Sample Category Title

Rising Gasoline Prices Push Up Canadian Inflation in January

Canadian consumer price inflation accelerated to 2.1% (year-on-year) in January, well ahead of the consensus expectation for a 1.6% increase. Prices rose 0.9% month-on-month (compared to consensus call for 0.4%).

Higher prices at the gasoline pump were the main contributor to the outsized gain. Gasoline prices were up 20.6% year-on-year. The sharp rise in the price of gasoline and other energy goods and services reflects both the rebound in oil prices, as well as new carbon levies in Alberta and Ontario. In Alberta, gasoline prices were up 33.9% while natural gas prices rose a toasty 42.3%.

Despite the sharp move higher in headline inflation, core inflation measures remained benign: CPI-common fell to just 1.3% from 1.4%, CPI-median remained unchanged from a downwardly revised 1.9%, and CPI-trim edged up to 1.7% (from 1.6% previously). All core measures are year-over-year.

The other category to see a notable acceleration in prices was the shelter index, which accelerated to 2.4% from 2.1% in December (y/y). The uptick was mainly due to rising homeowners' replacement costs, which rose 4.3% in the month.

On the other side, Canadians are paying less for food. Food prices declined 2.1% in January from the same time last year, even more than the 1.3% decline in December.

Key Implications

As far as headline inflation is concerned, oil prices give and they take away. Having said that, the sharp rise in inflation is less than meets the eye, reflecting the turnaround in the price of energy from its nadir at the beginning of 2016. While the rebound is likely to keep headline CPI above the 2.0% mark over the coming months, little of it is expected to pass through to core inflation, which should keep the Bank of Canada on the sidelines.

The impact of carbon levies will nonetheless remain a component to watch for on headline prices. Since these measures are meant to raise the price of carbon year-after-year, they will not fall out of the inflation data the way a one-off price increases would. Over time, substitution away from energy products should reduce the impact of gains in energy prices on inflation, but this will take time to show up.

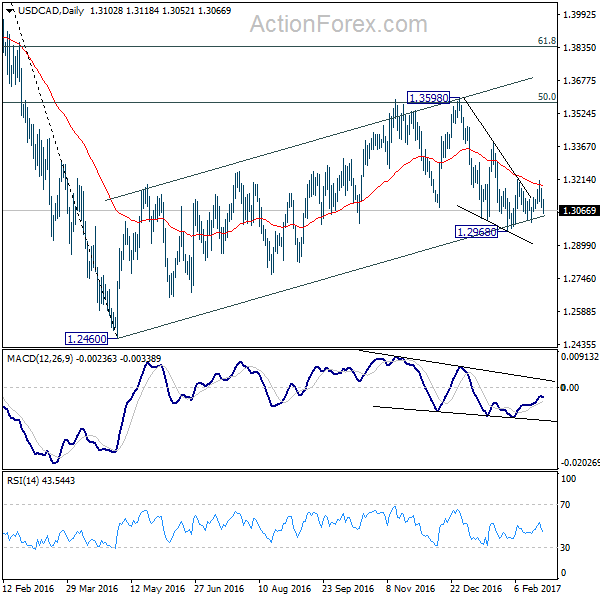

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3067; (P) 1.3118; (R1) 1.3154; More...

USD/CAD dips sharply today but stays in range of 1.2968/3211. Intraday bias remains neutral first. On the upside, break of 1.3211 resistance will argue that fall from 1.3598 has completed at 1.2968. And more importantly, rise from 1.2460 is still in progress. In that case, intraday bias will be turned back to the upside for 1.3598 and above. On the downside, below 1.2968 will revive the case that rise from 1.2460 is completed and turn outlook bearish for this low. Overall, choppy rise from 1.2460 is still seen as a corrective move.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg could be completed at 1.3598 and fall from there is tentatively seen as the third leg. Break of 1.2460 will target 50% retracement of 0.9460 to 1.4689 at 1.2075 before completing the correction. In case of another rise, we'd look for reversal signal above 61.8% retracement of 1.4689 to 1.2460 at 1.3838.

CAD Surges on Strong Inflation Reading

Canadian dollar surges in early US session after stronger than expected inflation data. Headline CPI jumped 0.9% mom and 2.1% yoy in January. That's way above expectation of 0.3% mom, 1.6% yoy. Meanwhile, BoC CPI core also rose 0.5% mom and pushed the annual rate higher to 1.7% yoy. The Loonie was mildly troubled by WTI crude oil's breakout failure. But much support is seen from the inflation reading. Released earlier today, UK BBA mortgage approvals rose to 44.7k in January.

Trump called China "Grand Champions" of currency manipulation

In US, the markets are still waiting for details of president Donald Trump's economic policies, including that "phenomenal" tax reform. It's reported that Trump told "some two dozen" heads of major companies that he has plans to bring millions of jobs back to the US. He was quoted as saying, "we are going to find out how we bring more jobs back". Without more details unveiled yet, the market is awaiting a joint session of Congress on February 28. But at the same time, Trump has started his verbal attack on other countries again. He labeled China as the "grand champions" of currency manipulation. However, his Treasury secretary Steven Mnuchin said on Thursday that the administration isn't "making any judgements" on China's currency yet. The messages out of the administration are so far rather confusing.

RBA governor Lowe expects a period of stability in interest rate

RBA governor Philip Lowe said today that he expects a "period of stability" in interest rates. He pointed out that "the issue we're discussing, internally, is how much extra fragility would that mean in the economy with household debt already at a record high." In particular, he throw out that question that "is it really in the national interest to get a little bit more employment growth in the short run at the expense of creating vulnerabilities which would become quite dangerous in the medium term?" In his view, lowest interest rate will encourage people to borrow more for "housing" but not "consumption.

Regarding economic outlook, Lowe said "the picture remains quite complicated." And, "in parts of the country that have been adjusting to the downswing in mining investment or where there have been big increases in supply of apartments, housing prices have declined. In other parts, where the economy has been stronger and the supply-side has had trouble keeping up with strong population growth, housing prices are still rising quickly."

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3067; (P) 1.3118; (R1) 1.3154; More...

USD/CAD dips sharply today but stays in range of 1.2968/3211. Intraday bias remains neutral first. On the upside, break of 1.3211 resistance will argue that fall from 1.3598 has completed at 1.2968. And more importantly, rise from 1.2460 is still in progress. In that case, intraday bias will be turned back to the upside for 1.3598 and above. On the downside, below 1.2968 will revive the case that rise from 1.2460 is completed and turn outlook bearish for this low. Overall, choppy rise from 1.2460 is still seen as a corrective move.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg could be completed at 1.3598 and fall from there is tentatively seen as the third leg. Break of 1.2460 will target 50% retracement of 0.9460 to 1.4689 at 1.2075 before completing the correction. In case of another rise, we'd look for reversal signal above 61.8% retracement of 1.4689 to 1.2460 at 1.3838.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:30 | GBP | BBA Mortgage Approvals Jan | 41.9K | 43.2K | ||

| 13:30 | CAD | CPI M/M Jan | 0.30% | -0.20% | ||

| 13:30 | CAD | CPI Y/Y Jan | 1.60% | 1.50% | ||

| 13:30 | CAD | BoC CPI Core M/M Jan | -0.30% | |||

| 13:30 | CAD | BoC CPI Core Y/Y Jan | 1.60% | |||

| 15:00 | USD | New Home Sales Jan | 575K | 536k | ||

| 15:00 | USD | U. of Michigan Confidence Feb F | 96 | 95.7 |

Gold Glimmers as Uncertainty Mounts

The heightened political risks in the U.S and Europe have revived an appetite for safe-haven assets with Gold becoming an investor's popular choice. This metal remains firmly tilted to the upside on the daily charts and the rapidly fading expectations of a U.S interest rate increase in March has inspired bullish investors to propel prices higher. With prices already charging to a fresh three-month high above $1255, further Dollar weakness could fuel the upside momentum that sends the metal towards $1260. Although the prospects of higher US rates in 2017 may cap gains on Gold in the longer term, bulls remain in control in the short term with the current trajectory pointing to further upside. From a technical standpoint, previous resistance around $1250 could transform into a dynamic support that encourages a further incline higher towards $1260.

Stock markets gripped by unease

Global stocks were exposed to downside shocks on Friday as the growing concerns over U.S trade policies impacting regional economies sparked waves of risk aversion. Asian shares were heavily depressed during early trading on Friday with the bearish contagion infecting European markets. The visible jitters created from the events in Europe and growing unease over the Trump developments could place Wall Street under renewed selling pressures moving forward. Although global stocks have repeatedly hit record highs, there remains some scepticism over the sustainability of the rally with a selloff on the table if Trump fails to deliver his market shaking tax cuts and fiscal policies.

Dollar under renewed pressure

The Greenback lost its attitude this week after the Fed minutes failed to convince participants that US rates would be increased in March. Uncertainty originating from the Trump developments has fuelled the Greenback selloff with the Dollar Index currently trading around 100.80 as of writing. Although it is visibly clear that economic data and overall sentiment towards the U.S remains bullish, the uncertainty and politics continue to cap Dollar gains. The downside momentum on the Dollar Index could drag prices lower towards 100.50. A technical breakdown below 100.50 may open a path to the next relevant support at 100.00.

Commodity spotlight - WTI Oil

Oil price volatility remains a dominant theme this quarter as participants re-evaluate the supply and demand dynamics that has driven the global oil markets. Although the rising optimism over OPEC members' cutting oil production has attributed to WTI's impressive appreciation this quarter, the fears of U.S shale obstructing OPEC's effort to cutting supply could limit gains on oil. Much attention will be directed towards the ongoing OPEC and U.S shale developments in the coming weeks with any signs of the oversupply woes resurfacing exposing WTI to steep losses. WTI remains pressured below $55 with weakness potentially encouraging a selloff lower towards $52.

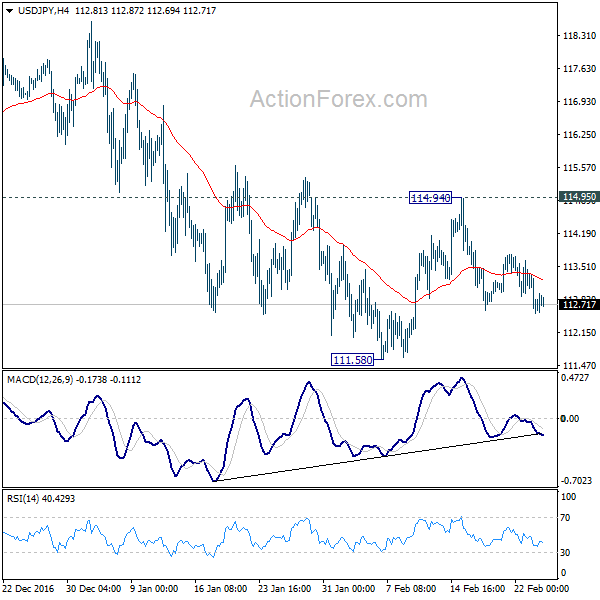

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.29; (P) 113.87; (R1) 113.20; More...

Intraday bias in USD/JPY remains neutral for the moment. Corrective fall from 118.65 could extend lower through 111.58. But we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, above 114.94 resistance should confirm completion of pull back from 118.65. In such case, intraday bias will be turned back to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

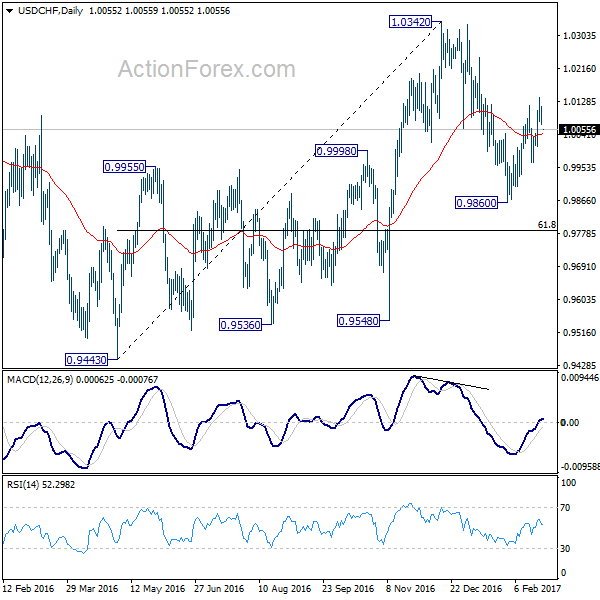

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0038; (P) 1.0077; (R1) 1.0101; More.....

Intraday bias in USD/CHF remains neutral for the moment. With 0.9966 minor support, further rise is still expected. Above 1.0140 will target 1.0342 high. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. Meanwhile, break of 0.9966 will indicate completion of the rebound. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

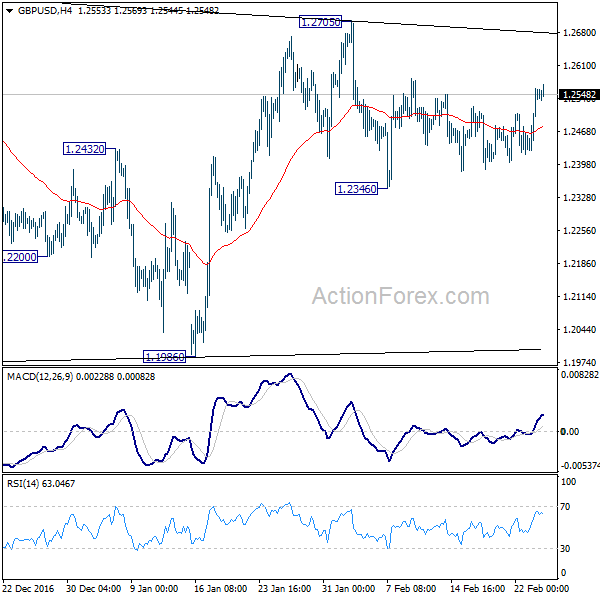

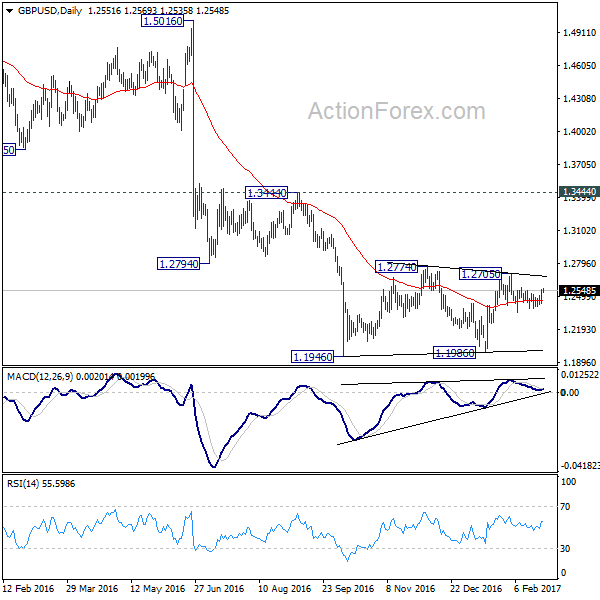

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2469; (P) 1.2514; (R1) 1.2602; More...

GBP/USD continues to gyrate in range of 1.2346/2705. Intraday bias remains neutral at this point. Price actions from 1.1946 are viewed as a consolidation pattern, with rise from 1.1986 as the third leg. In case of another rise, we'd expect upside to be limited by 1.2774 to bring larger down trend resumption. On the downside, below 1.2346 will revive the case that such consolidation is completed at 1.2705 already. In that case, intraday bias will turn back to the downside for retesting 1.1946 low.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

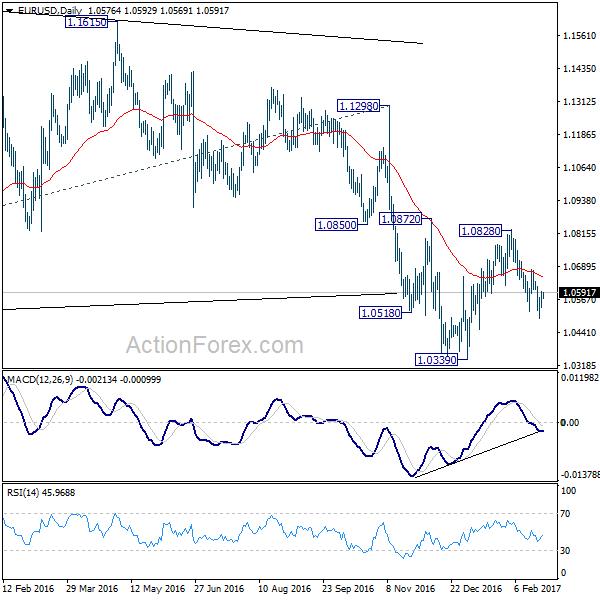

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0547; (P) 1.0571 (R1) 1.0605; More.....

EUR/USD's recovery from 1.0493 temporary low continues today but stays below 1.0678 resistance. Intraday bias stays neutral first with a mild bearish outlook. We're viewing fall from 1.0828 as resuming the larger down trend. Below 1.0493 will target 1.0339 low first. Break will confirm our bearish view and target parity. However, break of 1.0678 will dampen our view and turn focus back to 1.0828 resistance instead.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Euro Recovers Mildly in Directionless Markets

Euro recovers mildly today but remains the second weakest major currency for the week, next to Swiss Franc. Dollar, on the other hand, lost momentum again. Dollar index was repelled from 101.96 resistance and is back below 101 handle. Overall, the financial markets are losing their directions. DJIA closed at another record high overnight, up 34.72 pts or 0.17%, at 20810.32. S&P 500 jumped to new high at 2368.26 but pared gains to close at 2363.81, just up 0.99 pts, or 0.04%. NASDAQ dropped for the second straight days and closed down -25.12 pts, or 0.43%. Treasury yields closed lower as recent sideway consolidation extends. Gold, however, extended recent rise to as high as 1254.8 so far today. WTI failed to break out from recent range and gyrates lower to 54.24.

It's reported that US president Donald Trump told "some two dozen" heads of major companies that he has plans to bring millions of jobs back to the US. He was quoted as saying, "we are going to find out how we bring more jobs back". Without more details unveiled yet, the market is awaiting a joint session of Congress on February 28. Separately, the new US Treasury Secretary Steve Mnuchin indicated that the White House wanted to pass "very significant" tax reform by August. He signaled that the tax plans, together with deregulation measures, would boost US GDP growth to at least 3% in as soon as next year. Note that the US has not recorded full-year growth of 3% since 2005, while growth in 2016 was 1.6%. But after all, markets are cautious as there is no detail on anything yet.

In Eurozone, ECB executive board member Peter Praet talked down recovery in the region. He noted that "the growth pattern is still very much conditional on a substantial degree of accommodation." And, he noted that "these economies are still fundamentally fragile so no complacency is the main message." Also, Praet warned that "the recent bouts of (political) uncertainty are a source of concern, and represent a downside risk to the economic outlook." On the other hand, Bundesbank head Jens Weidmann was more positive and he said that "the upturn in the euro zone has consolidated and is increasingly secure."

On the data front, UK will release BBA mortgage approvals in European session. Canada CPI will be the main feature in US session. US will release new home sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0547; (P) 1.0571 (R1) 1.0605; More.....

EUR/USD's recovery from 1.0493 temporary low continues today but stays below 1.0678 resistance. Intraday bias stays neutral first with a mild bearish outlook. We're viewing fall from 1.0828 as resuming the larger down trend. Below 1.0493 will target 1.0339 low first. Break will confirm our bearish view and target parity. However, break of 1.0678 will dampen our view and turn focus back to 1.0828 resistance instead.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:30 | GBP | BBA Mortgage Approvals Jan | 41.9K | 43.2K | ||

| 13:30 | CAD | CPI M/M Jan | 0.30% | -0.20% | ||

| 13:30 | CAD | CPI Y/Y Jan | 1.60% | 1.50% | ||

| 13:30 | CAD | BoC CPI Core M/M Jan | -0.30% | |||

| 13:30 | CAD | BoC CPI Core Y/Y Jan | 1.60% | |||

| 15:00 | USD | New Home Sales Jan | 575K | 536k | ||

| 15:00 | USD | U. of Michigan Confidence Feb F | 96 | 95.7 |

DAX Muted as Investors Looking for Cues

DAX Muted as Investors Looking for Cues

The DAX Index is quiet in the Friday session, as the index is down by 0.30%. Currently, the DAX is trading at 11,920.90 points. On the release front, there are no eurozone economic indicator, so it could remain a quiet day. On Thursday, the DAX briefly pushed across the symbolic 12,000 level, but has since retreated.

In tandem with other stock markets, the DAX shrugged off the Federal Reserve's January minutes. There were no dramatic hints as to the timing of the next move by the Fed. The most important comment was that policymakers believe that a rate hike "fairly soon" could be appropriate in order to head off an overheated economy. The minutes indicated that Fed policymakers remain confident that the central bank will raise rates gradually, given the strong performance of the US economy. At the same time, the minutes noted uncertainty about President Trump's fiscal stimulus plan but little concern over the risk of inflation. So the million dollar question of when the Fed will press the rate trigger remains unanswered. Although pressure is slowly building towards a move by the Fed, there does not appear a sense of urgency to raise rates at the next meeting in March. According to the CME Group, the odds of a March hike are only at 17%, while the likelihood of a hike in either May or June stands above 40%.

Investors are constantly looking for cues, but shouldn't count on the European Central Bank making any dramatic moves which will shake up the stock market. There's no arguing that the eurozone has recorded moderate growth and higher inflation in recent months. Nonetheless, the central bank appears in no rush to tighten monetary policy, which would be bullish for the euro. ECB President Mario Draghi will likely be reluctant to make any major moves which could entangle the ECB in hotly contested elections in France and Germany (France goes to the polls in April, followed by Germany in September). At the same time, "political risk" in Europe is affecting investor confidence and weighing on the euro and the stock market. In June, Britain stunned the continent by voting to leave the European Union, throwing British-EU relations into crisis mode. In France, Marine Le Pen, leader of the far-right National Front, is the front-runner in the first round and could conceivably be elected president. Le Pen wants to take France out of the eurozone and has promised a referendum on French membership in the EU. Germany's Angela Merkel, a pillar of stability on the continent, is in a tough election fight and voters may choose change rather than hand her a fourth term in office.