Sample Category Title

Gold Consolidates After Correction As Traders Await Fresh Catalysts

Key Highlights

- Gold started a consolidation phase after a dip to $3,885.

- A contracting triangle is forming with support at $3,970 on the 4-hour chart.

- WTI Crude Oil prices could struggle to recover above $62.20.

- EUR/USD is again moving lower and could drop to 1.1450.

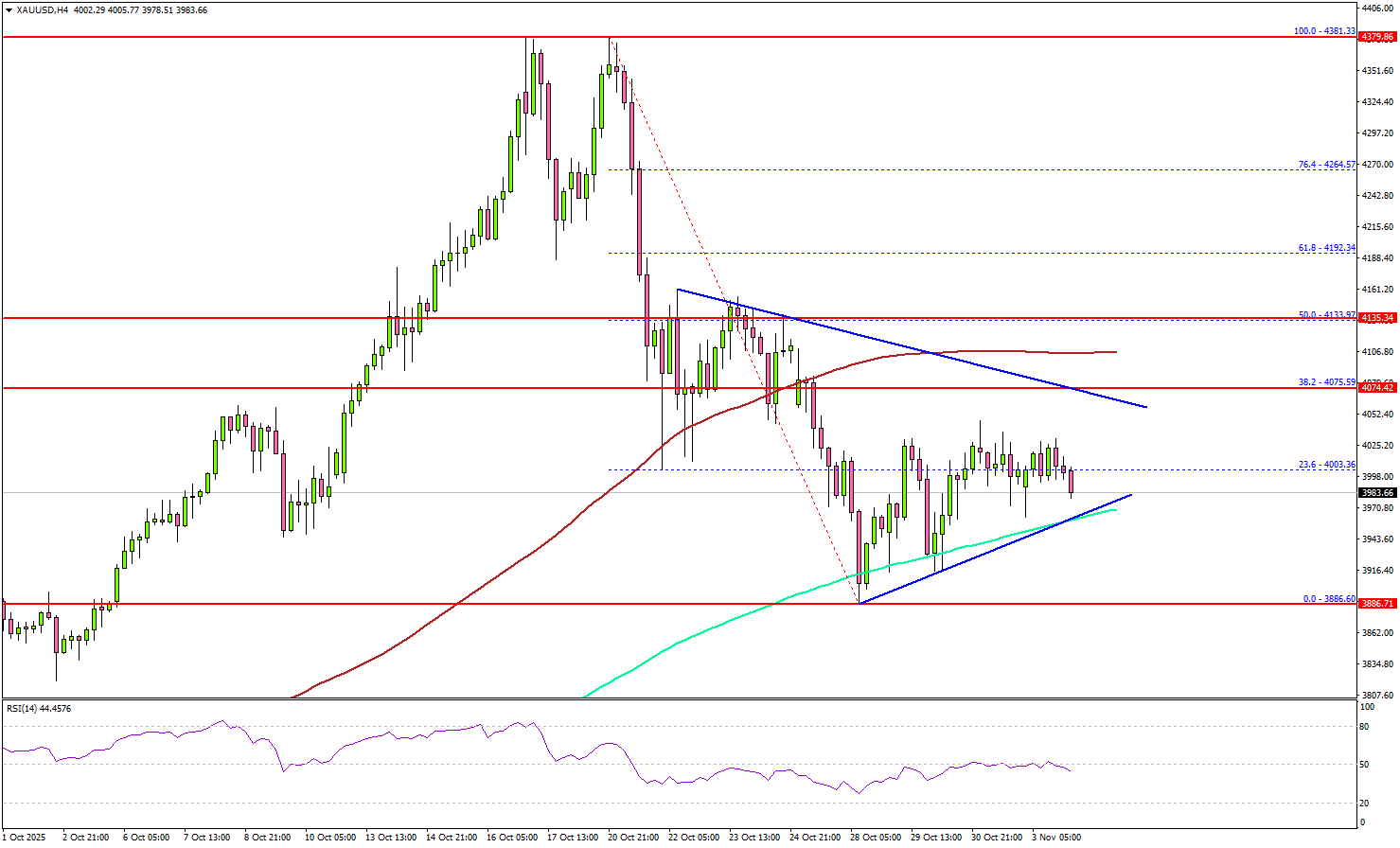

Gold Price Technical Analysis

Gold prices corrected some gains and traded below $4,000 against the US Dollar. It even tested $3,885 before starting a consolidation phase.

The 4-hour chart of XAU/USD indicates that the price settled below the 100 Simple Moving Average (red, 4 hours) but stayed above the 200 Simple Moving Average (green, 4 hours).

Recently, there was a move above the 23.6% Fib retracement level of the downward move from the $4,381 swing high to the $3,886 low. On the upside, immediate resistance is near the $4,070 level. The next major resistance sits near the $4,100 level.

A clear move above $4,100 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $4,135 and the 50% Fib retracement level of the downward move from the $4,381 swing high to the $3,886 low.

On the downside, initial support is near the $3,970 level. There is also a contracting triangle forming with support at $3,970. The first key support is $3,945. The next major support is near the $3,885 level. A downside break below $3,885 might call for more downsides. The next key zone to watch could be $3,800.

Looking at WTI Crude Oil, the price attempted a decent recovery wave, but the bears remained active below the $62.50 level.

Economic Releases to Watch Today

- ECB's President Lagarde speech.

- Fed's Bowman speech.

- BoE's Breeden speech.

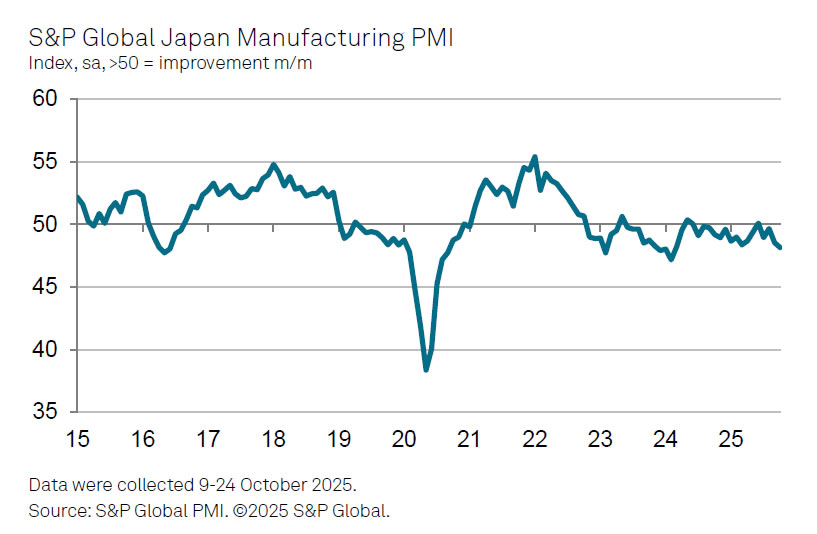

Japan’s PMI manufacturing finalized at 48.2, but sentiment shows improvement

Japan’s manufacturing sector contracted again in October, with the final S&P Global PMI edging down to 48.2 from 48.5 in September. According to S&P Global’s Pollyanna De Lima, demand softness — particularly in the automotive and semiconductor sectors — triggered the sharpest fall in new orders since early 2024, while exports to Asia, Europe, and the U.S. continued to decline.

Manufacturers also faced rising cost pressures, as higher input costs squeezed margins even as demand waned. To offset these pressures, many firms lifted selling prices despite intense competition for new business.

Still, sentiment showed some improvement. The decline in production was relatively contained, and many firms expressed greater optimism about future output. Hopes for successful new product launches and expectations that the impact of U.S. tariffs will eventually fade helped boost confidence.

Fed’s Cook: Every meeting is live, December included

Fed Governor Lisa Cook said she supported last week’s quarter-point rate cut, describing it as “another gradual step toward normalization.” Cook noted that she views current policy as “modestly restrictive,” which remains appropriate given that inflation is still above target. At the same time, she argued that “downside risks to employment are greater than the upside risks to inflation,” suggesting a tilt toward caution on the growth side of the Fed’s dual mandate.

Cook emphasized that monetary policy is “not on a predetermined path”. She said the economy is at a moment when risks to both sides of the mandate are elevated: keeping rates too high could cause a sharp labor-market deterioration, while cutting too aggressively could risk unanchoring inflation expectations. .

Looking ahead, Cook stressed that each meeting remains a “live meeting,” including December’s. She will base her decision on incoming data and shifts in the economic outlook, particularly regarding labor conditions and inflation persistence.

Fed’s Daly keeps open mind on December, sees labor market still stable

San Francisco Fed President Mary Daly said she supported last week’s rate cut and will approach the December meeting with “an open mind”. She believed it was “appropriate to take another bit off the policy rate,” while emphasizing that the central bank must now gauge whether the 50 basis points of easing delivered this year are sufficient to guard against further weakness in hiring.

She noted that incoming data, including state-level jobless claims, suggest the labor market is not on a “precipice,” with conditions still stable despite slower momentum. Inflation, she said, is running near 3%, indicating progress but not yet a full return to target.

Daly added that FOMC participants often hold diverse views ahead of meetings, but consensus tends to emerge as new data clarify the outlook.

Gold (XAU/USD) Price Forecast: Bullion Buoyant Above $4,000, Now Looks for Support Ahead of ADP Payrolls

Trading at $4,008 well into the US session, up +0.14% in today’s trading, gold bullion continues to look for support at the key psychological level of $4,000.

With the US government shutdown still ongoing, US data releases remain sparse.

Eyes now turn to the private release of ADP payrolls this Wednesday, which will likely offer some insight into how the Fed will continue its easing cycle.

Join me as I attempt to answer the $4,008 dollar question:

How will gold (XAU/USD) fare in this week’s trading?

Gold (XAU/USD): Key takeaways 03/11/2025

- Cooling after a period of significant upside, gold bullion has found some support at the key psychological level of $4,000, with Thursday’s price action showing a persistent level of bullish interest

- Priced in for some time, last week’s rate cut by the FOMC offered a hawkish tilt, with Chair Powell making some suggestion that this could be the final rate cut of the year, which, in theory, would be negative for gold pricing

- With the dollar continuing to fresh highs in today’s session, gold has not only become more expensive for international buyers, but the associated rise in short-term bond yields is increasing the opportunity cost of holding gold bullion, hurting pricing

Gold (XAU/USD): Safe at $4,000

Although I don’t wish to speak too soon, gold pricing is looking relatively stable above $4,000.

Despite the recent downside, which, by most metrics, was entirely inevitable after the explosive rally, gold remains on a firm fundamental and technical footing, with the current consolidation necessary if the yellow metal is to move higher.

With that said, this is market commentary, as in, what’s happening now, so allow me to explain some of the key macroeconomic headwinds currently at play in the precious metal markets.

Let’s discuss.

Gold (XAU/USD) vs Dollar Strength Index (DXY), D1, OANDA & TVC, TradingView,

Gold (XAU/USD): Fundamental Analysis 03/11/2025

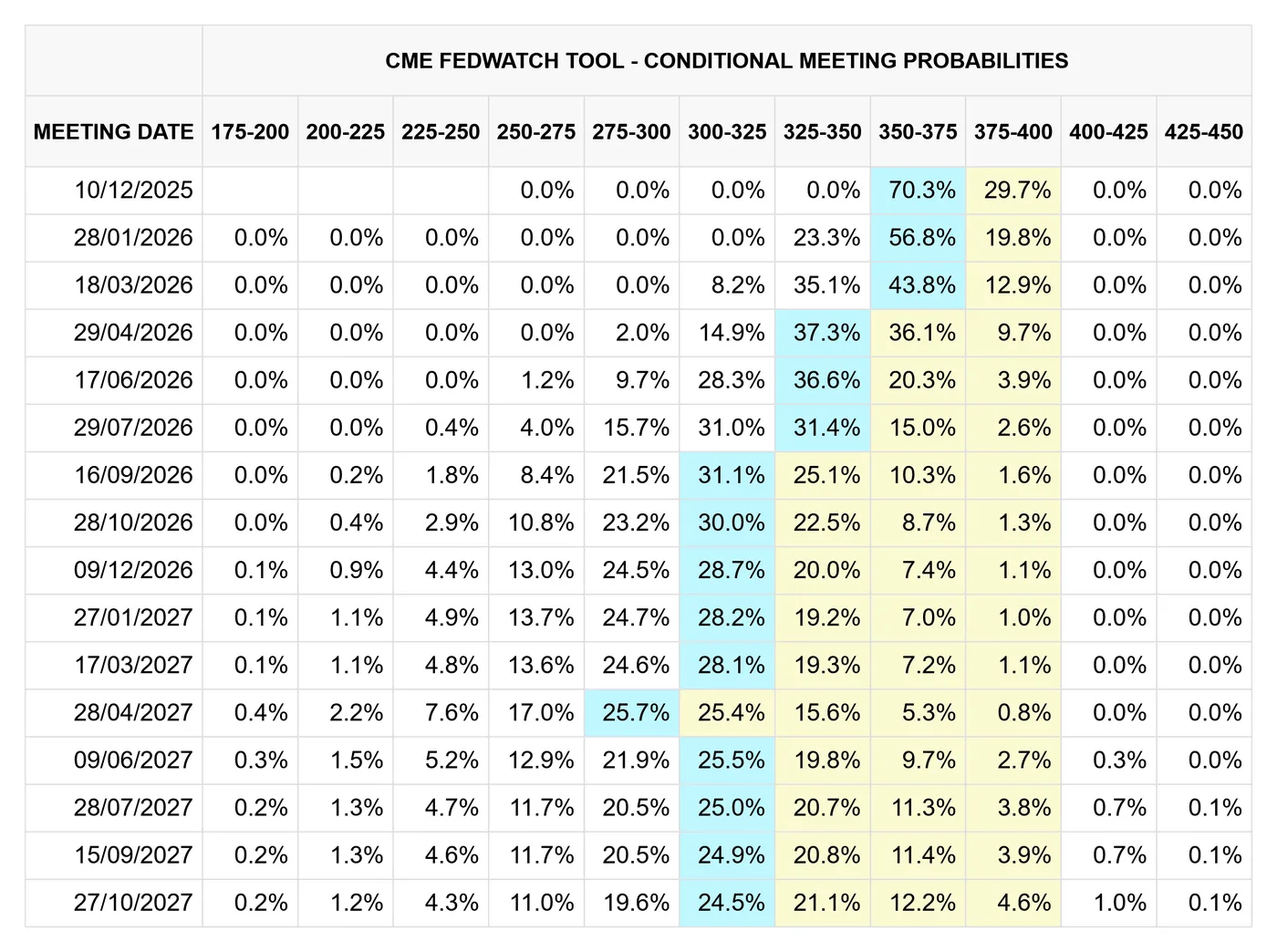

Hawkish commentary from Fed Chair Powell: Starting with the most significant of the three themes, last week’s interest cut of 25 basis points by the Federal Reserve was met with hawkish commentary from Jerome Powell, citing a need for “data-driven caution”.

These comments come at an interesting time, within the context of a full US government lockdown, where data that the Fed would otherwise rely on to guide its decisions, such as PCE, CPI, and NFP, is entirely unavailable.

The ongoing government shutdown is now only two days shy of being the longest in history, currently at 34 days.

Therefore, considering Powell’s comments, markets have somewhat repriced the probability of a December rate cut from approximately 90% down to 70%, with some surprised at the Fed Chair’s hawkish undertones.

CME FedWatch, 03/11/2025

Although markets still overwhelmingly predict rates will be cut in the Fed’s final decision of 2025, the notion that the Federal Reserve is becoming more hawkish directly challenges the current gold rally, with lower interest rates favouring higher bullion prices.

With Stephen Mirran speaking earlier today, notably more dovish amongst his fellow policymakers, markets will continue to refine expectations ahead of December 10th.

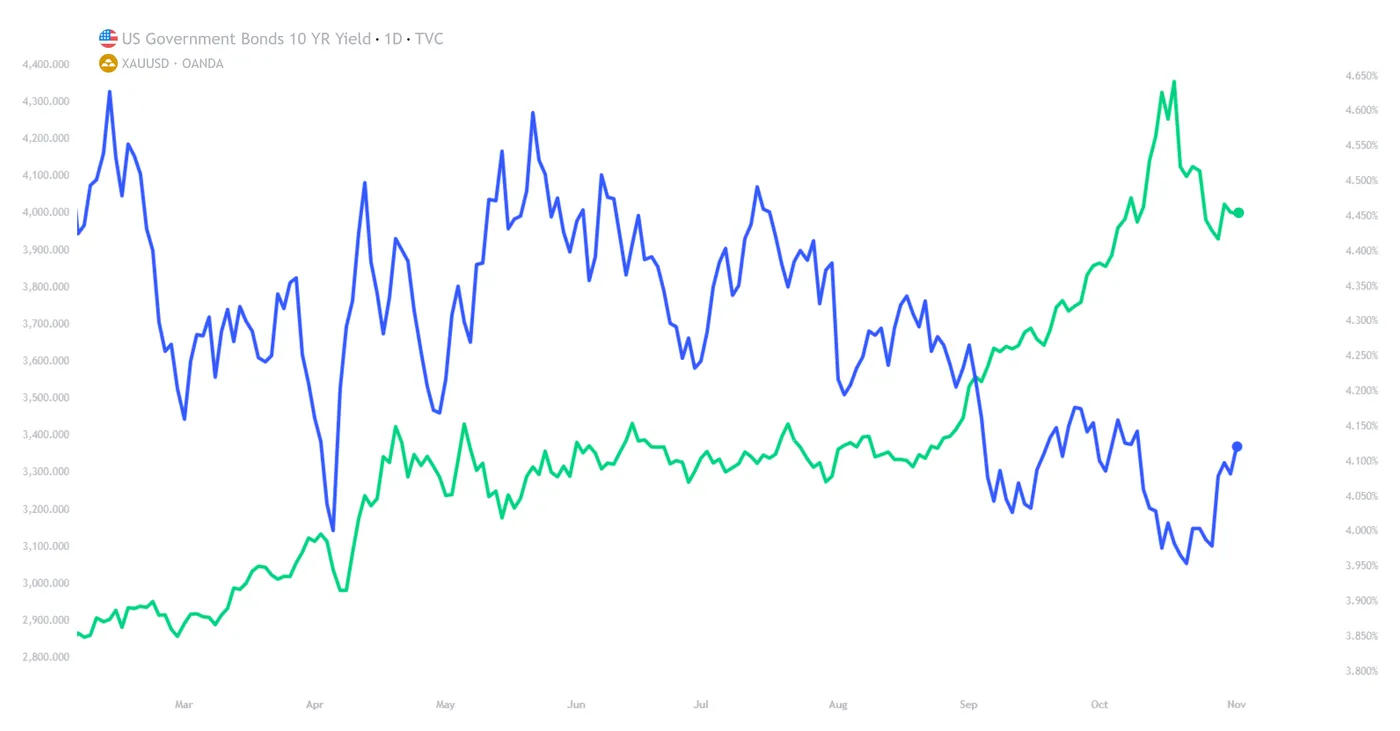

Rising dollar and increasing bond yields: Now I’ve set up the premise of a more hawkish Fed than once thought, a further two knock-on effects have been the following:

- A rally in dollar pricing, which now trades at 3-month highs

While it is possible for metals to rally alongside a strengthening dollar, rising USD value makes gold more expensive to buy with non-dollar currencies, hurting international investment.

- Rising short-term bond yields, with the 10YR rising to 4.11%, its highest level since early October

This increases the attractiveness of holding government debt when compared to precious metals, hurting bullion pricing

Gold (XAU/USD) vs US 10-Year Bond Yield (US10Y), D1, OANDA & TVC, TradingView, 03/11/2025

Put simply, a more hawkish Fed often means higher interest rates, which is inherently bad for gold pricing.

Easing of US-China tensions: To conclude our fundamental analysis for today, it would be remiss not to mention how easing tensions between President Xi and President Trump has effectively removed a significant headwind that was otherwise offering upside to gold pricing.

Following the recent agreement on a tariff truce, the risk premium priced into gold has been significantly reduced, resulting in lower pricing.

Gold (XAU/USD): Technical Analysis 03/11/2025

XAUUSD, D1, OANDA, TradingView, 03/11/2025

As stipulated in my commentary a couple of weeks ago, gold did breach the key psychological level of $4,000 and continued lower to the first resistance level of approximately ~$3,889.

What’s happened since, however, is more a following of the first scenario:

Gold price action will form a base, consolidate, and stage another leg higher, aiming to overcome resistance held at ~$4,240

Technically, gold remains well supported at both $4,000 and $3,889, although a move below the latter could spell trouble for gold pricing, with the next stop being at the 50-period SMA.

To the upside, which bulls will be keen to hear, we can expect our next reasonable price target to be at the 20-period moving average, roughly at $4,090.

Otherwise, our secondary target would be at the previous support-turned-resistance level at $4,240, and then aim to surpass the all-time high of $4,381.

Price targets and support/resistance levels:

- Price target #1 - 50-period SMA - $4,090

- Price target #2 - Previous support turned resistance - $4,240

- Price target #3 - All-time highs - $4,381

- Support #1 - Key psychological level - $4,000

- Support #2 - Swing low - $3,889

- Support #3 - 50-period SMA - $3,834

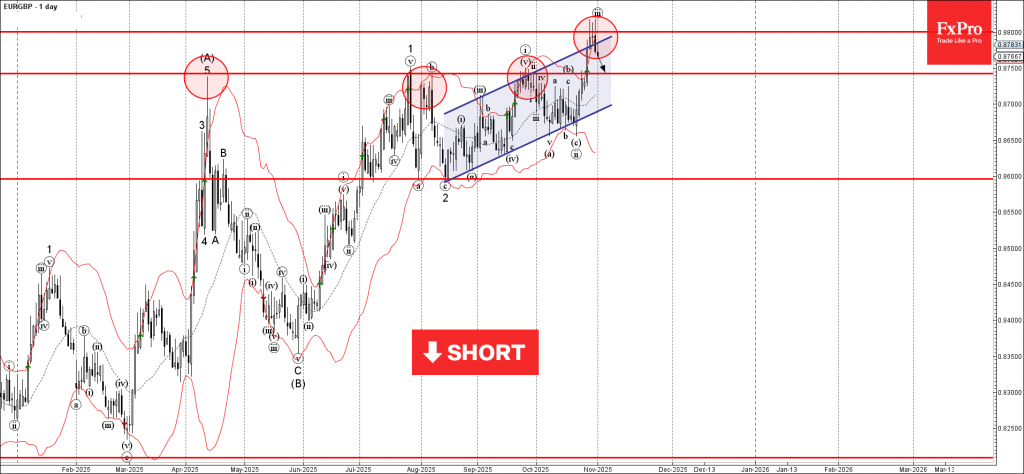

EURGBP Wave Analysis

EURGBP: ⬇️ Sell

- EURGBP reversed from resistance zone

- Likely to fall to support level 0.8750

EURGBP currency pair recently reversed from the resistance zone between the resistance level 0.8800, resistance trendline of the daily up channel from September and the upper daily Bollinger Band.

The downward reversal from resistance level 0.8800 created the daily Japanese candlesticks reversal pattern Evening Star Doji – with the middle candle being Shooting Star.

Given the strength of the resistance level 0.8800, EURGBP currency pair can be expected to fall to the next support level 0.8750, former strong resistance from April, July, August and September.

Fed’s Goolsbee cautions against front-loaded cuts, undecided with December

Chicago Fed President Austan Goolsbee said he remains uneasy about the idea of front-loading rate cuts, citing persistent inflation pressures and an uncertain growth backdrop. Speaking with Yahoo Finance, Goolsbee admitted he is “not decided” going into the December meeting, emphasizing that inflation remains “above target for four and a half years and trending the wrong way.” .

Goolsbee added that the threshold for cutting rates is now higher than at prior meetings. While he acknowledged that interest rates should ultimately fall alongside inflation, he expects them to settle “a fair bit below current levels” only once inflation shows sustained progress toward 2%. His stance aligns with other centrist officials who are reluctant to accelerate rate cuts amid mixed economic signals.

On the labor market, Goolsbee described an unusual environment of “low hiring” and “low firing,” calling the hiring rate one of the economy’s weakest points. Despite slower job creation, he noted that broader employment indicators remain stable.

ISM Manufacturing Index Shows Eighth Consecutive Month of Contraction

The ISM Manufacturing Index fell to 48.7 in October, reversing September's increase and returning to the level we saw in August.

Six of 18 industries reported growth last month, up from five in September. But it was smaller industries that reported growth this month, accounting for only 58% of manufacturing GDP compared to 70% last month.

Demand conditions improved in October. New orders, new export orders, backlog of orders, and customers inventories all improved, but remain in contractionary territory.

The production index declined to 48.2 in October after spiking up to 51.0 in September, close to the 47.8 it had registered in August, making its time in expansionary territory short-lived.

Price gains decelerated again in October, coming in at 58.0 vs. 61.9 in August. Prices are still increasing, but at a slower rate.

Key Implications

Although manufacturing activity contracted at a faster pace in October, there are some welcome signs in this report. All the demand indicators improved, albeit remaining very weak, and the price index remains elevated, but eased. On the supply side, while production and employment indexes both declined, the low reading on customers' inventories is usually a sign of future production increases, which could be positive for manufacturing output in future months if demand indicators continue to improve. The moderation in the price index adds to the case for the Federal Reserve to reduce interest rates again, and carries added importance given that it seems October CPI is unlikely to be released anytime soon due to the government shutdown.

Survey respondents continue to report substantial struggles with adjusting to tariffs, in addition to weak demand conditions. Some respondents identify added costs from tariffs, volatility in prices of their imports, and a lack of success in attempts to reshore production. Some respondents also noted that tariffs are driving up their prices, but it is either not possible to source their imported inputs domestically or it is still cost effective to import, leading to cost and price increases. These are all factors that make it difficult to increase capacity or expand.

Sunset Market Commentary

Markets

Last week’s ECB and even more Fed policy decisions helped to put a floor for EMU and US yields and this pattern still was the ‘by-default bias’ at the start of this week. Admittedly, the filtering-through of (mainly German) fiscal intentions to support growth develops at slower pace than hoped for. Even so, the 0.2% Q/Q EMU Q3 growth didn’t call for ECB support anytime soon and confirms the view that downside risks to growth have diminished. At the same time, inflation has landed close to the 2% target. In this context, Slovak ECB member Kazimir warned against ‘over-engineering‘ and fine-tuning the inflation dynamics to perfection. In doing so, the ECB at some point risks becoming a source of volatility rather than stability. German yields in technical trading today at 2-3 bps across the curve. Markets again see a <50% probability of a potential ‘fine-finetuning’ rate cut somewhere next year. Last week’s hawkish/no-consensus-driven Fed rate cut also still helps US yields cautiously higher from the support levels tested before the Fed decision. The 2-y yield (3.60%) left the 3.50% area. The 10-y yield (4.11%) again settles well north of 4%. US yields in a slight steepening move are rising further between 3 bps (2-y) and 3.2 bps (30-y). Some analyses also question whether heavy issuance for tech majors to finance AI related investments at some point by become a competitor for US Treasuries. At the moment of finishing this report, the US manufacturing ISM at 48.7 (from 49.1) printed slightly softer than expected (49.5). Subindices were mixed with prices also slightly softer than expected (58 from 61.9) but employment and new orders marginally better. The impact on markets remains limited for now. This weekend’s OPEC+ decision to continue with a small 137k b/d production hike in December before shifting to a pause in Q1 next year, had little impact on the oil price (and on broader markets, including inflation expectations). Brent oil even eases slightly today ($ 64.7 p/b). For equities the ‘by-default’ bias remains to hover near recent top levels even as momentum isn’t really that convincing anymore (EuroStoxx 50 +0.3%, Nasdaq +0.7%).

Section three of the ‘buy-default-continuation trade’ applies to the US dollar. An ‘a bit higher, probably for a bit longer’ US interest rate scenario, a lack of outright positive eco news from other major economies (Japan, EMU, China, Europe, the UK) and a feeling that the risk rally might have run the easiest part of its course still support the greenback. DXY (99.95) is only a whisker away from the 100 barrier with the early August top at 101.25. EUR/USD dropped below the 1.1542 October low, accelerating losses to 1.1515. After substantial losses last week, sterling started the week in more of a wait-and-see modus ahead of Thursday’s BoE policy decision. EUR/GBP (0.877) at least didn’t push any further on last week’s attempt to break the 0.88 barrier. We stay cautious on sterling. An unexpected BoE rate cut probably won’t help the UK currency. However, is the BoE holding rates unchanged as it sees it hands tied by too high inflation better news for sterling? In CE, the forint near EUR/HUF 386.7 touched the strongest level against the euro since end May last year.

News & Views

Swiss consumer prices fell by 0.3% m/m in October, more than the -0.1% expected and deepening from September’s -0.2%. Annual inflation missed the 0.3% consensus estimate as well by coming in at a mere 0.1%. The Federal Statistical Office singled out several factors to explain the price drop, including lower prices for hotels and international package holidays and for the hire of private means of transport. Clothing & footwear, housing maintenance and caretaking, by contrast, recorded a price increases. Core inflation unexpectedly slowed as well, from 0.7% to 0.5%. The Swiss franc weakened to its lowest level in around three weeks. EUR/CHF at 0.93 remains historically strong though. Bets for another rate cut by the Swiss National Bank are gradually building meanwhile. That would bring the policy rate back, currently 0%, into negative territory. It remains nothing but a tail risk so far. Swiss policymakers including SNB chair Schlegel have signaled a high bar for going negative again.

The Czech ANO party, which won the most votes in October’s election but fell short of a majority, has signed a coalition agreement today with the Motorists and the Freedom and Direct Democracy (SPD). The former is a Eurosceptic movement which campaigned against the EU’s climate goals and the latter is considered an anti-immigrant party, making the agreement a consolidation of the rightwing populist bloc. The stage is now set for ANO’s leader Babis to return as prime minister. A preliminary outline of the program manifesto included a cap to the retirement age at 65 and a pledge to stick to the koruna throughout their term.