Sample Category Title

GBP/JPY Amazing Breakout

The GBP/JPY has rallied aggressively and has managed to resume the bullish movement. The pair has finally managed to breakout from the extended sideways movement and goes for the next upside target from the lower median line (LML) of the ascending pitchfork.

August Retail Sales Start Showing Storm Damage

Headline retail sales dropped 0.2 percent in August, as hurricane Harvey hit multiple categories. The July print was revised lower to 0.3 percent. The prognosis for PCE in Q3 GDP growth has certainly weakened.

Gas Prices and Shuddered Stores Impact August Sales

Advanced retail sales for August marked the beginning of several months in which retail sales data will show impacts from hurricane Harvey on Southeast Texas. Some early prepping by Floridians for Irma also may have been included in the surge of spending at grocery stores. Most sales showed steep declines from lost selling days at the end of the month, with auto sales showing the sharpest drop.

Downward revisions to the previous month added salt to the wound this morning. July's 0.6 percent rise first reported was revised to 0.3 percent, which wipes out some of the comforting buffer that Q3 PCE had built up to lessen the blow from the two major hurricanes that will inevitably cut into personal consumption growth in the GDP calculations. Control group sales also declined by 0.2 percent in August and the 3-month annualized rate of 1.1 percent is the slowest pace so far this year.

Auto sales were clearly the hardest hit in August. Sales of motor vehicles and parts declined 1.6 percent in August after a flat reading in July. The decline in auto sales trimmed 0.3 percentage points from headline growth, which was easily the largest drag from a single category in several months. Sales excluding motor vehicles were up slightly in August. The decline in auto sales eclipsed the boost from the 2.5 percent rise at gas stations. We were expecting gasoline sales to surge, due both to stocking up in storm affected areas and the surge in gasoline prices. Harvey slammed straight into the heart of the oil industry and several pipelines delivering fuel to the east coast were offline for several days, causing pump prices to rise in areas not directly hit by the storms.

August sales at building supply stores were somewhat of a wildcard, as Harvey made landfall on August 26, closing stores for the entire last week of August. While some rebuilding purchases may have been made in August, the 0.5 percent decline in building material sales on the month suggest most of that spending took place in September. Prepping for Hurricane Irma will also likely boost this category in September.

Sales were up for miscellaneous retail stores, grocery stores and eating and drinking places on the month, though non-store retailers' sales dropped on the month. Non-store retailers' sales, which include online shopping, surged 1.8 percent in July, so the August drop is likely payback. Amazon's 'Prime Day' was on July 10, which may have made for tougher month-tomonth comparisons in August. The category is up 8 percent over the year.

In the first of many indicators this fall to be impacted by hurricanes, the August retail sales report showed the surge in gasoline sales was erased by the lost business from other categories in August. In September, building supply stores will likely see much stronger sales as Houston and the entire state of Florida rebuild and recover from major back-to-back storms.

US Data Can’t Help Dollar Find a Solid Bottom

- European stock markets correct lower today with losses of up to 0.5%. US stock markets opened mixed with the Dow gaining some ground and the S&P and Nasdaq suffering small losses.

- Gertjan Vlieghe, one of the BoE's nine-strong rate-setting committee, said in a speech today that the base rate may need to rise "as early as the coming months". Previously, he has defended the central bank's programme of monetary stimulus.

- An improvised device was detonated on a London Underground train on Friday morning, injuring 22 people in what police say was a terrorist incident. Counter-terrorism officers took charge of the investigation and were seeking to establish who had planted the device on a packed commuter train during rush hour.

- An unexpected decline in August US retail sales and downward revisions to the prior two months mainly reflected weaker results at auto dealerships. Retail-control group sales, which are used to calculate GDP and exclude the categories of food services, auto dealers, building materials stores and gasoline stations, decreased 0.2% following a 0.6% advance

- US industrial production dropped unexpectedly by 0.9% M/M in August following an upwardly revised 0.4% M/M in July. Manufacturing production was down 0.3% M/M. The US empire manufacturing index declined less than forecast, from 25.2 to 24.4 (18 expected).

- There is a realistic chance of another Czech interest rate hike this year, partly due to an unexpectedly fast rise in wages, the central bank's monetary department director Tomas Holub was quoted as saying.

- EMU wages grew at their fastest rate in two years in Q2, increasing the chances that the ECB will set out plans next month to rein in its economic stimulus. Hourly labour costs rose by 1.8% in the April-June period, from a revised 1.4% in Q1, its highest growth since the first quarter of 2016, Eurostat said.

- "It is time to take a decision now on scaling back our bond purchases at the beginning of next year," ECB Lautenschlaeger said. "We need to think about how to bring our unconventional measures to an end. We need to look ahead and discuss what the exit might look like."

Rates

Core bonds lose more ground despite weak US eco data

Global core lost more ground today despite disappointing US eco data (retail sales, industrial production). US Treasuries nevertheless outperformed German Bunds because of these data. Today's session confirms that sentiment on core bond markets turned a corner compared to the Summer months. The main culprit for the decline in core bonds was BoE Vlieghe. He is by far the most dovish BoE-member, but in a speech he argued as well in favour of rate hike (in line with BoE communication yesterday). Both the Bund and the US Note future suffered a blow via the UK Gilt market (5-yr yield at one stage +12 bps). It makes the topic of policy normalisation in EMU and US back alive ahead of next week's FOMC meeting. US eco data mainly disappointed (only empire manufacturing better than forecast) but offered only temporary relief for the US Note future. Hawkish comments by ECB Lautenschläger (see headlines) marginally weighted on the Bund as well.

At the time of writing, changes on the US yield curve range between +0.2 bps (30-yr) and +1.5 bps (5-yr). The German yield curve trades 0.7 bps (30-yr) to 3.1 bps (5-yr) higher. On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 3 bps (Portugal).

Currencies

US data can't help dollar find a solid bottom

The dollar couldn't confirm tentative signs of a bottoming out process earlier this week. EUR/USD returned to the upper half of the 1.19 big figure. The move was reinforced by poor US retail sales and production data. USD/JPY (and EUR/JPY ) are in good shape, but this is mainly yen weakness as the Japanese currency suffers from higher US/EMU yields.

Overnight, North Korea launched a new missile over Japan. However, the multiple North Korean actions have diminishing impact on markets. Asian equity markets traded mixed, mostly even slightly stronger. USD/JPY spiked briefly below 110, but soon returned to the mid 110 area. The EUR/USD chart hardly showed any ripples.

There was no high profile eco news in Europe. European equities didn't suffer from the North Korea missile launch, but there were also no sustained gains. At the same time, US and European bond yields still trended cautiously higher. Contrary to what was the case of late , the euro this time profited more than the dollar. ECB's Lautenschlaeger said that it is now time to take a decision on scaling back QE. Her point of view is no surprise but it brought the ECB tapering story again in the spotlight. The hawkish comments from the UK were maybe also slightly more supportive for the euro than for the dollar. Whatever, EUR/USD returned to the mid 1.19 area going into the US session. The yen suffered quite heavily from higher US & EMU yields. USD/JPY jumped above 111. EUR/JPY even reached the highest level since end 2015.

The early morning US data were mixed. The US empire manufacturing remained strong, but August retail sales brought a big miss and a strong July report was downwardly revised. The August US production also declined sharply, but Harvey was to blame. The dollar lost some further ground, but the additional losses were modest given the substantial miss in the data . EUR/USD trades in the 1.1970 area. USD/JPY hovers around 110.85. Conclusion: There were tentative signs of a USD bottoming out prices earlier this week, but these are not yet confirmed. USD/JPY is testing the 111 resistance area but this is yen weakness rather than USD strength.

Sterling gets additional support as dove turns hawkish

Yesterday, sterling jumped sharply higher as the BoE minutes of the 13 September policy meeting revealed that a majority of MPC members expected that a gradual withdrawal of monetary stimulus is likely to be appropriate over the coming months in order for inflation to return sustainably to target. There were no eco data in the UK today. However, BoE's Vlieghe, a notorious dove within the MPC, gave a speech in London. Remarkably Vlieghe also supported the call for a rate hike. He even suggested that the equilibrium UK interest rate may be rising. This hawkish turn of a BoE dove evidently triggered further GBP gains. EUR/GBP dropped temporary below 0.88 and trades currently at 0.8825. Cable (currently 1.3575) jumped north of 1.36, supported by USD softness, too.

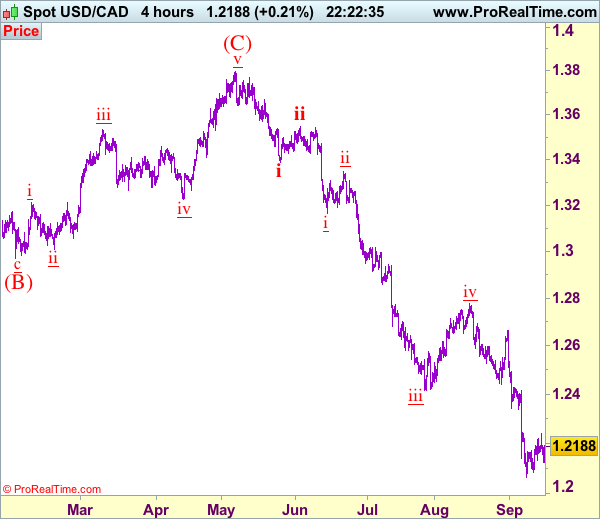

Trade Idea: USD/CAD – Hold short entered at 1.2240

USD/CAD - 1.2186

Trend: Down

Original strategy :

Sold at 1.2240, Target: 1.2080, Stop: 1.2240

Position: - Short at 1.2240

Target: - 1.2080

Stop: - 1.2240

New strategy :

Hold short entered at 1.2240, Target: 1.2080, Stop: 1.2240

Position: - Short at 1.2240

Target: - 1.2080

Stop:- 1.2240

As the greenback found support at 1.2121 today and has rebounded, suggesting further consolidation would take place, however, as long as indicated resistance at 1.2240 holds, bearishness remains for recent decline to resume after consolidation, below said support at 1.2121 would signal the rebound from 1.2061 has ended, bring retest of this level later, below there would confirm recent decline has resumed and extend weakness towards psychological support at 1.2000 but loss of downward momentum should prevent sharp fall below 1.1950-60, bring rebound later. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

In view of this, we are holding on to our short position entered at 1.2240. Above 1.2240-50 would risk rebound to 1.2300 but only break there would defer and signal a temporary low has been formed, bring a stronger rebound to 1.2335-40, however, upside should be limited to resistance at 1.2429 and price should falter well below 1.2490-00.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

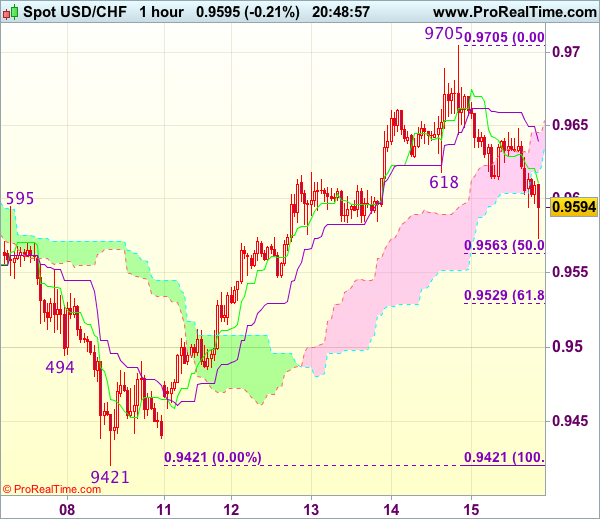

Trade Idea Update: USD/CHF – Target met and stand aside

USD/CHF - 0.9578

Original strategy :

Sold at 0.9680, met target at 0.9580\

Position : - Short at 0.9680

Target : - 0.9580

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has slipped again after meeting renewed selling interest at 0.9648 earlier today, justifying out view that top has been formed at 0.9705 yesterday and our short position entered at 0.9680 just met our downside target at 0.9580 (with 100 points profit) in NY morning, this anticipated decline signals the rise from 0.9421 low has ended at 0.9705 yesterday and mild downside bias remains for weakness to 0.9560-63 (50% Fibonacci retracement of 0.9421-0.9705) but reckon 0.9525-30 (61.8% Fibonacci retracement) would hold.

As we have taken profit on our short position entered at 0.9680, would not chase this fall here and would be prudent to stand aside in the meantime. Above the Kijun-Sen (now at 0.9621) would bring another bounce to 0.9648 but break there is needed to signal an intra-day low is formed, bring test of 0.9670-75 later.

Gold Unable to Make Headway on Weak Retail Sales

Gold has lost ground in the Friday session. In North American trade, the spot price for an ounce of gold is $1324.61, down 0.37%. On the release front, US retail sales reports were dismal. Core Retail Sales slowed to 0.2%, missing the forecast of 0.5%. Retail Sales was even worse, posting a decline of 0.2%, compared to the estimate of +0.1%. On the manufacturing front, the Empire State Manufacturing Index dipped to 24.4, but this easily beat the forecast of 18.2 points. Later in the day, the US releases UoM Consumer Sentiment.

North Korea was back in the headlines on Friday, as the country fired a missile over Japan, which landed in the Pacific Ocean. A similar launch several weeks ago ratcheted tensions in the region and sent investors flocking to safe-haven gold. However, investors have not panicked just yet, as the stock markets and gold remain steady despite the North Korean provocation. If the US decides to respond forcefully to the North Korean move, however, nervous investors could return to gold and send the metal to higher levels.

Earlier in 2017, the Federal Reserve was full of optimism that a strong US economy would warrant three rate hikes during in 2017. Fast forward to September – the economy has generally performed well, but the US continues to grapple with weak inflation levels. A strong labor market has not helped push inflation higher, as wage growth remains soft. Fed policymakers have retreated from their earlier optimistic forecasts, and have been counseling caution and patience regarding rate increases. A December hike remains iffy, but the odds of a rate increase have slowly been moving higher, and are currently at 50%. CPI, the primary gauge of consumer inflation, improved in August. Could this be a sign that at long last, inflation is moving in the right direction? If the markets feel this is the case, the odds of a December hike should continue to increase.

Strategy: A Tale of Three Central-Bank Camps

Today's key points

- Central bankers look increasingly divided into those in the 'exit' camp (Fed, BoE, ECB), those in the 'no exit camp' (BoJ, SNB), and those in between (Riksbank, Norges Bank)

- While the Fed looks determined to hike in December, it is unlikely to drive a major sell-off in EUR/USD

In a week which saw risk sentiment improving again following set-backs ahead of hurricane Irma and the imposition of harsher sanctions against North Korea, we also saw the Bank of England (BoE) signal a hiking cycle to begin sooner than we and the market were looking for, and the Swiss National Bank (SNB) emphasising its commitment to accommodative policy. In our view, this served to confirm that central bankers are now divided into largely three camps.

In the 'exit' camp we have the central banks looking to 'normalise' policy after years of using unconventional measures. A prominent member of this camp is the Fed, which has in fact been in tightening mode since the tapering discussion began back in 2013. But, this week's BoE meeting also clearly cemented that the BoE is keen to start a hiking cycle, see Bank of England review: November hike is now a close call. And then importantly, in our view, there is the ECB, which has somewhat started talking about 'reflationary' (rather than deflationary) risks – a wording once again used by ECB chief economist Praet in a speech reiterating the hawkish tone from last week's meeting.

In the 'no exit' camp, we have the central banks keen to avoid joining the 'normalisation' discussions taking place elsewhere, not least as they worry this could bring about unwanted currency strength. The Bank of Japan (BoJ) has clearly placed itself in this camp following the introduction of yield curve control and will likely stay in easing mode for an extended period as price pressure remains weak, see Research Japan: Running on all engines. This week's SNB meeting also confirmed that the Swiss are 'in it' (negative rates and a bloated balance sheet) for the long run as sustained price pressure is lacking still.

And then there is the group of those in-between, reluctant to side with either camp: arguably these would under 'normal' circumstances be looking to make policy less accommodative but are reluctant to do so as they are uncertain whether underlying inflationary pressure is strong enough to withstand currency strength along the way. This group in our view includes notably the Riksbank and Norges Bank, with the latter struggling with recent low inflation prints and the former insisting the latest inflation uptick is temporary; also both are wary of potentially wobbly housing markets.

Next up for revealing its preferences regarding policy is the Fed with the FOMC meeting next week, see FOMC preview, 15 September 2017. We expect the Fed to stay on hold but announce it will begin shrinking its balance sheet in October. The latter is widely expected and should not have a major impact on neither Treasury yields nor USD. But we also expect the median FOMC 'dots' to still signal one more hike this year and three hikes next year, which remain far from market expectations. This week saw a decent inflation print out of the US which, alongside slightly improved prospects of a corporate tax reform in the US, should keep the Fed on track for a December hike, in our view, even if it is an increasingly close call.

With central banks divided as indicated above, it is tempting to conclude that US yields should move higher and that USD strength could materialise near term. But not so fast: the short end of the US yield curve has struggled to move higher this year, which may be ascribed partly to fading Trump optimism, but which may more broadly be seen in the context of the sustained downward pressure on the natural rate of interest across a range of countries. The latter hints that the longer-term potential for yields to move higher may be limited, which in turn suggests that the potential for the Fed to hike and reduce its balance sheet simultaneously could be rather limited. This week we have seen a decent rebound in US and European bond yields, but we do not see this as the start of a continued sell-off in the bond market.

In the FX sphere, while USD/JPY remains in the hands of US Treasury yields which could be in for a muted rise in 2018, relative interest rates have largely failed to track movements in notably the sustained uptick in EUR/USD in the year so far. That said, a range of factors should cap EUR/USD upside near term on top of the possible, if limited, downside from a possible December Fed hike. Speculative positioning is closing in on stretched territory, suggesting risks are tilted to the downside for the cross. Unhedged equity flows seems to be fading and should thus provide less EUR support going forward. Also, our quantitative business-cycle models suggest the US economy is re-gaining momentum while the eurozone is now losing steam a bit.

But, as we highlighted in FX Edge: Power of flows - EUR/USD eyeing 1.30 longer term, the potential for a 'normalisation' in eurozone debt flows as the next leg of ECB exit pricing gains traction is a key source of upside risk for the single currency longer term. Crucially, the ECB seems increasingly willing to accept EUR appreciation these days as long as it happens gradually and is supported by a strong domestic economy. We look for EUR/USD to trade in a range around the 1.20 mark near term and reiterate our call that any dips in the cross will be shallow and short-lived. While we still look for a move towards the mid-1.20s further out we emphasise that the speed with which EUR/USD is set to move higher will be reduced going forward. Next to join the 'exit' camp could be the Riksbank, which we think will end its QE scheme this December. Relatively high inflation prints for the remainder of this year should serve as a cap on EUR/SEK, but significant SEK appreciation from here still requires a marked shift in policy stance from the Riksbank. We look for continued range-trading in EUR/SEK around 9.50 in the next few months.

Bank of Japan Preview: On Hold as Political Uncertainty Increases

- We expect the Bank of Japan (BoJ) to maintain its 'QQE with yield curve control' policy unchanged at its monetary policy meeting ending on 21 September.

- Political uncertainty is likely to increase in Japan where the focus will in particular centre on whether PM Abe calls for an early general election, and not least whether BoJ governor Koruda will be re-appointed to lead the BoJ for another five years when his current term ends in April 2018.

- In our main scenario, we expect the BoJ to keep its policy unchanged throughout our 12M forecast horizon, assuming that BoJ governor Koruda is re-appointed.

- We look for USD/JPY to remain range bound in the near term as political uncertainty (both in relation to North Korea and domestically in Japan) is likely to counter most of the JPY depreciation potential. Longer term, we expect USD/JPY to increase, targeting 114 in 3M and 116 in 6-12M.

- Tactically, we prefer to stay sidelined USD/JPY as highly unpredictable political risks leave a less attractive risk/reward. EUR- and DKK-based corporates should hedge JPY income with FX forwards.

We expect the Bank of Japan (BoJ) to maintain its 'QQE with yield curve control' policy unchanged at its monetary policy meeting ending on 21 September. It is widely expected that the BoJ will keep its monetary policy unchanged and that the announcement should not have any significant impact on price actions.

The Japanese economy is currently running on all engines, and GDP growth picked up speed in Q2 with at annualised growth of 2.5%. CPI inflation has also been increasing through 2017, but it has mainly been due to rising energy prices. Hence, the underlying price pressure in Japan remains very low, despite solid growth and a closed output gap, and the BoJ's 2% inflation target is currently nowhere within reach. See Research Japan: Running on all engines (12 September) for more details.

New board members less likely to oppose Kuroda's policy

The 20-21 September meeting will be the first meeting for the two new board members, Hitoshi Suzuki and Goshi Kataoka, who have been appointed by Japan's parliament to replace the two frequent dissenters on the board, Takahide Kiuchi and Takehiro Sato, as their five-year terms ended in July. Kataoka has an economic background and is viewed as a reflationist who is likely to support the BoJ's large-scale monetary easing, while Suzuki comes from a position in Tokyo-Mitsubishi UFJ's financial market operations, and both new members are less likely to oppose Koruda's policy. Hence, with the arrival of Kataoka and Suzuki the BoJ board will move in a more dovish direction and the nominations underscore that the Abe administration wants the BoJ to continue its current expansionary stimulus programme.

In terms of the BoJ, the focus will gradually turn to the question of who will be the next BoJ governor as Koruda's term as BoJ governor expires in April 2018. The decision about the next BoJ governor is expected by end-2017 and we still think it is most likely that Koruda will be reappointed. But uncertainty could create some volatility and induce JPY appreciation pressure, as the nomination of another candidate could be viewed as a signal that the government is expecting the BoJ to exit its current monetary policy

Rising political uncertainty the main risk to the BoJ's policy

The government's approval rating has recovered somewhat following a turbulent summer when a series of scandals involving PM Abe and his close political allies led to a plunge in the government's approval rating. The cabinet reshuffle in August has probably helped to improve his image, but political uncertainty is likely to remain high as the political calendar in Japan is packed with important events in the coming years.

During the autumn, the focus will be on the FY 2018 budget negotiations and not least the nomination of the next BoJ governor. Moreover, there has been some speculation whether PM Abe will dissolve the Lower House and call for an early general election in an attempt to strengthen his powerbase ahead of the LDP presidential election in September 2018 and the Upper House election in July 2019. As markets will probably link the fate of the Abe administration to the current accommodative policy regime (Abenomics), a potential change in leadership is likely to affect the expected outlook for fiscal and monetary policy.

FX outlook: higher USD/JPY and EUR/JPY in 6-12 months

While the combination of strong global PMIs and postponement of US debt limit risk is good for risk appetite and has improved the prospect of a higher USD/JPY in the near term, geopolitical uncertainty related to North Korea still represents a substantial downside risk and will continue to weigh on the cross. According to the latest IMM data, non-commercial JPY positioning is now back in stretched short territory, suggesting risks are tilted to the downside for USD/JPY from a positioning point of view. We still expect USD/JPY to trade within the 108-111 range near term targeting 111 in 1M and 114 in 3M. Fundamentally, we still see a case for a higher USD/JPY over the medium term horizon, driven by Fed-BoJ divergence, higher global yields (eventually) supported by global growth recovery and portfolio outflow out of Japan. We target USD/JPY at 116 in 6-12M.

EUR/JPY has proved to be less sensitive to negative risk sentiment driven by North Korean woes (declines in USD/JPY have been echoed by drops in EUR/USD). However, if the crisis escalates significantly, EUR/JPY would also take a plunge in our view. We look for EUR/JPY to trade in the range of 128-135 in the near term, targeting 135 in 3M. Longer term, we expect EUR/JPY to continue higher driven by real interest rates and portfolio outflows out of Japan as we expect the ECB to move towards monetary policy 'normalisation' before the BoJ. We target EUR/JPY at 141.50 in 6M and 145 in 12M.

FX strategy

Leveraged funds

While the underlying fundamentals combined with the postponement of the US debt limit risk support the case for a higher USD/JPY in the coming months, we prefer to stay sidelined USD/JPY for now. In our view, the combination of highly unpredictable political risks related to North Korea, and the risk of rising volatility and JPY appreciation pressure driven by domestic political uncertainty in Japan, leaves a less attractive risk/reward.

Corporates

We recommend EUR- and DKK-based corporates to hedge JPY income with FX forwards, while JPY expenses should be hedged via knock-in forwards.

US: Retail Sales Decline in August as Harvey Makes Landfall in Texas

Retail sales decreased 0.2% in August according to the advance Census Bureau report. This was well below expectations, which called for a rise of the same magnitude. Moreover, the previous month's surge in retail sales was cut in half, with the July gain now only reported as 0.3% m/m.

Sales at motor vehicle & parts dealers (-1.6%) subtracted from the headline - not surprising given the pullback in August auto sales to 16 million annualized. This decline was more than offset by the surge in gasoline stations spending , which rose by 2.5% on the month with the ex. autos and gas measure down 0.1% on the month.

Excluding gas, autos, building materials (-0.5%), and food services (+0.3%), the so-called 'control group' used in calculating GDP was down 0.2% on the month - below the 0.2% gain expected by economists. Gains in the control group were relatively broad, with miscellaneous (+1.4%), furniture (+0.4%), food & beverage (+0.3%) and general merchandise (+0.2%) seeing gains. Unusually, e-commerce sales were down 1.1%, alongside declines in clothing (-1.0%), electronics (-0.7%), and building materials (-0.5%).

Key Implications

Last month's advance report made us giddy with excitement at the prospect that American consumers were back in full force. And then came this morning's report, which effectively erased much of the outsized gains we believed occurred last month. Worse still, this morning's report also indicated that consumers were reluctant to spend in the month of August, despite the strong job and income figures as of late. Overall, the new information suggests that consumption in the third quarter was not as strong as otherwise thought, with real PCE growth likely to be near the 2.5% mark - down from the 3.2% during the second quarter.

Still, as far as the decline in retail sales during August, we believe that most is likely related to the disruption in economic activity in southeast Texas. While some retailers likely experienced pre-emptive buying ahead of landfall, others likely faced prolonged closures due to weather conditions and lack of inventory. The Census Bureau indicated that reports suggested that the "hurricane had both positive and negative effects" on sales while others indicated no impact at all. Moreover, some firms reported due to "permanent or temporary store closures and stores having reduced business due to damage, shipment delays, etc."

Ultimately, the decline in July makes sense given the disruption in economic activity related to the storm. We expect that both Harvey and Irma are likely to drag down GDP growth in the third quarter by about half a point (in annualized terms) with a boost of a similar magnitude during the fourth quarter. As such, expect further volatility in the data going forward. Having said that, we expect the Fed to largely see through the volatility given its transitory nature.

Elliott Wave Analysis: NZDUSD and GBPUSD

Good day traders! Let's start the US session with NZDUSD and GBPUSD.

NZDUSD is now finally turning up for wave c as part of double zig-zag correction. We see some sharp leg up now to the upper trendline which looks like a wave c that may stop at 0.7350 area next week and make a new turn lower.

NZDUSD, 1H

Pound is one of the strongest this week, now again at new highs, currently near 1.3600 which can be wave three so be aware of more upside after any intraday set-back. Trend is now up as long as market is above 1.3400.

GBPUSD, 1H