Sample Category Title

Fed Holds Rates, Signals No Rush to Start Cutting

The Federal Reserve Open Market Committee (FOMC) maintained the federal funds rate in the 5.25% to 5.50% range and announced it would continue its balance sheet runoff.

The Fed adjusted its language to acknowledge the recent strengthening in economic data, stating "recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have moderated since early last year but remain strong."

With inflation having decelerated in the last few months, the statement added that inflation risks are "moving into better balance."

On the future path of policy, the statement added that "the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent".

All of the members of the FOMC voted in favor of the decision.

Key Implications

We were all keenly attuned to how Chair Powell would change his tone in response to the recent improvement in U.S. inflation. The Fed's preferred core PCE metric has moved to 2.9% year-on-year, with the 3-month annualized figure having moved below the Fed's 2% target (at 1.5%) in December. Powell noted the improvement but highlighted that "ongoing progress is not assured". The need for further evidence that inflation will move to stabilize at 2% was the main theme of Powell's presser today.

Powell's desire for further proof of inflation's trajectory hasn't stopped markets from maintaining 50/50 odds of a cut in March. We believe this timing is premature. While the trend in inflation has been encouraging, the strength of the U.S. economy has given the Fed a free option to wait longer before it cuts rates. Given this economic strength, and with global supply chain issues popping up again, there is risk that inflation could surge higher. This argues for greater patience – a sentiment echoed by Powell as he leaned against market pricing for earlier rate cuts.

Anticipating Fed: Potential Disruptions in Dollar’s Calm

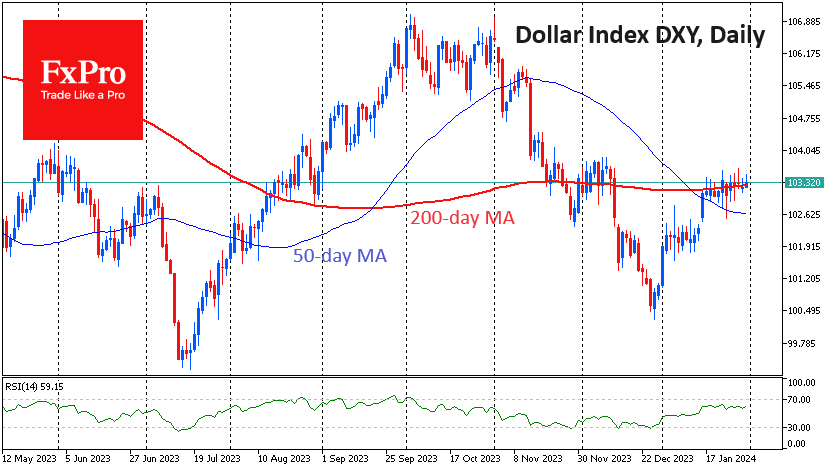

The pause in the currency market is dragging on. Over the past two weeks, the Dollar Index has risen 0.15%, although intraday volatility has been within normal limits. This is by no means a balanced market but rather a manifestation of a wait-and-see attitude.

Wednesday evening is the next FOMC meeting on monetary policy. No changes are expected, but everyone will be watching the wording of the official commentary and Chairman Powell’s answers to questions about the outlook for monetary policy.

A month ago, markets were 90% certain of a rate cut in March. Today, that probability is estimated at 45%. Much of this reassessment has taken place in the last two weeks. Still, it has yet to be reflected in the dollar index rate.

The stabilisation at current levels is also notable from a technical perspective. The Dollar Index is hovering around its 200-day moving average, which is a strong trend indicator for the major players.

Moreover, at the current level of 103.30, the DXY has given back about half of the amplitude of the decline from 107 in early November to 100.3 in late December. The decline began as the Fed signalled the end of its hiking cycle and reached a tipping point when FOMC members began to express overly optimistic expectations about the timing and speed of rate cuts.

The last fortnight has paved the way for a strong move with little indication of direction. Traders should not rush to take sides ahead of Wednesday’s or Friday’s news and join what is likely to be a prolonged trend.

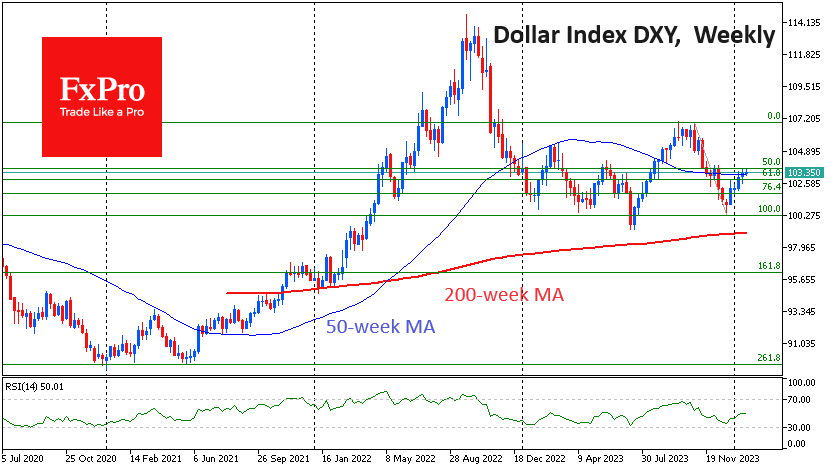

If Powell’s comments reinforce the expectations for a quick and sharp rate cut that have been forming in investors’ minds since the end of last year, the dollar could start to move towards the 95-97 area. The dollar could also return to 90, the area of the 2021 and 2018 lows, within a couple of years.

If the Fed were to adopt a dovish stance, citing upside risks from a strong labour market or fears of repeating the mistakes of the 1980s, this could be the starting point for a dollar rally. Potentially, the US currency would be on its way to the late October high of 107, with a chance of rising to 113 in the two-year outlook.

Sunset Market Commentary

Markets

A busy eco calendar provided some distraction in the run-up to tonight’s FOMC gathering. French January CPI slowed more than forecast in January (-0.2% M/M & 3.4% Y/Y), balancing yesterday’s upward Spanish surprise. German Bunds immediately attempted to gain some momentum, but the move didn’t go that far. German inflation printed as expected at -0.2% M/M with the Y/Y-figure at 3.1% (from 3.8% vs 3.2% expected). National data released so far suggests that aggregate EMU CPI data will tomorrow barely deviate from consensus (-0.4% M/M & 2.7% Y/Y). US Treasuries equally attempted some kind of rally after payrolls processor ADP reported a 107k net job increase for January where markets banked on 150k new jobs. The employment cost index also slowed from 1.1% Q/Q in Q3 to 0.9% Q/Q (vs 1% expected). Data and the soft stock market opening (-1.3% for Nasdaq on earning misses; see graph) push US yields more than 10 bps lower at the front end of the curve, pulling German yields down in the process. EUR/USD rises towards 1.0880 on yield differences. Together with the early US data, the US Treasury announced its quarterly refunding statement. Since August 2023, Treasury has significantly increased issuance sizes. It intends to do so a final time this quarter and believes that the cumulative changes will then leave the US Treasury well positioned to address potential changes to the fiscal outlook. Auction sizes of the 2-yr and 5-yr will be increased by $3bn/month, the 3-yr by $2bn/month and the 7-yr by $1bn/month. The 10-yr and 30-yr will respectively see a $2bn and a $1bn increase for both new issue and reopening with the 20-yr tenor the only one being unchanged. These increases were more or less in line with WS expectations.

The Fed will keep its policy rate unchanged tonight. Back in December, FOMC projections suggested a cumulative 75 bps of rate cuts this year, but Fed Chair Powell didn’t push back against more aggressive market bets at that time. One month and a half onwards, markets are banking on an even steeper path lower with a cumulative 150 bps of rate cuts discounted by the end of the year and the probability of a March cut at 50%. This time we might see Powell being a little more vocal in obstructing that given the outperforming US economy and looser financial conditions. A risk factor is if the Fed plays the “real interest rate” card, aiming to keep that benchmark level as the disinflation process continues. The debate about tapering QT (currently $95b/month) could serve as a lightning rod. Discussing and deciding over QT first buys the central bank some time before moving on to rate cuts. If successful and markets do pare some of the excessive bets, we may see a modest, and likely temporary, yield advance. If US data later this week (payrolls, ISM) underscore the message, there is potential for something more.

News & Views

In an interview with Reuters, Czech National Bank Deputy Governor Jan Frait indicated that he is prepared to support a 50 bps rate cut at next week’s CNB policy meeting. Even a larger cut might be discussed next week. Frait assessed that the annual price mark-ups for goods and services at the start of the year didn’t bring any shocks while at the same time the outlook for growth, household demand and inflation pressures was softening. Frait indicated that he favors more bold steps at the beginning (of the easing cycle) to bring the policy rate to levels that then need finetuning. Frait also expects the quarterly economic update to show a softer economic and inflation outlook. The Czech 2-yr swap rate tumbled 15 bps (4.07%) reaching the lowest level since the CNB stopped raising the policy rate. The krone at EUR/CZK 25.86, is nearing the lowest level since May 2022.

Polish annual GDP growth slowed to 0.2% in 2023, compared to 5.3% growth in 2022 (vs 0.5% consensus). First partial data indicate that gross added value in the industry declined 0.7%. Trade and repair was 2.4% below the level of last year while construction activity grew by 3.4%. In terms of spending, consumptions fell slightly (-0.1%). Gross fixed capital formation was 8% higher compared to the previous year. Softer than expected growth data come as the National Bank of Poland halted its rate cut cycle after a cumulative 100 bps of cuts in October and November. The NBP currently has put further easing on hold as it assesses the impact of fiscal policy of the new government on inflation. At EUR/PLN 4.33 the zloty is holding strong, keeping the December top at 4.2935 within reach.

Will Fed Hint at a March Hike or Just Leave the Door Slightly Ajar?

It's been a relatively slow start to trading on Wednesday which isn't surprising considering what's to come later in the day.

On another day, earnings from Alphabet and Microsoft may have dictated sentiment in the broader markets but as it is, investors are more focused on events in Washington, so tech aside markets are relatively flat.

There's a very good reason why this is the case. Stock markets have been driven by two things over the last year, the explosion of AI and its seemingly endless possibilities and interest rate prospects. The latter is more important for most companies and the economy this year.

Markets have priced rate cuts extremely aggressively over the last couple of months but have pared these back slightly as we've got closer to today's decision. At times, March was viewed as a banker for a rate cut and now it looks more of a coin toss, while in recent weeks 175 basis points were almost fully priced in this year; now it's closer to 125.

Whether that remains the case will partly depend on the Fed's messaging today. Remember, it was the December dot plot that triggered such a flurry of optimism into year-end. Will the Fed further fuel that or push back?

I expect Powell and his colleagues may opt for language that leaves the door open to a rate cut in March without giving the impression that it's likely. Flexibility is key at this stage and there's a lot of important data over the next six weeks that could fully justify beginning the easing cycle and policymakers will be very aware of that.

The ADP employment number was lower than markets expected but I don't think it changes anything for a couple of reasons. The most obvious is that it's been a terrible indicator for the official payroll number so, barring an enormous miss, it should probably be ignored. The other is that employment is no longer as important to the Fed achieving its inflation goal, wages are the more important element of the jobs report.

Middle East tensions and stronger growth boost Oil

Oil prices have pulled back over the last few sessions after surging higher since the start of the year. Middle East tensions and disruptions in the Red Sea appear to be among the driving factors here but there is also the fact that countries continue to resiliently cope with high interest rates, which may soon fall.

The US is at the forefront of this, potentially on course for the fairytale outcome of a strong and growing economy, low inflation, and falling rates. This could boost demand for crude this year more than anticipated and by extension the price.

Will the Fed deliver another boost to Gold prices?

Gold appears stuck between $2,000 and $2,050 at the moment, torn between the prospect of multiple rate cuts this year and those expectations being pared back in recent weeks. There remains a plenty of optimism that rates could fall a lot this year which has enabled the yellow metal to remain above $2,000. But the data needs to deliver and some dovish messaging from the Fed today wouldn't do the price any harm either.

Onwards and upwards for Bitcoin?

Bitcoin has recovered strongly over the last couple of weeks following the post-ETF sell-off. Whether driven by Grayscale outflows or the fact being sold, or a combination of the two, the worst appears to be behind it. That's not to say it's onwards and upwards from here but there'll be some relief that the more than 20% plunge in 12 days is over.

The halving event may provide the next distraction over the next few months but to what extent we can expect it to boost prices is hard to say. Other factors could be supportive though such as an improved risk environment and falling interest rates.

Canada’s Economy Beat Expectations in November, Strong Growth Expected for December

The Canadian economy bucked the trend of flat growth over the past several months, growing by 0.2% on a month-on-month (m/m) basis in November. This print comes in above Statistics Canada's advanced guidance and market expectations for a 0.1% m/m gain. The flash estimate for December points to a healthy advance of 0.3% m/m.

November's reading was broad-based, with output expanding in 13 of 20 industries. The gain was led by goods-producing industries (+0.6% m/m), while the services side eked out a 0.1% m/m gain.

On the goods side, gains in both non-durable (+1.2% m/m) and durable goods manufacturing (+0.6% m/m) helped the sector chalk up the biggest contribution to the monthly GDP gain. Growth in mining, quarrying, and oil & gas (+0.3% m/m) and agriculture (2.4% m/m) provided an assist to November's growth.

On the services side, a rebound in wholesale trade (+0.7% m/m), led by motor vehicles (+2.6% m/m), did most of the heavy lifting. Transportation and warehousing also grew by a healthy +0.8% m/m. Services gains were offset by a 0.3% m/m slip in educational services as a result of the Quebec strikes, retail trade (-0.1% m/m) and finance and insurance (-0.2% m/m).

The advanced reading of 0.3% m/m growth in December was driven by increases in manufacturing, real estate, and oil & gas. December's education services and construction were cited as headwinds.

Key Implications

November's GDP print surprised against expectations that the economy would advance at a more modest 0.1% m/m pace. With today's print and guidance for a December GDP rebound, fourth-quarter GDP is tracking just over 1% quarter-on-quarter annualized. This is roughly in line with our own expectations and materially above that of the Bank of Canada's (BoC) newly revised projection of no growth.

The Canadian economy looks to be finishing the year on a stronger note than most expected. Markets are still focused on the timing of rate cuts, but a heating up of the Canadian economy may push expectations for a first cut further down the line. Markets are leaning towards a rate cut by the spring, when it is expected that trends in both growth and inflation will be in the Bank's comfort zone. While the BoC remains in a holding pattern as it awaits confirmation that inflation will decisively settle at their 2% inflation target, strong data prints like today's GDP release will be keeping the Bank on their toes.

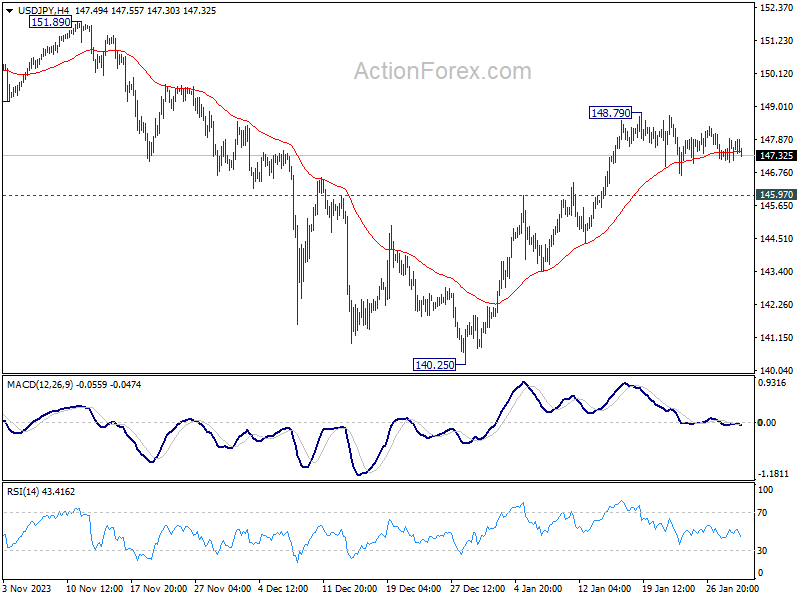

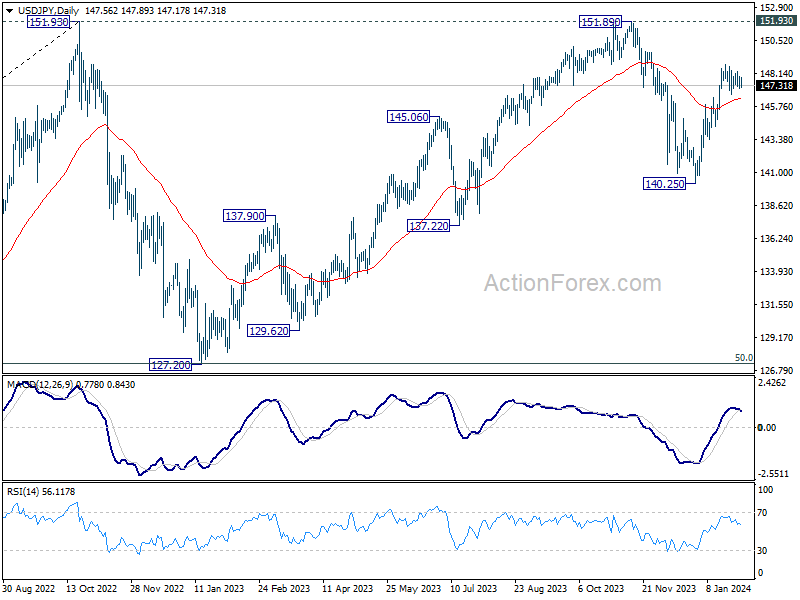

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.16; (P) 147.54; (R1) 147.99; More...

USD/JPY's consolidation from 148.79 is still in progress and intraday bias remains neutral. With 145.97 resistance turned support intact, further rally is in favor. As noted before, corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 142.33) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

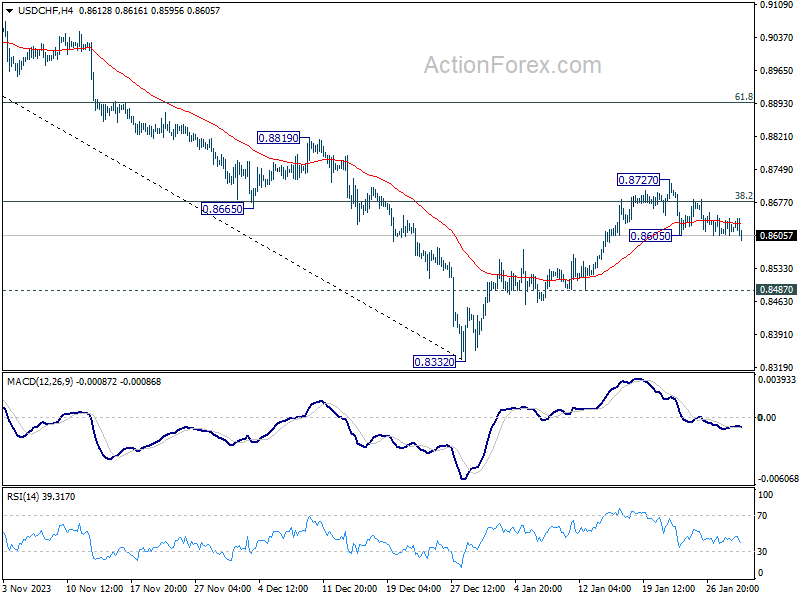

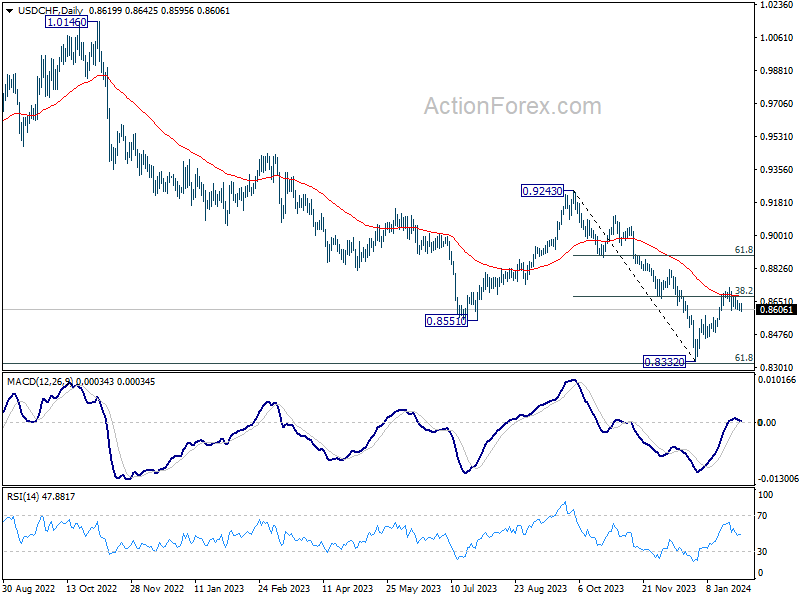

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8602; (P) 0.8622; (R1) 0.8639; More....

USD/CHF's fall from 0.8727 resumed by breaking 0.8605 temporary low. Intraday bias is back on the downside for 0.8487 support. Break there will argue that rebound from 0.8332 has completed, and bring retest of this low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

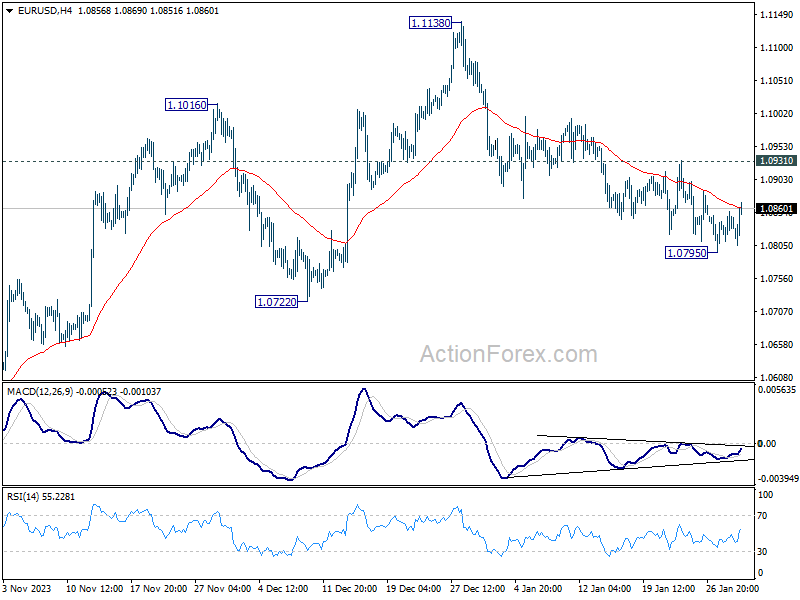

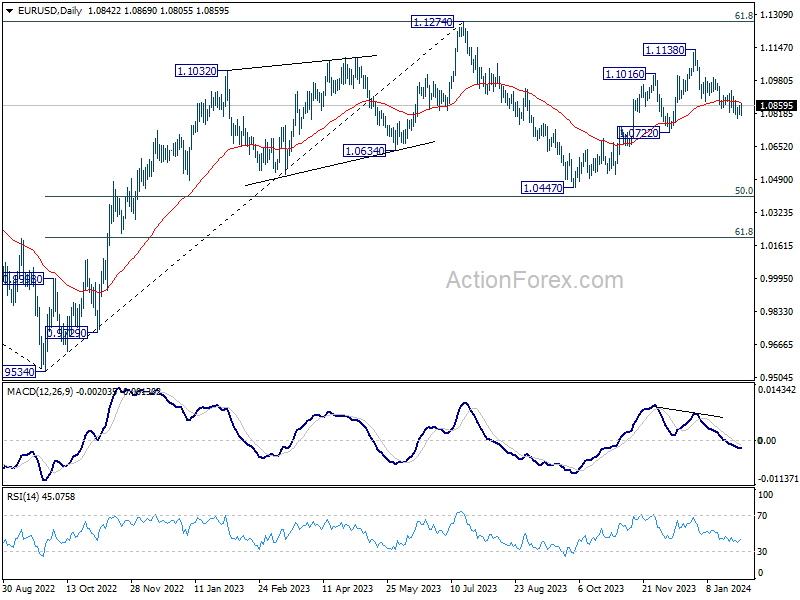

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0820; (P) 1.0838; (R1) 1.0865; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. But further decline is expected as long as 1.0931 minor resistance holds. Below 1.0795 will resume the fall from 1.1138 to 1.0722 structural support next. On the upside, however, break of 1.0931 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

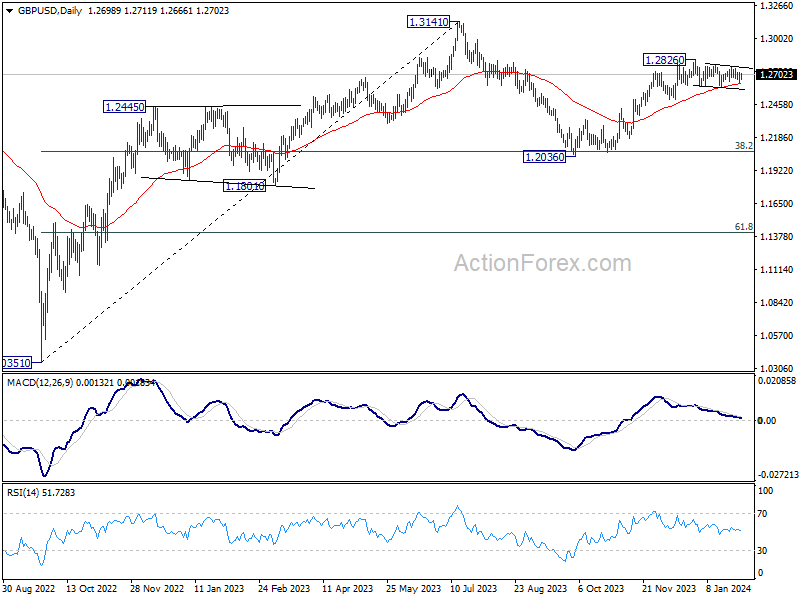

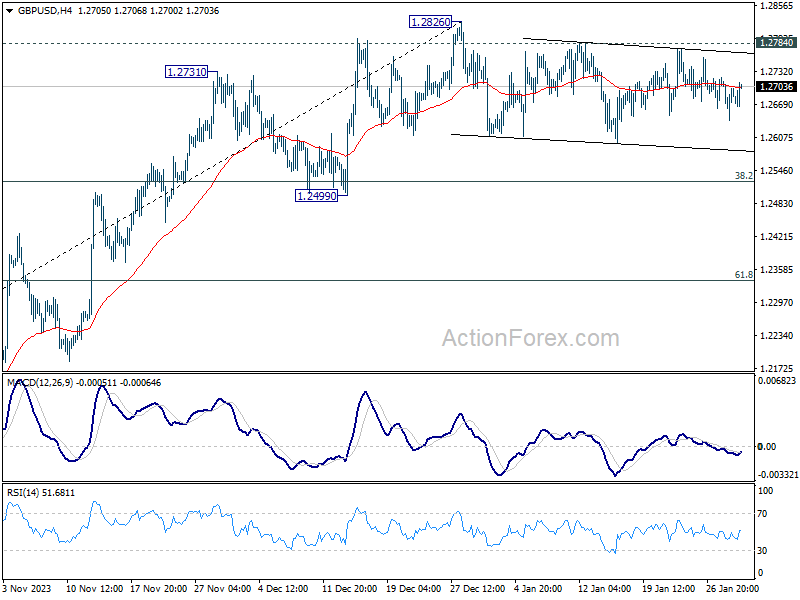

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2653; (P) 1.2687; (R1) 1.2734; More...

Range trading continues in GBP/USD and intraday bias remains neutral. Another fall cannot be ruled out, but downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.