Sample Category Title

USD/JPY Temporary Decrease?

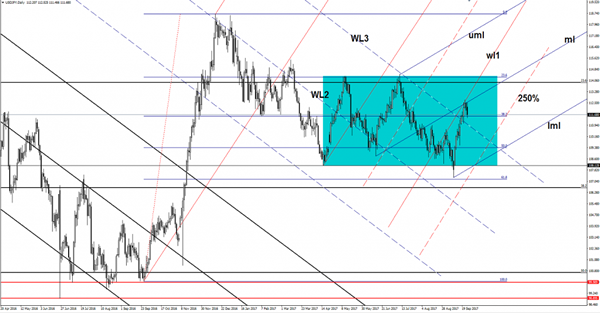

The currency pair has dropped in the start of the week and resumes the Friday's bearish candle. USD failed to hold the pair higher even if the dollar index has managed to climb higher. The minor retreat is natural after the rejection from an important confluence area, we'll see what will happen because has reached an important horizontal support.

Price continues to move in range on the short term, but I really hope that we'll have a clear direction very soon because cannot move sideways forever.

The Yen increases as the Nikkei stock index has found strong resistance and now slips lower. The JP225 was expected to drop a little after the amazing rally, I've said in the previous reports that the index should drop to retest the 20058 static support (resistance turned into support).

Technically, the JP225 is expected to climb much higher in the upcoming period after the breakout above the 20320 former high despite a minor drop.

Price failed to take out the resistance from the confluence area formed at the intersection between the first warning line (wl1) of the ascending pitchfork with the median line (ml) of the blue ascending pitchfork.

Now is pressuring the 38.2% retracement level, a valid breakdown will confirm a further drop towards the WL3 and towards the 250% Fibonacci line.

AUD/NZD Second Chance To Short

Last week's AUD/NZD cut and reverse played out nicely and with this little Aussie rally to open the week, I wanted to highlight an opportunity to get in if you missed the boat the first time around.

Click the link in the opening paragraph and take a look at the original setup, but it's all about the following daily support/resistance zone:

AUD/NZD Daily:

The significance of the zone is pretty straightforward, but I've marked the swing swing high top that I'm using just to make it clear.

You can see that after failing to hold above the zone, price dropped through. But now that price has rallied back into the zone to start the week, could this be the final retest before the pair really rolls over?

Now zoom into the hourly chart:

AUD/NZD Hourly:

I've marked the same level that we were shorting in the blog I linked to above and as you can see, price is back retesting the level again.

As long as price is below this level (which is the middle of the daily zone acting as resistance anyway), then shorts are still in play.

If this level does hold, I expect some nice momentum to come into the market and really push us lower.

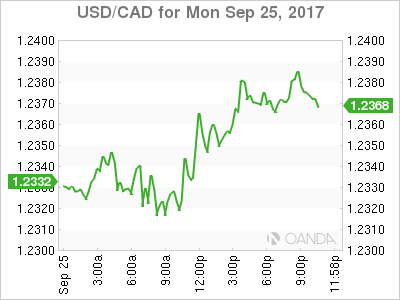

USD/CAD Canadian Dollar Lower Despite Surge In Oil Prices

The Canadian dollar depreciated on Monday hit by rising risk aversion as geopolitical events around the world dominated headlines. The German elections over the weekend showed that not even the largest member of the European Union is immune to the rise of eurozone opposition within its borders. The situation in North Korea continues to be elevated as Donald Trump’s tweets were called a declaration of war by the asian nation Foreign Minister.

Japanese Prime Minister Shinzo Abe has called a snap election of the lower house. Rising support as the result of the situation in North Korea has emboldened Abe to call for elections in October. The move is intended to weaken opponents, but like in the United Kingdom the move is a gamble that can backfire with a new national party offering the biggest threat. His major objective seems to be achieving a majority with the aim of reforming the constitution.

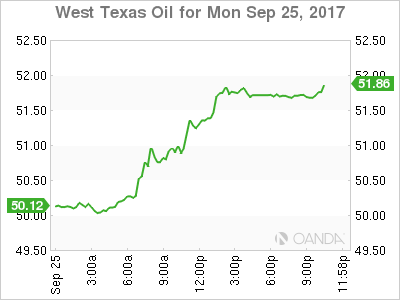

Oil is higher at the beginning of the week after the independence referendum vote in Northern Iraq could lead to disruptions in the oil rich area. The vote was not agreed to with the central Iraqi government and has drawn criticisms and threats of pipeline closures from other nations.

Trade representatives for Canada, Mexico and the United States are in Ottawa for the third round of talks of NAFTA renegotiation. Canadian negotiators have spoken out about the lack of details from the US team and despite good progress so far it is hard to predict when or how the talks will end.

The USD/CAD rose 0.205 percent on Monday. The currency pair is trading at 1.2364 as geopolitical risks are driving the market. Safe havens have been the biggest movers in the market. The potential disruption of Iraqi supply has put oil prices higher, but offered no support to the loonie.

This week will have few economic data points for CAD traders. Bank of Canada (BoC) governor Stephen Poloz will make his first appearance since the surprise September rate hike took the benchmark rate to 1.00 percent. The central bank was quiet ahead of announcing the monetary policy decision in stark contrast with the July meeting when it gave the market a clear heads up on its intentions. The market was expecting the 25 basis points rate hike to come in October, but the BoC thought it best to do it sooner rather than later with no warning. Poloz’s speech will be filled with the bank’s assessment of the economy that prompted the BoC to make that decision.

Later in the week the monthly GDP figures will be announced which could validate Mr Poloz’s eagerness to hike. A slowdown in growth could also raise question marks about his decision given that as expected the European Central Bank (ECB) and the U.S. Federal Reserve did not touch their benchmark rates. The Fed did finally announce the details of its balance sheet reduction program. December will be once again host the most important meetings of the year for most central banks. The Fed could hike a third time, but it all depends on the economic performance in the third quarter.

Energy in the US rose by 3.029 in the last 24 hours. The price of West Texas Intermediate is trading at $51.73 due to comments about a rebalancing of the market after the production cut agreement between the Organization of the Petroleum Exporting Countries (OPEC) and other major producers. The situation in Iraq, where an independence referendum took place on Monday. Iraqi Kurds are voting against the wishes of the central government and other nations. Turkey is on alert and has threatened to cut the pipeline taking Northen Iraqi oil to market.

Market events to watch this week:

Tuesday, September 26

10:00am USD CB Consumer Confidence

Wednesday, September 27

8:30am USD Core Durable Goods Orders m/m

10:30am USD Crude Oil Inventories

4:00pm NZD Official Cash Rate

4:00pm NZD RBNZ Rate Statement

Thursday, September 28

8:30am USD Final GDP q/q

8:30am USD Unemployment Claims

Friday, September 29

4:30am GBP Current Account

8:30am CAD GDP m/m

War Games

North Korea called Trump's recent comments a "declaration of war" and vowed to respond as the rhetoric ramps up. The US replied that Trump's comments were not a declaration of war. The Japanese yen was the top performer, closely followed by gold,while the New Zealand dollar lagged. The BOJ minutes are due later. Watch out for Yellen's Tuesday speech on inflation and monetary policy at 14:45 Eastern (19:45 London time).

The words 'North Korea' and 'war' set off algos Monday and a wave of selling in yen crosses. USD/JPY fell as low as 111.48 from 112.15. The Swiss franc and gold also jumped on the headlines and didn't retrace.

The problem with the North Korea story lately is that there is no ebb and flow. You would expect some rhetoric and then something to cool it off but neither side seems capable of diffusing tensions. Instead, the series of insults and threats continues. The comments echoed especially loudly as they emerged during US market hours. North Korea's foreign minister spoke early in New York trade and that meant extra attention in markets. Previously, the main rhetoric was limited to the weekend. Inevitably, the talk will cool down but it's tough to fade the trend at the moment against the risk of a tweet or statement at any moment.

Politics Galore

Separately, politics are dominating markets. Merkel's disappointing election showing and the risk of fractured or failed coalitions in Germany hurt the euro. US Congress is haggling over a healthcare proposal that seems dead and a tax proposal that's still unclear. In Japan, the snap election raises new risks. Brexit is never ending. It's a veritable minefield with tape bombs landing constantly and the threat of real bombs. That makes a good argument for paring risk until there is more clarity.

Coming up in Asia-Pacific trading, the minutes of the July 19-20 BOJ meeting will be released but the yen is more-likely to driven by comments from Abe and developments in North Korea.

Gold Starts Off Week With Strong Gains

Gold has started the trading week with gains, pushing above the $1300 level. In North American trade, the spot price for an ounce of gold is $1308.47, up 0.92%. There are no US economic releases on the schedule, but FOMC member William Dudley spoke earlier, and we'll also hear from Charles Evans and Neel Kashkari. On Tuesday, the US releases CB Consumer Confidence and New Home Sales. Federal Reserve Chair Janet Yellen will speak at an event in Cleveland.

Federal Reserve policymakers have been divided over a rate hike in December, which would mark a third rate increase in 2017. With no clear message from the Fed, the markets really don't know what to expect, and fed futures have priced in a December hike at 55%. On Monday, New York Fed President William Dudley made a strong case to raise rates. Dudley cited a soft US dollar and strong global growth as reasons why inflation would increase and also translate into stronger wage growth. Dudley said he expects inflation to reach the Fed's target of 2% in the "medium term", and predicted that the Fed would continue to gradually remove monetary accommodation. In last week's rate statement, the Fed announced that it would reduce its $4.2 trillion balance sheet by $50 billion/mth, starting in October.

Germany held a national election on Sunday, and the markets are following the results with caution. Angela Merkel's CDU won 33% of the vote in the German election, which means that Merkel will have to enter arduous negotiations with other parties in order to form a coalition government. The center-left SFD, which won 20% of the vote, has already said it will not join the CDU, so Merkel has her work cut out for her. The far-right AFD ran on a far-right, anti-immigrant platform, and the party's surge in support has sent shock waves in Germany and across Europe. The AFD cannot be considered as a coalition partner, which leaves the Greens and the pro-business FDP party as the most likely configuration. However, the FDP has insisted on the powerful finance portfolio and will likely try to reduce German transfer payments to the European Union. If negotiations become deadlocked, gold prices could rise in response to nervous markets.

German Election Monitor: Difficult Government Formation Ahead

Angela Merkel has secured her fourth term in office as her Conservatives (CDU/CSU) remained the largest party with 33.0%, followed by the Social Democrats (SPD) with 20.5%. However, both parties registered significant losses in their vote shares to the benefit of the euro-sceptic AfD party, which will become the first right-wing nationalist party to enter the Bundestag since the 1950s, with a vote share of 12.6% (see Chart 1). Although the AfD outperformed previous polls, its chances of realising any of its policy goals (Table 2) remain very slim, as all other parties have ruled out any cooperation with it. Together with the Greens and the Left, the Liberals (FDP) will also re-enter the Bundestag, taking the total number of parties in parliament from five in 2013 up to seven (Chart 2).

In line with similar trends observed in the Dutch and French elections this year, Election Day brought a dire defeat for the SPD, which recorded its worst ever parliamentary election result. The outcome now leaves only two viable coalition possibilities that can obtain a majority: another grand coalition of CDU/CSU and SPD or a 'Jamaica' coalition of CDU, FDP and the Greens (Table 1). However, as the SPD leadership currently rules out another grand coalition under Merkel because of its disappointing election result, a Jamaica coalition seems increasingly likely in our view. Note, however, coalition talks will be difficult and take several weeks or even months in light of the more fragmented political landscape, and the new government composition might not be known before November or December this year.

The election result means that we will probably enter a period of heightened political uncertainty in Germany over the coming weeks as coalition talks drag on. However, we expect that a solution on a government formation under Merkel as Chancellor will eventually be found before the end of the year. Hence, we believe that any adverse market reaction will be short-lived given the high degree of policy continuity under a CDUled coalition and the AfD's political isolation in parliament. The CDU plans to increase spending on infrastructure and lower taxes should strengthen domestic demand-driven growth in the future, in our view, and support the economic recovery in the eurozone and a gradual scaling back of ECB stimulus over coming years. However, difficult coalition talks ahead raise the bar for any swift progress on potential eurozone reforms as initiated by Emmanuel Macron, also in light of the FDP's more conservative stance on fiscal risk-sharing.

Euro Extends Decline after German Elections; Oil Jumps to Fresh Multi-Month Highs

The euro continued to be dogged by concerns about the outcome of the German elections, extending its losses in European trading, while a similarly disappointing election outcome in New Zealand caused the kiwi to be the day's worst performing major currency. The US dollar was firmer as the yen came under pressure after the Japanese prime minister called a snap general election. Oil prices meanwhile rose to fresh highs after major producers said the market was rebalancing.

The prospect of prolonged uncertainty as Angela Merkel and her CDU/CSU alliance try to form a coalition with two smaller parties pulled the single currency deeper into the red in Monday's European session. The stronger-than-expected showing for the far-right anti-immigrant AfD party has reignited fears about the rise of populist parties in Europe, while a potential coalition with the FDP and the Greens could force Merkel to take a tougher stance on further EU integration.

Further weighing on the euro today was weaker-than-expected German business survey data from the Ifo Institute. The Ifo's business climate index missed forecasts of 116.0 to decline to 115.2 in September from the prior 115.9. The current conditions index also missed estimates to fall to 123.6 in September, while the Ifo's expectations index dropped from 107.8 to 107.4.

The euro's woes worsened after ECB President Mario Draghi said that the economic recovery has yet to "translate more convincingly into stronger inflation dynamics". Speaking before the European Parliament's Economic and Monetary Affairs Committee, Draghi added that volatility in the exchange rate was "a source of uncertainty which requires monitoring".

The single currency fell back below the key $1.19 level, hitting a session low of $1.1861. It was also lower against the yen and the pound at 133.27 yen and 0.8788 pounds.

The greenback was unable to retain its Asian session highs against the yen but remained up on the day, and was last trading at 112.20. The dollar index was also firmer to stand at 92.47, up 0.3% from Friday's close. The US currency was supported by relatively hawkish remarks from New York Fed President William Dudley. Speaking at a college in New York, Dudley said he expects inflation to "rise and stabilize around the 2 percent objective over the medium term" as the effect of temporary factors fade and a weaker dollar pushes up import prices.

The yen weakened slightly after the Japanese prime minister, Shinzo Abe, said he will dissolve parliament on September 28 and call early elections in October (slated for the 22nd). Earlier today, Abe announced a fiscal spending package amounting to two trillion yen to stimulate the Japanese economy.

The pound pared back some of Friday's losses when it tumbled after Prime Minister Theresa May's highly anticipated speech on Brexit failed to provide enough clarity on what kind of a deal the UK will be seeking with the EU once it leaves the bloc. However, hopes that the speech has done enough to unblock the stalemate in the negotiations lifted sterling against the dollar today. The pound last traded at $1.3514, down from a session high of $1.3570 but up 0.2% on the day, as the fourth round of talks between the EU and the UK got underway.

The New Zealand dollar was the day's worst performer as an inconclusive election outcome weighed on the currency. Saturday's general election left the country's third largest party, New Zealand First, holding the balance of power as it will have to decide whether it wants to form a government with the ruling National Party or with the opposition Labour. The kiwi fell to a one-week low of $0.7250 during Asian hours but managed to stabilize around $0.7275 by late European trading, though this was still 0.9% lower on the day.

Oil prices resumed their uptrend on Monday as investors became more optimistic about the outlook for the market. On Friday, OPEC and other major oil producers signalled they will likely decide in late 2017/early 2018 whether to extend the current output cap deal but said the market is now "evidently well on its way towards rebalancing." WTI crude hit a 4-month high of $51.43 a barrel but Brent crude fared even better, surging to a 9-month high of $58.05 a barrel.

EUR/USD On The Way Down

The currency pair has opened with a gap down in the morning, signaling that the bears are in control on the short term. Price has come higher to close the morning gap, but has failed. EUR/USD is trading in the red right now and seems too heavy to be stopped.

Price erased the morning gains and could hit fresh new lows till the end of the day as the dollar index could breakout above the 92.49 static resistance. The dollar index moves somehow sideways on the short term, signaling a potential reversal. The behavior changed on the USDX as the rate has started to make higher lows, but we still need a confirmation that the index will really start a broader rebound, which will lead the USD much higher versus all its rivals. The Euro dropped further also because the German Ifo Business Climate decreased from 115.9 to 115.2 points, even if the estimate 116.0 points.

The price failed to close above the upper median line (uml) of the minor descending pitchfork and above the UML and now is going down again. Price also failed to retest the upper median line (uml) in the last attempt, so the bearish movement is natural.

It could be attracted by the confluence area formed between the median line (ml) with the ML of the ascending pitchfork. EUR/USD is narrowing right now, but I hope that we'll have a significant move very soon.

Brent Oil At New Peaks

Price rallied aggressively and jumped much above the median line (ML) of the major ascending pitchfork, signaling that is strongly bullish. Has broken above the 150% Fibonacci line (descending dotted line) and above the upside line (uml) of the up channel. A retest of the broken levels will signal a further increase in the upcoming period.

Brent is almost to hit the $58.00 per barrel, it wasn't reached since July 2015, so the price could touch new peaks in the upcoming period.

AUD/USD Imminent Breakdown

Price increased a little today, but wasn't able to reach the 0.7985 Friday's high. It seems undecided right now because the USDX has managed to increase a little. Could retest the lower median line (LML) again, remains to see if we'll have a breakdown or a bounce back. A breakdown is favored if the USDX will jump and will stabilize above the 92.49 static resistance.