursday.

Fresh weakness diminishes hopes of stronger recovery after Wednesday's action was shaped in Hammer.

Mixed techs on daily chart show no clear near-term direction, with rising downside risk on recovery stall under top of hourly cloud (1.3232). Thick hourly cloud (spanned between 1.3203/32) so far limited recovery attempts, with sustained break above cloud needed to generate bullish signal.

UK Retail Sales data are in focus today, with forecast for September at -0.1% m/m vs 1.0% in Aug and 2.4% y/y vs 2.8% in Aug, seen as negative signal for Sterling if release comes at/below forecasts.

Bearish scenario could trigger acceleration through 55SMA pivot at 1.3140, towards 1.3100 and possible extension lower on stronger bearish acceleration.

Conversely, upbeat Retail Sales numbers in September would inflate pound and expose barriers at 1.3274 (falling 20SMA) and 1.3313 (30SMA).

Res: 1.3232, 1.3264, 1.3286, 1.3313

Sup: 1.3181, 1.3154, 1.3140, 1.3100

Technical Outlook: EURUSD – Politics Would Be Likely Main Driver For The Euro Today

The Euro holds positive near-term tone and extended recovery on Thursday after repeated strong downside rejections at 1.1730 and subsequent bounce added to the upside potential. Recovery extension stalled in early European trading at pivotal 1.1822 barrier (Fibo 61.8% of 1.1879/1.1730 downleg/4-hr cloud top) with rising concerns over Catalonia weighing on single currency. Increased downside risk could be expected on sustained break below 4-hrr cloud base (1.1774) which would attract key n/t support at 1.1730 for retest. Bullish scenario requires sustained break above 1.1822 to signal further recovery and expose barriers at 1.1851 (daily Kijun-sen) and 1.1879 (12 Oct high). With no releases from the EU today, technicals and situation in Catalonia are expected to be Euro's main drivers today.

Res: 1.1800, 1.1822, 1.1851, 1.1879

Sup: 1.1774, 1.1730, 1.1702, 1.1669

USDJPY Neutral Both In The Short- And Medium-Term

USDJPY is neutral both in the short- and medium-term. A broad range of (roughly) 108 and 114 has been formed since March and this is highlighted by a lack of direction in the major moving averages (50,100 and 200-day). Price action in the near-term since September 20 shows a consolidation range between 111.46 and 113.43.

USDJPY is currently trading in the upper end of the broader range. Short-term downward pressure has weakened and there is a positive undertone in the market as indicated by the RSI and MACD (both in bullish territory).

Support is being provided by the 200-day MA, currently at 111.75. Dropping below this would target the mid-point of the medium-term range at the key 111 level. Further weakness would push prices towards the lower end of the range at 108. Based on price action during the past six months, this area has been rejected, thus making it a strong support level. A drop below it would change the broader trend to bearish from neutral.

USDJPY has been firm in the past couple of sessions with risk clearly tilted to the upside. Breaking out of the 114 level and top of the range area would give scope to target the 118.66 peak from December 2016. Such a move would change the broader trend to bullish.

Despite the current positive tone in USDJPY, the short- and medium-term trend remains neutral

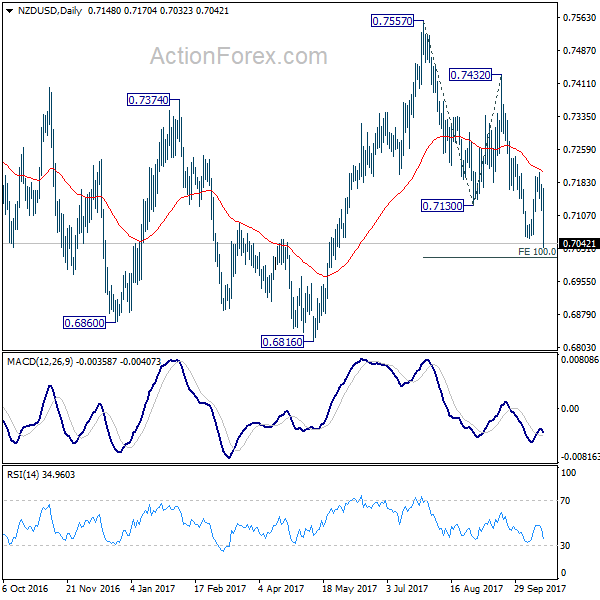

NZDUSD Sees Increased Downside Pressure

NZDUSD has shifted its near-term bias to bearish after dropping sharply to break key support at 0.7055. The odds are high for a move towards the next major low in the 0.6800 area.

On the 4-hour chart, RSI has fallen into bearish territory below 50, indicating momentum is tilted to the downside. Price action is currently below the 20 and 50-period moving averages, which also highlights increased downside pressure in the market.

The market has been in a downtrend since falling from the July peak of 0.7557. NZDUSD needs to rise back above key resistance at 0.7200. From here, the focus would shift back to the upside to target the next resistance level at 0.7343 and ahead of the 0.7434 high.

NZDUSD is at risk of putting in another lower top at 0.7210 if price action continues to fall below 0.7055.

Kiwi Sinks As Peters Supports Labour Party, Aussie Slips As China’s Growth Softens

A day after China's twice-in-a-decade Communist Party Congress commenced, statistics out of China showed that the economy continued to grow above the government's annual target, giving more confidence on President XiJinping's leadership. However, the expansion was slightly softer relative to the previous quarter, with the Australian dollar falling slightly in the wake of the data. In New Zealand, the Labour Party looks set to govern the country pushed the kiwi to a near five-month low.

According to the National Bureau of Statistics of China, the second-largest economy grew in line with expectations by 6.8% y/y in the third quarter, at a slightly slower pace than in the previous quarter as the government put extra efforts to cool the property market and limit debt-related risks. However, markets remained positive on the country's economic outlook with PBOC Governor Zhou Xiaochuan saying that GDP growth could reach 7.0% in the second semester of 2017.

Other data showed that Chinese industrial production climbed by 0.6 percentage points to 6.6% y/y in September, surpassing the forecast of 6.2%, whereas investments on equipment fell short of expectations, decreasing by 0.3 percentage points to 7.5% y/y, and missing projections of a rise by 7.7%.

The Chinese yuan retreated against the dollar, with dollar/yuan rising to a ten-day high of 6.6417 before it fell back to 6.6234.

In Europe, the focus is on Catalonia, with markets eagerly anticipating whether the Catalan leader, Charles Puigdemont, would step back from his symbolic independence declaration – Madrid set him a deadline for today at 0800GMT. The Spanish Prime Minister, Mariano Rajoy, warned Puigdemont on Wednesday to “act sensibly” in order to avoid the implementation of the direct rule which would give the right to the Spanish government to suspend the region's autonomy.

The euro, though, continued its uptrend during the Asian session, approaching a one-week high of $1.1821 after Reuters polls indicated that the ECB will announce on October 26 its decision to start trimming its asset-buying program in January. Recall that the plan was for the monthly purchases to drop from the current 60 billion euros to 40 billion. However, there is still doubt whether the plan would extend for six or nine months.

The pound was mainly flat around $1.3195 ahead of retail sales figures during the European session. The UK Prime Minister is also expected to attend the EU summit in Brussels later today (which concludes on Friday), where European leaders will discuss the progress in Brexit negotiations.

The dollar index was ranging around 93.32 after posting moderate gains earlier on the back of higher Treasury yields.

Dollar/yen was moving sideways at 112.95.

In New Zealand the leader of the kingmaker First Party, Winston Peters, announced his decision to support the opposition Labour Party to form a government, declaring Jacinda Ardem the next Prime Minister – she will hold the role for the next three years. The kiwi tumbled, reaching a near five-month low of $0.7037, losing 1.41% on the day.

On the other hand, the aussie recorded gains during the session in the wake of better-than-expected employment data that were partially lost after China's GDP growth appeared softer. Note that China is the largest export partner of Australia. Employment in Australia increased by 19,800 people, exceeding the forecast of 15,000 but remaining below the previous mark of 53,000 (downwardly revised from 54,200). The unemployment rate declined to 5.5%, a level seen before in March 2013, while analysts expected the figure to remain at August's rate of 5.6%.

Turning to commodities, oil prices moved lower on Thursday, while gold stood taller. WTI crude was down by 0.35% at $51.86 per barrel and Brent fell by 0.33% to $57.97. Gold was up by 0.13% at $1,2820 per ounce.

XAUUSD Analysis: Tries To Cross 61.8% Fibo

Despite release of negative data about the American housing market growth, the exchange rate continued to move to the bottom, in the process crossing a combination of the weekly S1 and the lower support line of senior ascending channel. At the moment, the pair is testing the 61.8% Fibonacci retracement level at 1,278.98. It seems that pressure from the slipping 55-, 100- and 200-hour SMAs should eventually push the pair through that barrier. Afterwards, the pair would face no obstacles on its way up until the weekly S2 at 1,265.92. On the other hand, daily chart clearly indicates that an area near 1,276.34 represents location of the 100-day SMA. From this perspective, it seems that the pair is going to make a temporary rebound.

Euro Tumbles as Spain Going to Suspend Catalonia Autonomy, Kiwi Dives as Labour Forms Coalition

This is a quick update.

Euro tumbles sharply while Yen jumps on as political risks come back to markets. Passing the deadline imposed to Catalan leader Carles Puigdemont, Spanish government said they will "continue with the procedures set out in Article 155 of the Constitution to restore the legality of self-rule in Catalonia." That is, the Spanish Government is going to suspend autonomy of Catalonia.

On the other hand, Puigdemont refused to withdraw the declaration of independence. And Puigdemont said that he will still go on with the declaration unless Madrid agrees to talk. Puigdemont said that "if the central government persists in blocking dialogue and continues its repression, the Catalan Parliament may proceed, if it considers it appropriate, to approve a formal declaration of independence."

Euro reverses much gains against Yen and Dollar. But still, EUR/JPY is staying in range and keeping intraday bias neutral.

New Zealand Dollar plunges today on news that New Zealand First would be forming a coalition with the Labour Party. And Jacinda Ardern will become the next Prime Minister. An important to note is that both Labour and NZ First propose reduction in net immigrations and reform on the RBNZ. Cutting immigration is seen as a factor that will drag on economic growth. Also, Labour-led government would likely boost social spending and push to add full employment to RBNZ's mandate. And the overall effect is prolonging RBNZ's accommodative policy.

NZD/USD dives to as low as 0.7032 so far today. The break of 0.7055 support confirms resumption of whole decline from 0.7557. NZD/USD should now target 100% projection of 0.7557 to 0.7130 from 0.7432 at 0.7005 first. And, sustained break there will pave the way to retest 2017 low at 0.6816.