Sample Category Title

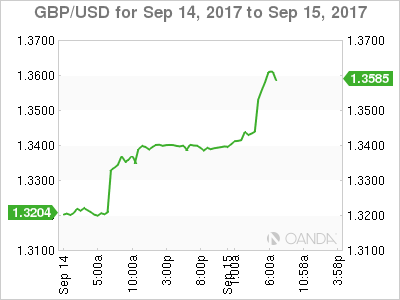

GBPUSD Moves Towards 1.3600

The British pound has moved to a new 2017 trading high against the U.S dollar for the fourth consecutive day, hitting 1.3600, following comments from BOE member Gertjan Vlieghe.

Active MPC voting member Vlieghe spoke of the need for the BOE to raise interest rates in the coming months, causing the GBPUSD pair to move to its highest trading level, since June 2016.

Going forward, the GBPUSD pair remains strongly bullish in the medium-term after a key technical break through above the pairs 100-week moving average, found at the 1.3401 level.

Key technical resistance above the 1.3600 level is located at 1.3620, 1.3652 and 1.3680.

Key GBPUSD technical support is found at the recent swing price lows, located at 1.3567 and 1.3536.

The January 2009 price low, offers further historical support, at 1.3503, as does the pairs 100-week moving average, at 1.3401.

EURUSD – Backs Off Lower Prices, Eyes Further Upside Pressure

EURUSD - With the pair halting its weakness to close higher on Thursday, a move further higher is envisaged. Resistance comes in at 1.2000 level with a cut through here opening the door for more upside towards the 1.2050 level. Further up, resistance lies at the 1.2100 level where a break will expose the 1.2150 level. Conversely, support lies at the 1.1900 level where a violation will aim at the 1.1850 level. A break of here will aim at the 1.1800 level. Below here will open the door for more weakness towards the 1.1750. All in all, EURUSD faces further upside on corrective recovery.

Technical Outlook: GBPJPY Surged Above 151.00 And Hit The Highest Since June 2016

The pair blasted through psychological 150 barrier on Thursday and broke above strong barrier at 151.11 (Fibo 38.2% of larger 195.24/123.83 (Aug 2015 / Sep 2016 descend), boosted by fresh hawkish comments from BoE MPC member about interest rate hike in coming months.

Weekly close above this pivotal point would generate another strong bullish signal for further advance.

The pair is currently riding on the third wave of five-wave cycle from 139.30 and eyes its FE 300% at 152.08.

There are no firmer signals of fatigue so far, as the pair gained over 3.5% in less than two days and strongly overbought daily studies, however, corrective action could be anticipated in coming sessions.

Former tops at 148.45, 148.10 and 147.77 (posted on 11 Dec 2016, 07 May and 09 July 2017 respectively) now act as solid supports.

Res: 151.54, 152.08, 153.01, 154.24

Sup: 151.00, 150.00, 149.31, 148.45

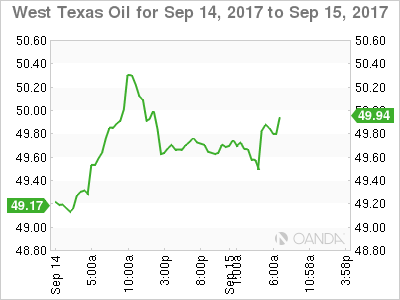

CRUDE OIL Surging Again

Crude oil has strongly declined after the commodity monitored the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance can be found at 50.43 (31/07/2017). Expected to show further monitoring of the 50- level short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Continued Bearish Consolidation

Silver has failed to reach strong resistance at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in an uptrend channel. Expected to show further consolidation.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

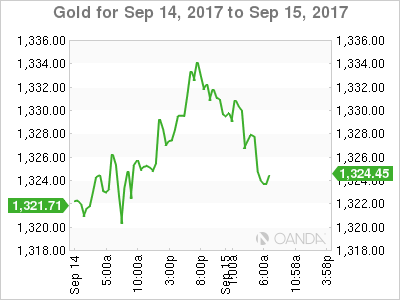

GOLD Timid Rebound

Gold is trading mixed within uptrend channel. Hourly support is given at a distance 1319 (intradayy low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued increase within uptrend channel.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

BITCOIN Crashing

Bitcoin is taking a dive after strong interest over the summer. Support lies at 3599 (22/08/2017 low) has been broken. Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further decline below $3000.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Buying Demand

EUR/CHF's buying pressures are going up and the pair has broken resistance area between 1.1356 and 1.1472. Further medium-term sideways moves are favoured.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low)

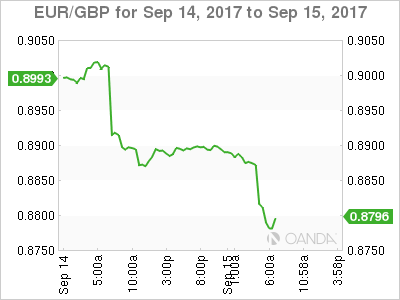

EUR/GBP Strong Decline

EUR/GBP is trading lower. However, as long as prices remain below the resistance at 0.9176 (declining trendline), the short-term technical structure is biased to the downside. Hourly support is given at 0.8982 (12/09/2017). Resistance lies at 0.9306 (29/07/2017 high).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

Safe Havens Fall Amid Missile Fatigue

Friday September 15: Five things the markets are talking about

North Korea's latest missile test overnight has not managed to generate a lasting market reaction. The launch is the second to fly over Japan in less than a month and the first since the U.N adopted fresh sanctions earlier this week.

Note: Japan's Defense Minister indicated that the missile launched could be an intermediate range ballistic missile (IRBM). The UN Security Council is expected to meet later this afternoon (3 pm EDT).

Global equities have traded mixed as Pyongyang latest missile launch raised geopolitical tensions, though declines in traditional risk assets – gold, yen and CHF – indicate that many investors are becoming somewhat accustomed to the sequence of baiting and diplomatic reaction.

Yesterday's stronger than expected U.S consumer inflation data is lending pockets of support for the 'mighty' dollar and U.S bond yields as fixed income dealers increase their bets for the potential of another Fed rate hike in 2017.

Markets focus now shifts to this morning's volatile U.S retail sales (08:30 am EDT), industrial production (09:15 am EDT) and consumer sentiment print (10 am EDT).

1. Global stocks mixed reaction

In Japan, the Nikkei share average ended higher overnight (+0.5%), and posted its biggest weekly gain in ten-months (+3.3%) as a stronger dollar supported exporters. Investors basically shrugged off N. Korea's missile launch that happened to knock risk appetite in wider Asia. The broader Topix advanced +0.4%.

In South Korea, the Kospi index ended +0.4% higher after dropping as much as -0.5% intraday, while down-under, Australia's S&P/ASX 200 Index fell -0.8%.

In Hong Kong, the Hang Seng Index swung between gains and losses (+0.1%), while the China Enterprises Index lost -0.3%.

In China, equities end the week lower on signs that Chinas economy may be losing steam. The blue-chip CSI300 index ended little changed, while the Shanghai Composite Index fell -0.5%. For the week, the CSI300 rose +0.1%, while SSEC slid -0.3%.

In Europe, regional indices trade mostly lower, led again by the FTSE 100 which has continued yesterday's steep drop after 'hawkish' commentary this morning from the BoE's strongest 'dove' has pushed GBP +1.2% higher outright (see below).

Indices: Stoxx600 -0.1% at 381.6, FTSE -0.7% at 7247, DAX flat at 12536, CAC-40 flat at 5225, IBEX-35 -0.2% at 10341, FTSE MIB flat at 22274, SMI -0.4% at 9040, S&P 500 Futures -0.1%

2. Oil falls as markets dip on N. Korea tensions, gold lower

Ahead of the U.S open, oil prices are a tad softer as global markets weaken following N. Korea's latest missile launch.

Nevertheless, crude prices remain atop of their five-month highs reached this week on bullish demand forecasts and U.S refineries restarting.

Brent crude futures are down -18c at +$55.29 a barrel, however the benchmark remains on track for its third consecutive weekly gain and the highest weekly rise since the end of July.

U.S West Texas Intermediate crude (WTI) is down -16c at +$49.73 a barrel. The contract is set for a +5% weekly gain, also its strongest in nearly two-months.

Note: OPEC this week forecasted higher demand for its oil in 2018 and pointed to signs of a tighter global market, while the IEA said the global oil glut was shrinking due to strong European and U.S demand, as well as production declines in OPEC.

Spot gold has slipped overnight (down -0.2% at +$1,326.70 an ounce), shrugging off N. Korea's latest missile launch. Strong U.S inflation data yesterday is raising the spectre of another Fed hike by year-end interest, which is supporting the U.S dollar. The 'yellow' metal is down over -1% for the week, on track for its first weekly decline in a month.

3. BoE's most 'dovish' member now sees need for rate hike

The BoE's most 'dovish' member has changed his view and now thinks a hike may be needed soon.

In a speech this morning, Gertjan Vlieghe said the U.K economy was “running through its spare capacity quicker than he had expected, while household spending was stronger.'

Fixed income dealers now peg a 50-50 chance that the BoE will raise its policy rate in November after his comments, which have boosted Sterling Overnight Index Swap Average (OIS) this morning. The probability of a +25 bps rate rise has jumped from +0.25% to +49.92% – it stood at +33.32% after yesterday's BoE decision and minutes. Ten-year gilt yields have backed up to +1.282% from +1.244%.

Elsewhere, the yield on U.S 10-year Treasuries advanced +1 bps to +2.19%, while Germany's 10-year Bund yield dipped -1 bps to +0.41%, the first retreat in more than a week.

4. GBP hits 15-month highs on a 'hawkish' dove

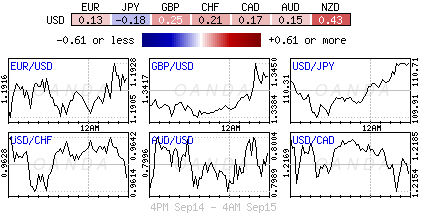

Sterling (£1.3569) continues its relentless rally in European trading, adding to yesterday's gains in the wake of the BoE sounding in favor of raising interest rates sooner than the market has expected. While voting 7-2 yesterday to hold steady, the post-meeting statement pointed to a November tightening amid central-bank forecasts of +3% inflation in October.

The EUR (€1.1949) remains better bid outright, helped as the dollar underperforms against a strengthening pound. It's also being supported by comments from ECB policymaker Sabine Lautenschlaeger who reiterated that “it is time to decide on scaling back bond purchases next year and that conditions are in place for inflation to reach a stable trend.'

The JPY (¥111.24) is well off its overnight highs despite another missile launch from N. Korea. Investors seem happy to speculate that the ongoing tension on the Korean Peninsula would not lead to any actual military action.

5. Eurozone wage growth hits two-year high

Data released this morning by the E.U statistics agency suggest that things are about to change on the inflation front for the ECB.

Eurozone wages rose at the fastest pace in more than two years during the three months to June, a sign inflation may be set to rise to the ECB's target.

Eurostat said wages were +2.0% higher in Q2 than a year earlier, the fastest rise since Q1 of 2015 and up from +1.3% in the previous three-month period.

Note: The missing element in the link between growth and inflation has been wages, which have grown more slowly than President Draghi and company had expected.