Sample Category Title

Elliott Wave View: ES_F E-Mini S&P500 Pullback Near

Short Term Elliott Wave view in ES_F E-Mini S&P500 suggests the rally to 2403.75 ended Minor wave A. Minor wave B unfolded as an Expanded Flat Elliott Wave structure where Minute wave ((a)) ended at 2379, Minute wave ((b)) ended at 2404.5, and Minute wave ((c)) of B ended at 2344.5. After ending the pullback, the Index started a new leg higher and the rally from 2344.5 low looks to be unfolding as a 5 waves Elliott Wave impulse structure where Minutte wave (i) ended at 2375, Minutte wave (ii) ended at 2361, and Minutte wave (iii) remains in progress and can reach 2423.13 or 161.8% fibonacci extension of Minutte wave (i). Expect Minutte wave (iv) pullback to start once Minutte wave (iii) is over before turning higher one more leg in Minutte wave (v). This last push higher will also complete larger degree Minute wave ((i)) and as impulse, it should be accompanied with momentum divergence.

Once Minute wave ((i)) is complete, the Index should pullback within Minute wave ((ii)) in 3, 7, or 11 swing to correct cycle from 5/18 low (2344.7) before the rally resumes again. As ES_F E-Mini S&P500 has broken above the previous peak at 2404.5, it gives more conviction that the Index has started the next leg higher and thus pullback can likely hold above 2344.7 for more upside. We don’t like selling the proposed pullback and expect buyers to appear again once Minute wave ((ii)) pullback is complete at later stage, provided that pivot at 2344.7 low remains intact.

Market Morning Briefing: Dollar Index (97.27) Held Previous Day’s Low

STOCKS

Dow (21082.95, +0.34%) has moved up exactly as expected. Now we need to see if it is able to break above 21200 or comes off sharply from there to re-test 21000 or lower in the near term. Note that 21200 is an important resistance to keep an eye on. A sustained break above 21200 could turn very bullish towards 21400-21600 in the long term.

Dax (12621.72, -0.17%) fell yesterday and is trading sideways within the 12700-12500 region for now. Trading exactly in the middle of the broader 12400-12900 region, there is equal chances of moving in either direction. We will have to wait and watch for some confirmation.

Shanghai (3109.25, +0.05%) has risen sharply breaking the immediate resistance on the daily charts, while the support on the 3-day charts has held well producing a bounce in the last few sessions as expected. There is enough room on the upside towards 3200 in the medium term.

Nikkei (19762.11, -0.26%) could possibly remain sideways within 20000-19600 region as mentioned earlier. Thereafter if resistance near 20000 holds, there could be a sharp fall towards 19200 or lower; else a sustained price confirmation above 20000 is needed to initiate further bullishness.

Nifty (9509.75, +1.59%) faced sharp bounce from levels just above our mentioned 9350 support. But also note that 9525 is an important immediate resistance and on a break above 9525-9530 only, we may become more bullish towards 9700-9800 on a longer term; else a fall back towards 9350-9300 is possible in the near term.

COMMODITIES

Muted price action has been seen in Gold (1256). If 1249 holds on a closing basis then sideways consolidation within 1249-1280 continues. Thus we need to keep a close watch on the price action in Dollar Index which could give some cue on further Gold direction. But we will remain bearish while it is trading below 1280 levels and a close below 1249 could open up 1230 levels as well.

Similar kind of trading pattern has been seen in silver (17.15) also. It is trading above 17 levels, thus a possibility of a sideways movement between 16.90-17.50 levels can't be ruled out.

Copper (2.58) is hovering around between 2.55-2.60 for last few days . Only above 2.62, higher resistances of 2.68-72 can come into consideration. In the medium term 2.55 are going to be a strong support now but a close below that could open up 2.44-35 levels as well.

We had clearly mentioned in our yesterday's morning briefing that “The only concern is the short term overbought condition though the downside possibly limited to 51.80 for Brent and 49.30 for WTI”. Yesterday Brent (51.50) fell $2.51, nearly 5% and WTI (48.88) was down by $2.45. Immediate trading range for Brent and WTI are 51.20-52.80 and 47.43-49.51 respectively.

FOREX

Dollar Index (97.27) held previous day's low to recover to a minor degree but the corrective bounce can reach 98.30 at best if it manages to break and sustain above the interim resistance of 97.45. Our downside target of 96.50-00 remains unchanged.

Euro (1.1196) is seeing a normal correction while the larger uptrend remains intact so far. This correction can take it to 1.1100-1.1075 where fresh buying can be expected again.

Dollar Yen (111.56) is almost stable and has not been able to break above 12 in the last 3-sessions. But while above important support at 110, there is scope for an upmove towards 114.0-114.5 in the medium term. We could possibly see a sideways consolidation for a few sessions before a sharp directional move is seen.

Pound (1.28890) is trading above support near 1.2865 and while that holds, a rise towards 1.32 cannot be ignored. Downside could be limited to 1.2750 in the next 2-3 sessions while an up move towards 1.3250 is still on the cards.

Aussie (0.7432) is trading lower and could possibly come off towards 0.74 or slightly lower in the near term.

Dollar Rupee (64.61) could remain stable within 64.90-64.50 today and while immediate resistance of 65.00-65.20 holds, the possibility of further Rupee weakness seems less.

INTEREST RATES

The US yields are almost stable but are trying to slowly inch up towards higher levels. There is some potential for an upmove in the near term.

The German-US 10YR (-1.88%) has come off from resistance at -1.83% and while that holds, the yield spread could come down in the near term.

The German yields by themselves are trying to move up slowly and looks bullish in the near term.

The UK yields are down and heading towards medium term support levels. A bounce thereafter could be possible by another 2-3sessions.

The Japanese yields on the other hand have fallen in the last 2-sessions and could test the earlier resistance turned support before again bouncing back in the longer run.

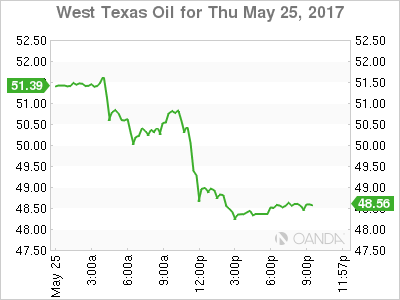

OPEC Supply Cut Extension Disappoints The Oil Market

- OPEC has decided to extend supply cuts until March 2018.

- That left the market disappointed, leading to the biggest daily plunge in oil prices since the start of 2016.

- We keep a short-term neutral stance on the oil price, while we remain mediumterm positive, maintaining our USD60/bl 2018 forecast for Brent crude.

Today, the Organisation of Petroleum Exporting Countries (OPEC) decided to extend the deal to cut oil production agreed on last November for another nine months with effect from 1 July. 11 non-OPEC countries including Russia are said to back the decision, which means that the group of 22 oil-producing countries will maintain 1.8m bpd of supply cuts until March 2018. The decision follows the recommendation from the Joint OPEC-Non- OPEC Ministerial Monitoring Committee (JMMC) from yesterday. The nine-month extension goes further than the original deal from last November, which included an option for extending supply cuts by six months.

JMMC further reported yesterday that compliance to the deal was 102% in April. Hence, OPEC and its allies outside the cartel have delivered on their part. However, it has only had little overall impact on the oil market. Firstly, the output cuts have been mitigated by expected production increases in the US (chart 2). Hence, overall production remains unscathed, but market shares have shifted from OPEC and Russia to the US. Secondly, oil stocks remains high. For example, US crude stocks remain around the levels from 2016 when taking into account seasonal fluctuations (chart 3). While they have fallen back in recent weeks, it most likely reflects an adjustment following the surprisingly strong build at the beginning of the year. Thirdly, the Brent crude spot price is around USD5/bl higher than before the supply cuts were announced last year. However, the price on longer-dated forward contracts is now lower. For example, the calendar 2019 average Brent swap is around USD52/bl, more than USD2/bl lower than last November. It suggests that the supply cuts should not lead to a tighter oil market over the longer run.

Following the announcement, the price on Brent crude has dropped more than 5% to close USD51/bl. It is the largest daily drop since the selloff at the beginning of 2016 (chart 1). Hence, the oil market is disappointed that OPEC did not deliver more today, either in terms of deeper production cuts or a longer extension. Speculative positioning before the meeting was net long (see IMM Positioning Update: GBP positioning at highest level since March 2016 ), which has likely exacerbated the market reaction. In our view, there is likely a degree of immediate overreaction in oil market and we could see prices recover slightly in the coming days. That said, we maintain a neutral stance on the oil price near term and highlight important downside risks from a potentially more hawkish Federal Reserve, which is set to meet in June. This could lead the USD higher (we forecast EUR/USD at 1.09 in 3M), a further deterioration of the recent financial stress in China and the global business cycle beginning to turn lower in the coming months. Medium term, we remain positive on the oil price and forecast the price on Brent crude to average USD60/bl in 2018 on the back of a lower USD and somewhat tighter oil market.

Slip Sliding Away: Oil

Slip Sliding Away: Oil

The highly anticipated OPEC meeting disappointed expectations as the cartel extended plans to limit production but did not announce deeper cuts. Oil prices were smoked in a classic case of buy the rumour sell the fact as markets prepositioning suggested some speculators were pinning hopes for a more bullish outcome. While a cruel move on WTI ensued, US equities shrugged off the oil spill propped by strong retailer earnings results.The uptick in earnings is turning more than a few heads this morning as investors efficaciousness of brick and mortar retailers to compete with online retailer was growing. The pleasant surprise saw the S&P close up .5 %

ON the US data front, dealers mostly ignored them, as the tier 2 releases were mixed with stronger initial claims results offset by downside disappointments in advance goods trade balance for April which showed a larger than expected deficit of -67.6bn and wholesale inventories were negative, declining -0.3% MoM vs. +0.2%. I suspect dealers will do little more than shrug off most data points leading up to next week’s granddaddy of them all, Non-Farm Payroll.

Dollar bulls took solace in FED member Brainard 'brighter' outlook comments. Although more fluff than candour, some are latching on to a shift in the ' Uber Dove Brainard' language as significant. Mind you US Treasuries sold off and provided a reprieve for the dollar.

The market is still having trouble making sense of the post-Fed minute’s price action.While the minutes did contain the usual level of verbal gymnastics, by all accounts it did provide confirmation that the FOMC is moving full speed ahead, so why isn’t USDJPY trading higher?

While the shifting focus to all things 'balance sheet' reads marginally hawkish, the markets acuteness to inflation and wages plays out dovish for the rest of the curve unless of course the data points otherwise. Hence the reason why next week’s NFP and in particular the wage growth component is a huge inflexion point.

Euro

EURUSD dips continue to be covered mind you at a much slower pace as we enter the weekend. The EURUSD into a wall of resistance at 1.1250 overnight from profit takers who were content to start the long weekend process of position unwind after a bountiful run on the Euro this week. .Look for further position squaring to dominate flow today; it could get choppy.

The song remains the same.With ECB in two weeks, we should expect a heightened level of market discourse between now and then as this policy battle unfolds.

Japanese Yen

Better risk appetite should eventually carry the day on this trade, and with dips remaining very shallow we could see some appeal for long USDJPY emerge next week, In the meantime, the market continues to rotate into EURJPY for now because of quicker price action, while maintaining a dip bias on the USDJPY.

Australian dollar

We don’t even need a crystal ball for this view as the market had all but convinced itself that selling above .7500 is the trade.

Action continues to pick up on the AUDNZD ( Dairy vs. Iron ore ) as we approach the critical 1.0600 level.Given the resilience in milk prices and the recent wobbles in iron ore, high NZD trade balance notwithstanding, a break of 1.06 should see significant buy-in which could pressure AUDUSD toward .7400 level.

Chinese Yuan

USDCNH is the hot topic and very well offered in the interbank after the CNY fix continues come out below model consensus. In defiance to the Moody’s downgrade, the state-owned banks are big sellers of the dollar as the Pboc want the currency strong and stable. While dealers were testing the waters buying dips early in the week post fixing, once again dancing with Tiger has again proven to be a dangerous pastime in the currency markets.

Malaysian Ringgit

The market continues digesting the oil spill.While the USDMYR has pulled back from overnight yet remains surprising constructive despite the massive drop in oil prices

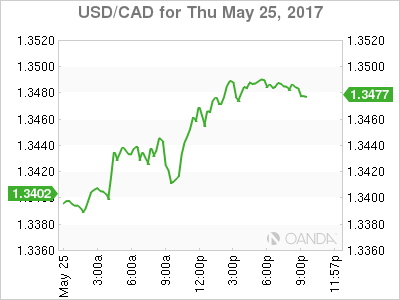

USD/CAD Canadian Dollar Lower After OPEC Extension Announcement Meets Expectations

The Canadian dollar depreciated on Thursday after the price of oil fell close to 5 percent after the announcement by the Organization of the Petroleum Exporting Countries (OPEC) and other major producers to extend the production cut deal by an additional 9 months. Rumours and statements ahead of at the meeting in Vienna had built up some anticipation about a longer time extension or deeper production cuts. The OPEC agreed to extend a daily 1.8 million cut to the end of the first quarter of 2018. The market had already priced in the expected extension and quickly sold crude when there was no surprise to the end of the meeting.

A Reuters poll released on Thursday showed that the Home Capital Group's problems are not likely to affect investor confidence in the Canadian market. Three of the six major banks agreed that the situation at Home Capital is one of liquidity, not a credit issue. The ratings agency Moody's has downgraded the banks citing a higher housing crisis exposure. Canadian banks reported earnings and boosted the TSX by easily beating estimates.

The loonie with high correlation to crude prices and a dependancy on exports to the US will be caught between the energy production fight between the US and OPEC. The renegotiation of the NAFTA is set for late August with an uncertain outcome as the US has stepped up the combative rhetoric.

The optimistic view of the Bank of Canada (BoC) towards the economy is not shared by the market as short positions on the CAD grew to a two decade high last week. Political risk in the US has not derailed its position on trade and could directly impact the Canadian economy as two thirds of exports are headed south of the border.

The USD/CAD gained 0.431 percent in the last 24 hours. The pair is trading at 1.3488 after the OPEC and other major producers announced the extension of the production cut deal for an additional 9 months. The high correlation between oil prices and the loonie dragged the currency further down as traders took profits from the crude move ahead of the OPEC meeting.

The USD came back against petrocurrencies as the price oil of fell off a cliff after the OPEC meeting. With little economic data to shore the CAD it fell ahead of the Group of seven meeting in Europe.

The USD has given back most of its post election gains. Political risk is becoming the most important driver of the currency. The turmoil surrounding the Russian links investigation is having a sizeable impact in US growth expectations as it directly impacts the timeline of the much-awaited pro-growth reforms on taxes and infrastructure spending.

The U.S. Federal Reserve is ready to hike rates in June and there is a big question mark if they will follow it with a December interest raise. Here again the central bank is awaiting for clarity in the government's efforts to boost the economy, if the chaos results in inaction the Fed will hold putting downward pressure on the greenback.

Oil prices will continue to be caught between US rising production and the efforts of the OPEC to reduce the glut. Demand for energy continues to stagnate which makes the showdown even more intense as the US exports have begun to move into markets usually dominated by OPEC members.

The price of oil fell 5.006 percent on Thursday. The West Texas Intermediate is trading at $48.41 after the extension announcement that will take the production deal between OPEC and 11 other major producers to March of 2018. The deal managed to stabilize the price of crude following the sudden drop in the past two years. The market share grab by Saudi Arabia backfired when oil prices spiralled down. The Organization of the Petroleum Exporting Countries (OPEC) then started approaching other major producers, Russia in particular about a production freeze that evolved into the current production deal.

The newly agreed extension will keep production subdued into 2018 is an effort to keep prices stable and reduce the oil glut that currently persists in the market. On the other side of the production equation are producers that did not sign into the agreement like Brazil, Canada and the United States.

The announcement today by the Organization of the Petroleum Exporting Countries (OPEC) and other major producers will go a long way in continuing what they started this year. Their goal to stabilize crude prices has been met, but ramping production from countries not part of the agreement (Brazil, Canada and the United States) is keeping the price of oil within a certain range.

Petrocurrencies will benefit from the decision as prices will keep near current levels despite higher shale production. The Canadian dollar, Australian dollar and the Norwegian krone will appreciate as long as crude prices are stable.

The United States has gone from a net importer of crude to an exporter which could benefit the USD by boosting economic growth as the American industry appears to have withstood the headwinds from falling prices from two years ago. The Trump administration even suggested selling part of its strategic reserves which could put further pressure on oil prices and the efforts of the OPEC and other producers who have signed the extension.

Market events to watch this week:

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

Gold Unchanged After Cautious Fed Minutes, Revised GDP Next

Gold is almost unchanged in the Thursday session. In North American trade, spot gold is trading at $1256.43 an ounce. On the release front, today's highlight was unemployment claims, which edged up to 234 thousand, lower than the estimate of 238 thousand. On Friday, the US releases Preliminary GDP for the first quarter, which is expected at 0.9%. The initial GDP release in April posted a gain of 0.7%. As well, the US releases Core Durable Goods Orders and UoM Consumer Sentiment. Leaders of the G-7 countries will hold a summit in Sicily, with the backdrop of the Manchester terror attack just a few days ago.

The Federal Reserve's minutes from the May policy meeting were closely watched by the markets, but gold has showed little reaction to the release. Traders hoping for confirmation of a June rate hike came away disappointed, as the minutes conveyed a less hawkish tone than the markets had expected. Policymakers were careful in their message, saying that a rate hike was coming “soon”. Does that mean a move at the June policy meeting? The markets clearly expect a rate hike, as Fed funds futures for a June increase remained at 78% after the minutes were released. At the same time, the Fed has given itself some wiggle room, and could opt to delay a hike until the second quarter if inflation or consumer indicators take an unexpected nosedive. The minutes stated that policymakers wanted to see additional evidence that the recent slowdown in the economy was temporary before raising rates. As for additional hikes in 2017, the markets remain skeptical. The odds for a September rate stand at just 37%. This pessimism is a result of a weak performance from the US economy in Q1, as well as doubts that President Trump, who is facing congressional investigations over his connections with the Russian government, will be able to pass his agenda of cutting taxes and government spending. Gone are the heady days at the end of 2016, when a red-hot US economy had analysts predicting four rate hikes in 2017. At the same time, a strong improvement in economic data could quickly change the cautious tone of the Fed and revive discussion of four rate hikes this year.

The White House sent President Trump's 2018 budget proposal to lawmakers in Congress this week, where it is sure to get a chilly reception. Trump has promised to slash government spending, and much of the funds for the budget would come from huge cuts to the Medicaid health program and food stamps. The budget proposes slashing more than $600 billion from Medicaid and over $192 billion from food stamps over a decade. Trump has promised to balance the budget within 10 years, claiming this can be achieved through tax cuts and annual growth of 3 percent. However, experts are at odds as to whether the economy can reach and maintain such levels of growth, which is much higher than current economic expansion. The budget proposal is unlikely to remain in its present form for very long on Capitol Hill. Democrats will want nothing to do with it, and Republicans will not want to make drastic cuts to federal programs that will incur the wrath of voters. Still, the Trump administration, which has been in damage-control mode for weeks over the firing of FBI director James Comey, can point to the budget as a step forward in trying to implement Trump's pro-business agenda.

OPEC Extends, Oil Crumbles

Crude prices fell 5% as traders sold-the-fact on a 9-month supply cut extension. The US dollar was the top performer while the Australian dollar lagged. Japanese CPI is due up next.

Management is the art of communication and that extends to market management as well. A month ago, a nine-month extension of OPEC/non-OPEC supply cuts would have been a welcome surprise in the energy market.

Instead, stories began to circulate about a six-month extension. That was followed by talk of a nine-month extension and it was eventually capped off by speculation about a 12-month extension or deeper cuts. By the time today's nine-month extension was announced it underwhelmed and WTI crude fell to $48.80 from $52.00. Brent had a similar 5% fall.

The challenge now is to separate the disappointment trade from the fundamentals. At current levels, oil is well below the Dec-Feb range and is nearing the March bottom at $47-48. It's still far above May's $44.00 low.

An offshoot of the oil trade is USD/CAD. That pair rose 65 pips on Thursday but that's less than the bulls would have hoped given the 100 pip drop the day before. You have to wonder if CAD has been hit by so much bad news – and with such a massive net short – that there is no fuel left for the bears.

Switching gears, the week winds down for Asia-Pacific traders with a Japanese CPI as the main highlight. The April numbers are due at 2330 GMT and expected to be up 0.4% year-over-year but flat excluding fresh food and energy.

Another event to watch is a speech from the Fed's Bullard at 0200 GMT. He's said previously that he doesn't think another hike is necessary but wouldn't be opposed to one more.

Finally, the RBA's Richards is in a panel presentation at 0430 GMT.

Yen Edges Lower as US Jobless Claims Beat Expectations, Japanese Inflation Next

USD/JPY has posted slight gains in the Thursday session. In North American trade, the pair is trading just below the 112 level. On the release front, US unemployment claims edged up to 234 thousand, lower than the forecast of 238 thousand. Japan will release a host of inflation indicators, led by Tokyo Core CPI, which an estimate of 0.0%. On Friday, leaders of the G-7 nations meet in Sicily. The US will release revised GDP for the first quarter, which is expected at 0.9%, compared to the initial GDP release, which came in at 0.7%. Other key US indicators include Core Durable Goods Orders and UoM Consumer Sentiment.

The currency markets have shown little response to the Federal Reserve's minutes from the May policy meeting. Traders hoping for confirmation of a June rate hike came away disappointed, as the minutes conveyed a less hawkish tone than the markets had expected. Policymakers were careful in their message, saying that a rate hike was coming "soon". Does that mean a move at the June policy meeting? The markets clearly expect a rate hike, as Fed funds futures for a June increase remained at 78% after the minutes were released. At the same time, the Fed has given itself some wiggle room, and could opt to delay a hike until the second quarter if inflation or consumer indicators take an unexpected nosedive. The minutes stated that policymakers wanted to see additional evidence that the recent slowdown in the economy was temporary before raising rates. As for additional hikes in 2017, the markets remain skeptical. The odds for a September rate stand at just 37%. This pessimism is a result of a weak performance from the US economy in Q1, as well as doubts that President Trump, who is facing congressional investigations over his connections with the Russian government, will be able to pass his agenda of cutting taxes and government spending. Gone are the heady days at the end of 2016, when a red-hot US economy had analysts predicting four rate hikes in 2017. At the same time, a strong improvement in economic data could quickly change the cautious tone of the Fed and revive discussion of four rate hikes this year.

The White House presented President Trump's 2018 budget proposal to lawmakers in Congress this week, but will it be dead-on-arrival? Trump has promised to slash government spending, and much of the funds for the budget would come from huge cuts to the Medicaid health program and food stamps. The budget proposes slashing more than $600 billion from Medicaid and over $192 billion from food stamps over a decade. Trump has promised to balance the budget within 10 years, claiming this can be achieved through tax cuts and annual growth of 3 percent. However, experts are at odds as to whether the economy can reach and maintain such levels of growth, which is much higher than current economic expansion. The budget proposal is unlikely to remain in its present form for very long on Capitol Hill. Democrats will want nothing to do with it, and Republicans will not want to make drastic cuts to federal programs that will incur the wrath of voters. Still, the Trump administration, which has been in damage-control mode for weeks over the firing of FBI director James Comey, can point to the budget as a step forward in trying to implement Trump's pro-business agenda.

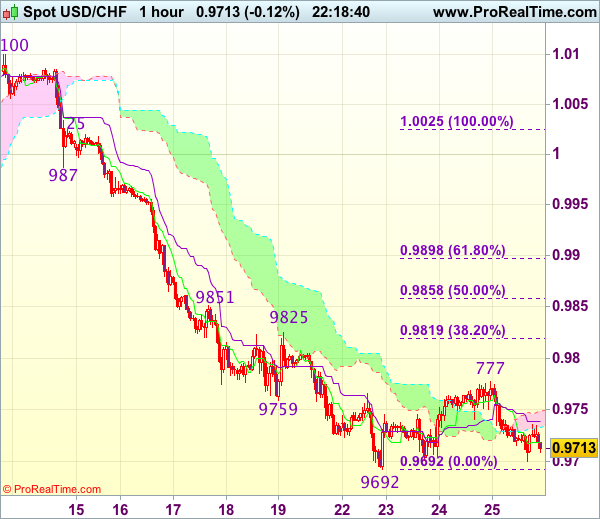

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9700

USD/CHF - 0.9718

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9718

Kijun-Sen level : 0.9739

Ichimoku cloud top : 0.9749

Ichimoku cloud bottom : 0.9733

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

As the greenback has retreated after meeting resistance at 0.9777 yesterday, as long as support at 0.9692 holds, further consolidation would take place and prospect of another rebound remains, above said resistance at 0.9777 would add credence to our view that temporary low is formed, bring retracement of recent decline to 0.9800, then 0.9819-25 (38.2% Fibonacci retracement of 1.0025-0.9692 and previous resistance) but price should falter below resistance at 0.9851 (also just below 50% Fibonacci retracement at 0.9858), bring another decline later.

In view of this, we are holding on to our long position entered at 0.9700. Below said support at 0.9692 would signal recent decline has resumed and extend weakness to 0.9670-75 but reckon downside would be limited to 0.9650 and 0.9620-25 should hold, bring another rebound later.

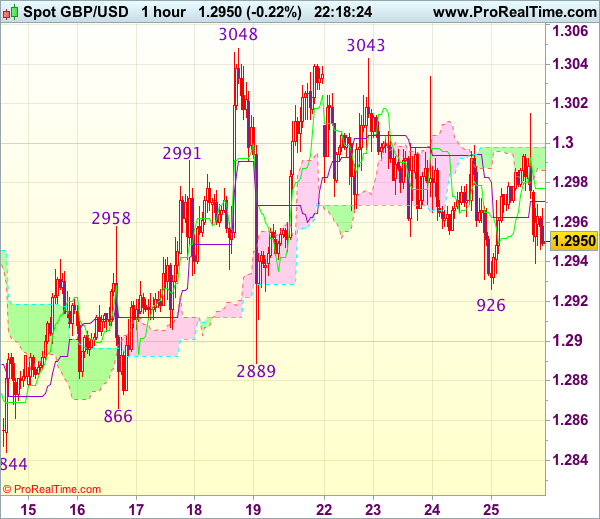

Trade Idea Wrap-up: GBP/USD – Hold long entered at 1.2960

GBP/USD - 1.2950

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2977

Kijun-Sen level : 1.2971

Ichimoku cloud top : 1.2998

Ichimoku cloud bottom : 1.2986

Original strategy :

Bought at 1.2960, Target: 1.3060, Stop: 1.2925

Position : - Long at 1.2960

Target : - 1.3060

Stop : - 1.2925

New strategy :

Hold long entered at 1.2960, Target: 1.3060, Stop: 1.2925

Position : - Long at 1.2960

Target : - 1.3060

Stop : - 1.2925

Failure to extend intra-day rebound and current retreat from 1.3015 suggest caution on our long position entered at 1.2960 but as long as yesterday’s low at 1.2926 holds, prospect of another rebound remains, above said intra-day high would bring test of strong resistance at 1.3043-48, however, break there is needed to confirm early upmove has resumed and extend headway to 1.3075-80 and possibly towards 1.3100-10 later.

In view of this, we are holding on to our long position entered at 1.2960. Below said support at 1.2926 would abort and risk weakness to 1.2900 but break of indicated support at 1.2889 is needed to signal top has been formed at 1.3048 earlier, bring retracement of recent upmove to 1.2850-55 first.