Sample Category Title

Trade Idea: AUD/USD – Buy at 0.7405

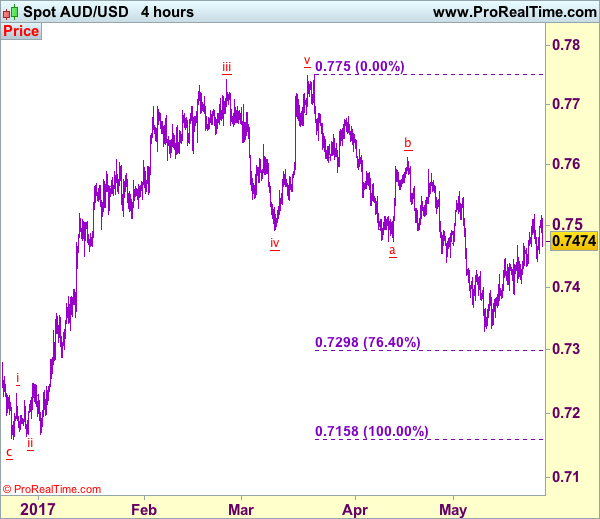

AUD/USD – 0.7467

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Buy at 0.7405, Target: 0.7570, Stop: 0.7345

Position: -

Target: -

Stop: -

New strategy :

Buy at 0.7405, Target: 0.7570, Stop: 0.7345

Position: -

Target: -

Stop:-

As aussie has retreated after faltering below indicated resistance at 0.7518, retaining our view that minor consolidation below this level would be seen and pullback to 0.7420-25 cannot be ruled out, however, if our view that low has been formed at 0.7329 is correct, downside should be limited to 0.7400-05 and bring another rebound later, above said resistance at 0.7518 would extend the rise from 0.7329 low to resistance at 0.7556, having said that, a break above there is needed to provide confirmation, bring subsequent rise towards 0.7595-00.

In view of this, we are looking to buy aussie on dips as 0.7400-10 should limit downside and bring another rise. A break of support at 0.7388 would abort and signal top is formed, bring further fall to 0.7360 but said recent low at 0.7329 should remain intact. Only a drop below this support at 0.7329 would abort and signal recent decline has resumed and extend weakness to 0.7295-00 (76.4% retracement of 0.7158-0.7750).

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

Will OPEC Deliver A Crude Missile?

Today's OPEC meeting will determine the direction of oil for the coming months with an extension of the production cut widely expected.

Anticipation is building in the oil market as the meeting of OPEC, and Non-Opec members get underway to discuss the joint production cut expiring at the end of the month. In the spirit of “future guidance,” various members of the grouping have signalled that an extension of six months is a done deal and could be as long as nine months.

Markets are certainly liking what they are hearing with both Brent and WTI up over one percent in Asia trading extending the fearsome bull run of the last week or so. OPEC is also being helped by the Americans for a change, with last nights Crude Inventory number coming in at -4.425 million barrels. Twice as high as the anticipated drop and the seventh drop in a row. Even more pleasing was that the gasoline and distillate inventories did not increase to offset it. America, it seems is consuming petroleum products faster then they are pumping them.

So what surprises could OPEC/Non-OPEC spring on us today? The markets seem rather complacent to my eyes and OPEC has proven it can surprise. Possible outcomes could be…

The meeting dissolves in acrimony with no extension. Unlikely to happen of course but this is OPEC. A worst case scenario which would not likely be positive for oil at all!

A six-month extension to the present deal. The baseline case and with oil having rallied so far so soon on it, this could bring profit taking to the market ahead of the weekend. Going forward as U.S. shale increases, it may not be enough to drain the glut, and both contracts have some serious resistance not too far above present levels.

A nine-month extension seems to be getting increasingly priced into crude. It may be bullish initially but could generate the same scenario as number 2 above.

An extension through to the end of 2018. Would most likely be construed as positive for oil and signals OPEC/Non-OPEC's determination and dedication to removing supply imbalances.

An extension and an increase in the production cut. Very tough to achieve given the disparate group but would certainly give the most bang for its buck. Could likely be very bullish for oil prices as long as everyone complies, but that is another story.

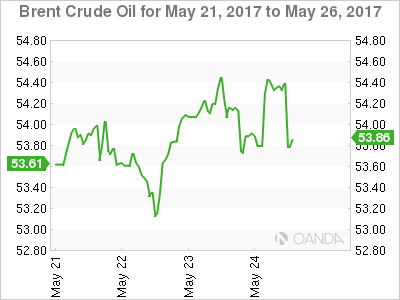

Crude, of course, has continued its march higher from overnight, ahead of today's OPEC meeting.

Brent

Brent spot opened at 53.80 and is trading near its overnight highs of 54.50 with a break through this level targeting 56.50 from a technical perspective. Lying in wait though is the 57.00 level which has capped all rallies in 2017. A daily close above could signal that OPEC has finally got it right. Support is found initially at the 100-day moving average at 53.40 and then 53.00.

WTI

WTI spot opened at and traded 51.00 in early Asia and has traded up to its New York highs at 51.50 before easing 30 cents. A break above 51.50 targets 52.00. A daily close opening a potential of the 54.50 regions, which has capped WTI for all of 2017. Like Brent, a daily close above this level would be a Nirvana moment for OPEC.

Summary

We may be seeing a bit of position reduction and profit taking ahead of the result from Vienna today. The direction of oil is very much in OPEC and Non-OPEC's hands now, but breaking 2017's highs in Brent and WTI may require the grouping to deliver a crude missile of a surprise.

Could USD Rebound After FOMC Less Hawkish Stance?

The FOMC released its May meeting minutes last evening stating that the overall economic assessment was little changed. The Fed sees to raise rates once again is 'soon be appropriate'. Markets assume that it signals a rate hike in June. The minutes also signals further tightening is expected if the incoming economic data shows improved economy. The Fed sees the weak economic performance in Q1 as transitory, caused by soft consumer spending and inventory investment.

Fed members considered it prudent to wait for further evidence that recent economic weakness was transitory before hiking rates again. The tone of the comments was less hawkish than expected with an increased potential for the Fed to hike rates again in June and then pause to consider developments. After the release of the minutes, per CME FedWatch tool, the probability for a June rate hike remains unchanged at 83.1%.

The minutes also signals shrinking the Fed's $4.5 trillion balance sheet in holdings of Treasury and mortgage securities later this year, by allowing a gradual maturity, setting a cap and reducing reinvestments.

After the release of the minutes, the dollar index fell from a 3-day high of 97.36, breaking the support line at 97.00, as US Yields moved lower. During the early European session on Thursday the dollar index hit a 2-day low of 96.79 looking to test the support line at 96.70. USD/JPY retreated from the resistance level at 112.00 and rebounded after testing the support line at 111.50.

Yesterday ECB President Draghi focussed on the risks around Euro-zone financial stability and remained optimistic that the central bank's unorthodox policies did not pose a risk. With the fall in USD, EUR/USD rebounded from a 2-day low of 1.1167, touching a 2-day high of 1.1244. Spot gold rebounded from the significant support line at 1250, touching a 2-day high of 1259.49.

US Equities reacted somewhat favourably to the Federal Reserve minutes with hopes that interest rates would not rise sharply with lower yields providing support. The S&P 500 index gained 0.25%. During the early European session on Thursday, the Dow Jones index reached a high of 21101.25 which was last seen on March 2. The S & P 500 index hit a record high of 2412.68.

The initial USD move seems to deviate from the overall message in the minutes, as markets have priced in the expectations on a June rate hike, and the Fed's hawkish stance appears to be less strong.

With WTI trading higher the market witnessed a degree of profit taking. Latest EIA data recorded a 4.43mn barrel decline in inventories for the latest week. OPEC is scheduled to hold a meeting today in Vienna to discuss whether to extend the existing output cut agreement. The consensus is that OPEC will extend the agreement. It is likely that we will not see a surge after OPEC announces an extension as markets have largely priced in the expectations since May 5.

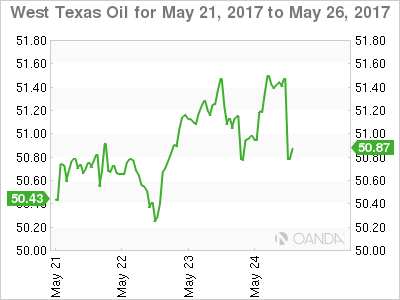

On Wednesday, Brent crude spot hit the highest level of 54.80, last seen on April 19. During early European session on Thursday, WTI spot hit the highest level of 51.96, last seen on April 19.

Bank Of Canada Leaves Monetary Policy Unchanged

'We're slowly but surely moving toward the day when the bank might actually consider raising interest rates. I think that's still a long way down the road, but you've got to walk before you run.' - Doug Porter, BMO Capital Markets

As markets expected, the Bank of Canada left its monetary policy unchanged as its meeting on Wednesday, suggesting that economic growth will likely slow in the June quarter. In a dovish statement, the Bank expressed concerns over capacity utilisation and subdued growth, but noted strong consumer spending, the prosperous housing market and solid job growth. Nevertheless, policymakers voted to keep the benchmark Overnight Rate at a record low of 0.50%. Rates are expected to remain unchanged until 2018. Nevertheless, the Canadian Dollar rose shortly after the release, boosted by expectations of an interest rate hike. According to the Central bank, despite the change of mortgage lending rules, the nation's housing market remained on an expansion path. The BoC Governor Stephen Poloz highlighted that the ratio of household debt to income remained at record highs. The Governor also said that the biggest threat to the economy was arising from the United States and Donald Trump's protectionist policies, as about 75% of Canadian exports go to the US.

US Crude Oil Inventories Fall For Seventh Straight Week

'If OPEC doesn't hold together on this, I think the market will start to test the low $40s again.' - Rory Johnston, Scotiabank

US crude oil inventories dropped for the seventh consecutive time last week, official figures revealed on Wednesday. The Energy Information Administration reported that US crude stockpiles fell 4.4M barrels in the week ended May 19, following the preceding week's decrease of 1.8M barrels and surpassing expectations for a 2.4M barrel decline. Thus, inventories hit 516.3M barrels, the lowest level since mid-February, suggesting that the OPEC production cut deal began working. The data came out a day before the OPEC meeting in Vienna, Austria. Analysts expect that OPEC and non-OPEC countries will likely extend the deal for six more months. Refinery production climbed 159K barrels per day to 17.281M bpd during the reported week, whereas the refinery utilisation rate advanced 0.1% to 93.5%. The four-week average of crude exports rose 30% to 4.7M bpd last week, compared to the same period a year ago. The EIA also reported that inventories at the Cushing, Oklahoma, dropped 741K barrels last week. Oil prices rose shortly after the releases, with WTI futures hitting $51.88 per barrel, the highest since April 19.

New Zealand To Spend NZ$11B On Infrastructure

'They've worked really hard over the past five years to turn deficits into surpluses and when you've got money in the bank it gives you options.' - Cameron Bagrie, ANZ

The government of New Zealand stated it would run a bigger-than-initially-expected budget surplus this year amid additional investments in infrastructure. The government estimated a NZ1.62M surplus in the year to June, compared to its prior projection of a NZ$473M surplus. The Finance Minister Steven Joyce reported that the government would spend extra NZ$11B on infrastructure, including housing, roads, railways and prisons over the next four years. Apart from that, the government said it would spend NZ6.5B to support families through increasing grants and reforming some taxes. The following move is expected to provide support to the current government ahead of the 2018 National Election. New Zealand is also expected to run a trade surplus of NZ$2.85B in the year to June 2018. Meanwhile, the Treasury revised up its economic growth forecast from 3.4% to 3.7% amid the recent rebound in dairy product prices and improving tourism. The Finance Minister also said that the government would invest additional money in the nation's disaster fund, following massive earthquakes Christchurch and Kaikoura.

EUR/USD Analysis: Rebounds Back Above 1.12

'It was supposed to be a year of risk that could lead to a break up of the euro. It's turning out to be the best year in a decade for the shared currency.' – Stefania Spezzati, Bloomberg

Pair's Outlook

On Thursday morning the common European currency was continuing the surge against the US Dollar. The surge began during Wednesday's trading session, when the currency pair remained at a resistance cluster in the expectations of fundamental news from the US Central Bankers. If the pair continues the surge, it is highly likely that after some struggling with weak resistance levels the currency exchange rate will surge to the 1.13 mark. There it will be most likely paused by the weekly R1, which is located at the 1.1306 level.

Traders' Sentiment

SWFX traders have 60% of open positions short, and that same percentage of all trader set up pending orders is set to sell the pair.

GBP/USD Analysis: Risks Ending Consolidation

'There is still scope for further upside in the near term. The long-term downtrend currently stands at approximately 1.35 and it is still possible that we could see that tested before the dollar begins to reassert itself.' – Charles Stanley (based on PoundSterlingLive)

Pair's Outlook

Even though the Cable failed to behave in accordance with expectations yesterday, the consolidation trend still remained intact. Overall, the situation did not change since Wednesday, as the Pound is still required to experience another leg down in order for the trend to continue its existence. The same supports and resistance are in play and technical indicators keep suggesting the GBP/USD pair is to appreciate, meaning that a bullish development is also more than possible, which would, this time, fully break the consolidation trend. However, solid gains beyond 1.3030 are also doubtful due to the absence of a strong market mover.

Traders' Sentiment

There are 52% of traders being short the Sterling against the US Dollar today, while the portion of buy orders inched down from 56 to 52% in the last 24 hours.

USD/JPY Analysis: Stuck Between 110.50 And 112.00

'The rise in Treasury yields is supporting the dollar. It appears that speculative buying of Treasuries has run its course, with Trump concerns and geopolitical risks no longer fresh news.' – Daiwa Securities (based on Reuters)

Pair's Outlook

The US Dollar weakened against the Yen on Wednesday, but managed to avoid serious losses by closing at 111.50. However, further bullish potential is now under question, as the 55-day SMA and the weekly pivot point are once again acting as an immediate supply area. A drop back under 111.00 is always possible, due to lack of supports around that area, leaving the monthly PP at 110.48 as the only possible turnaround point unless losses exceed 150 pips. Technical indicators are unable to confirm the possibility of either the negative or the positive outcome, thus, we should not rule out the chance of another leg up and the potential retake of the 112.00 mark.

Traders' Sentiment

Traders' sentiment remains bearish, with 57% of all open positions being short. Meanwhile, 52% of all pending orders are to buy the Buck.

Gold Analysis: Remains Below 1,260 Level

'I do not think the market's view for two more rate hikes has changed following the release of the Fed meeting minutes.' – Helen Lau, Argonaut Securities (based on Reuters)

Pair's Outlook

As the FOMC Meeting Minutes did not change the opinion of the market participants in regards to US rate hikes this year, the bullion began to regain previously lost ground. However, somewhere around midnight the situation has slightly changed. During the early hours of Thursday's trading session the commodity price had slightly declined, as it must have encountered a smaller timeframe chart's resistance, which keeps the metal form jumping. However, it is most likely that the surge will resume and the 1,270 mark will be reached.

Traders' Sentiment

SWFX traders remain almost neutral, as 51% of open positions are short. However, 68% of trader set up orders are to buy.