Sample Category Title

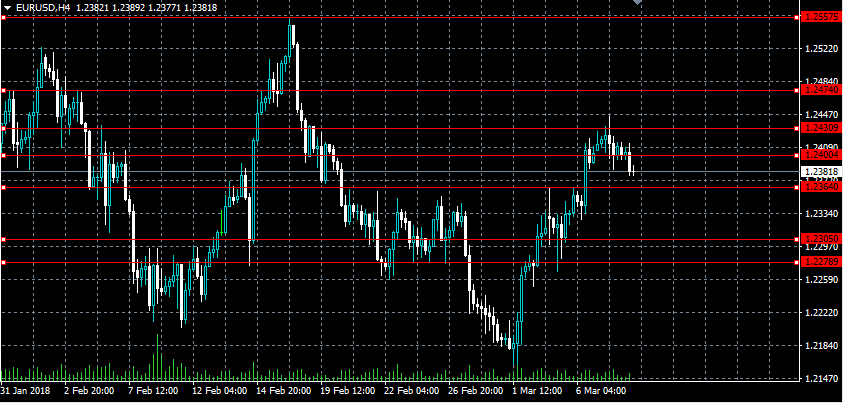

Key EURUSD Levels Ahead Of ECB Decision

The euro continues to consolidate around the 1.2400 handle against the U.S dollar, ahead of today’s ECB interest rate decision and policy statement from European Central Bank President Mario Draghi. The EURUSD pair failed to gain traction above the key 1.2430 level on Wednesday, with traders now taking profits as fears grow ECB President Draghi may discuss the negative impacts of a strong euro currency and U.S trade tariffs. Traders are likely to continue to watch the 1.2430 level for further upside, whilst the 1.2278 now acts as critical weekly support.

The EURUSD is likely to turn bullish above the 1.2430 level, with intraday buyers targeting the 1.2470 and 1.2557 levels.

Should the EURUSD pair fail to move back above the 1.2430 level, price-action may turn bearish toward the 1.2305 and 1.2278 levels.

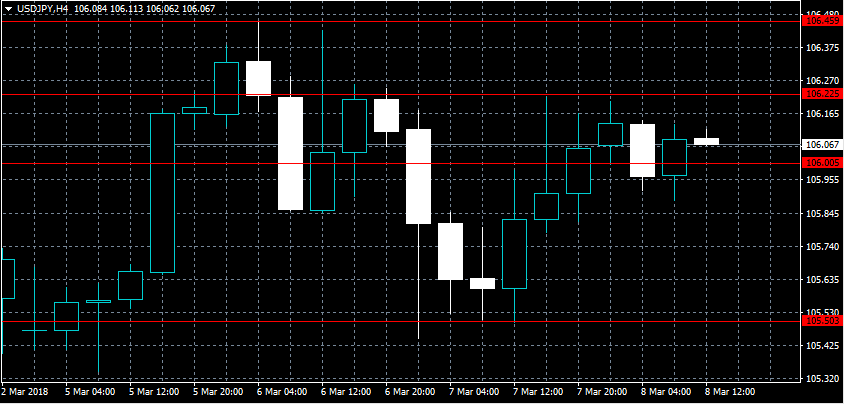

USDJPY Gaining Traction Above 106.00 Level

The U.S dollar has regained upside momentum against the Japanese yen during a quiet European trading session, with intraday buyers reclaiming the 106.00 handle. The USDJPY pair has suffered from depressed trading volumes, with price-action moving in a thirty-point trading-range ahead of a series of market risk-events. USDJPY traders now look towards the upcoming BOJ policy decision and Friday’s Non-farm payrolls job report for February.

The USDJPY pair is likely to edge higher whilst trading above the 106.00 level, further intraday upside towards the 106.22 and 106.45 levels remains possible.

Should USDJPY price-action move convincingly below the 106.00 level, sellers may test towards the 105.50 and 105.24 support regions.

DAX Lower On Soft German Industrial Report, ECB Decision Next

The DAX has lost ground in the Thursday session, after strong gains on Wednesday. Currently, the DAX is trading at 12,205.00, down 0.33% since the Wednesday close. On the release front, German Factory Orders declined 3.9%, weaker than the estimate of -1.9%. This marked the steepest decline since January 2017. Later in the day, the ECB releases its rate decision, followed by a press conference with Mario Draghi.

Global stock markets have been volatile since lat week, when US President Trump stunned investors last week when he proposed stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. Fears of a trade war sent the DAX sharply lower last week, with losses of 5.2%. The DAX has clawed back some of the losses this week, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. This has raised hopes that Trump will back down. However, the unpredictable president could barrel ahead and impose the tariffs, which would likely send global stock markets lower. There was further drama on Wednesday, as Gary Cohn, Trump’s chief economic adviser, resigned. Cohn was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility in the markets.

Euro Dips Ahead Of ECB Rate Decision

The euro has edged lower in the Thursday session. Currently, EUR/USD is trading at 1.2376, down 0.28% on the day. On the release front, German Factory Orders declined 3.9%, weaker than the estimate of -1.9%. This marked the steepest decline since January 2017. Later in the day, the ECB releases its rate decision, followed by a press conference with Mario Draghi. In the US, today’s key indicator is unemployment claims.

Investors are keeping a close eye on the ECB, which will set the benchmark rate on Thursday. This will be followed by a press conference with Mario Draghi. Interest rate levels are expected to remain at a flat 0.0%, where they have been pegged for the past two years. What could move the markets, however, is the language used in the press release following the rate decision, as well as Draghi’s press conference. The ECB has continuously included an easing bias, which means that it could increase or extend asset purchases if the economic outlook worsens. If the Bank removes this line, it would represent a less dovish stance, which could push the euro higher. Starting in January, the ECB reduced its monthly asset purchases to EUR 30 billion, and this stimulus program is scheduled to wind up in September. The Bank could extend purchases past this date, although such a move would likely not stir up the markets.

Investors continue to track the latest developments in the tariff crisis, which has shaken up the markets over the past week. President Trump’s threat to impose stiff tariffs on steel imports has infuriated US trading partners, as well as sharp criticism from senior Republican lawmakers. There was further drama on Tuesday, as Gary Cohn, Trump’s chief economic adviser, resigned. Cohnn was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility in the markets.

Markets Calm Ahead Of ECB Decision

It's been a relatively calm start to trading on Thursday, as we wait for the latest monetary policy announcement from the ECB and, more importantly, the statement and press conference that accompanies it.

It's not uncommon for markets to be a little quieter in the lead up to major central bank decisions, even those that don't promise to be overly eventful. The ECB extended its bond buying program at the start of the year at a rate of €30 billion per month, with the expiry now pushed back to September this year. It's so far kept its cards close to its chest regarding how it will handle the next taper, but many anticipate it will either end altogether in September or be extended to the end of the year at a reduced rate. Either way, the end of QE is near.

Which of these it opts for, assuming the speculation is accurate, is quite irrelevant, investors are more interested in how long after we can expect the first interest rate hike, with some pencilling one in next year. Anyone hoping to extract this kind of information from the ECB and its President Mario Draghi though will likely be disappointed. Instead, all we're likely to get today is a slight change in the language, with the possible removal of a willingness to increase the asset purchase program in size or duration if the outlook becomes less favourable.

While this may not seem like much, it is the gradual shift in policy stance that policy makers have been alluding to that will signal the end of QE later this year and is indicative of a central bank that is becoming less dovish and more optimistic on the economy. While the recovery remains fragile, the euro area economy is performing well and we are seeing what looks like a sustainable improvement. If that starts to filter through into higher inflation as labour market slack diminishes, it may force the ECB to consider rate hikes earlier than is currently expected.

ECB aside there isn't too much on the radar on Thursday. We'll hear from two Bank of Canada officials, including Governor Stephen Poloz, while US jobless claims are the only notable release on the data side. Traders may have one eye on the US jobs report on Friday, with the Federal Reserve now considering additional rate hikes on the back of tax reform providing additional stimulus in an already strong economy.

Fundamentals: Forex, Gold, Oil & Cryptos

Dollar strength was mitigated by a widening US trade deficit

Resignation of Gary Cohn the Whitehouse is now left without any heavyweight advocate

Forex

Encouraging data on domestic private hiring and labour costs reinforced the view of underlying strength in the US economy pushing it higher against currencies such as the Swiss Franc. However, dollar strength was mitigated by a widening US trade deficit for January, and many investors were favouring the yen as a safe haven asset over the dollar after anxiety of a deterioration of global trade. Despite a strengthening dollar, the euro still managed to make ground against the dollar, now trading above 1.241. Tomorrow, Draghi is likely to err on the side of caution amidst the tightening of global trade tensions. Although Brexit is still causing major headwinds for the Sterling, it too crept higher against the greenback.

Gold

The dollar succeeding to recouping some of yesterday’s losses up 0.2% against a weighted basket of currencies coupled with strengthening US equities saw Gold lose most of yesterday’s gains. However, following the resignation of Gary Cohn, Trump’s top economic adviser, the Whitehouse is now left without any heavyweight advocate of globalisation, reigniting fears of a global trade war which would provide a significant impetus for investors to back the precious metal.

Oil

Forecasts that US Crude Oil inventories increased by 3000k weren’t yet priced into the market as exemplified by the fact that an increase by 2400k was still enough to send US Oil down nearly 2% to $61. With prospects of the likelihood a global trade war increasing after comments that the EU would retaliate to Trump’s tariffs, the oil industry, an industry that thrives off of globalisation, would be negatively impacted.

Cryptocurrency

The cryptocurrency market takes yet another slump after speculation that Binance, one of the world’s largest cryptocurrency trading platforms has been hacked. Bitcoin dips below $10000 but hopefully the continuation of increased adoption in the economy will provide investors with more confidence in this new asset class.

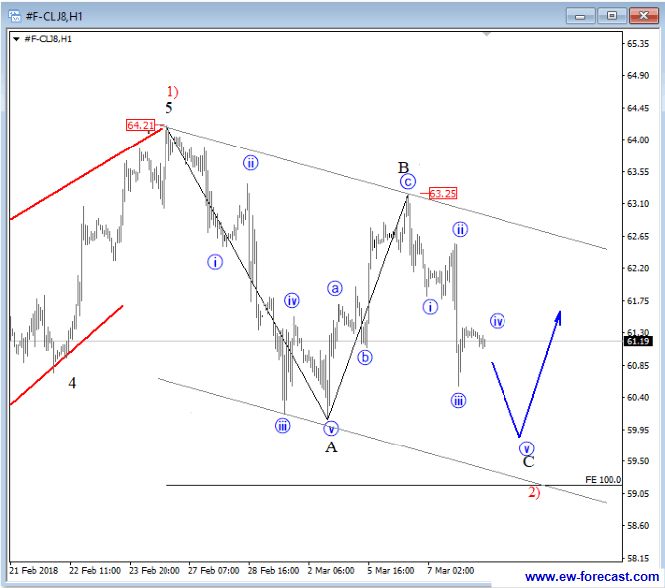

Elliott Wave Analysis: Crude Oil, BTCUSD And USDCAD

Crude oil came lower yesterday but still not into the bear market, as leg down from 63.25 can be wave C of a zigzag down from 64.21 as shown on the updated wave structure. Pay attention to 59.00 area where bounce can occur.

Crude oil, 1H

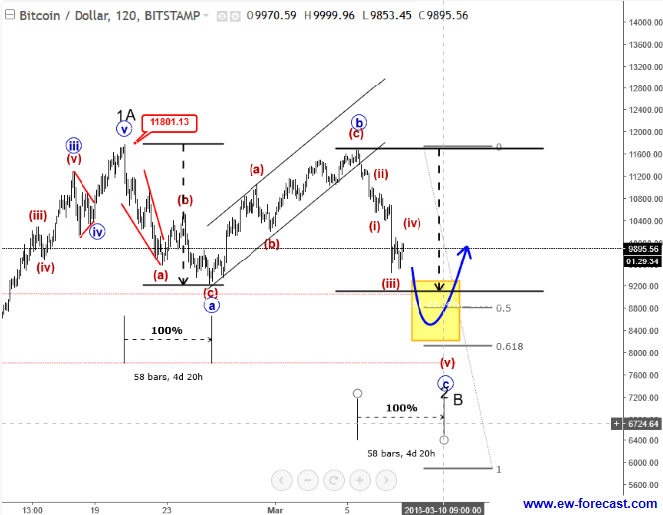

Crypto market is lower for the last 48 hours and this weakness we can label as wave c. So far there was a nice reaction down, a clear impulse so watch out for a five wave drop before market may see support; ideally, that will be at 8k-9k area, where a new bounce can occur.

BTCUSD, 2H

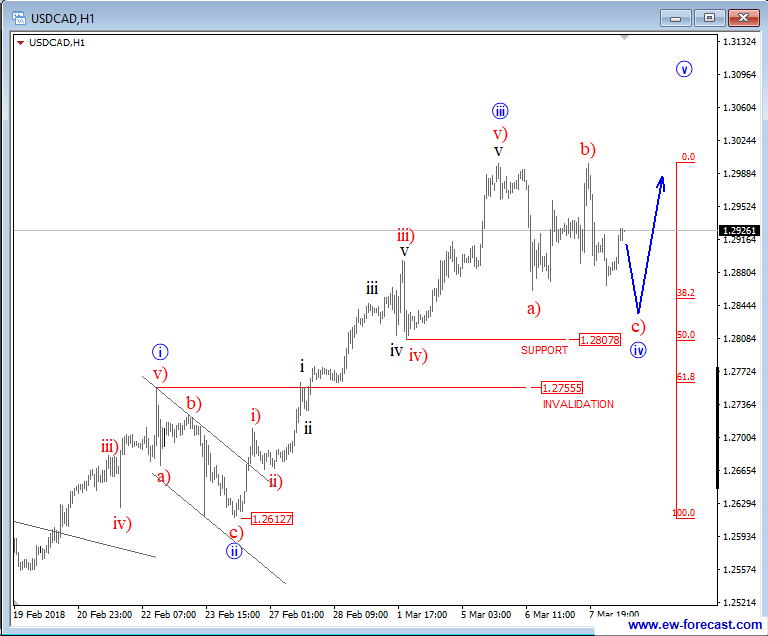

USDCAD came nicely lower since yesterday; it looks like a wave c) of a three wave structure in wave four which can already be searching for support this morning. Ideally a bounce will come from around 1.2850, while pair trades above 1.2755 invalidation mark.

USDCAD, 1H

Euro Jittery Ahead Of ECB Meeting

There was suspense in the air during Thursday's trading session ahead of the European Central Bank policy meeting.

Although markets widely expect the ECB to leave monetary policy unchanged in March, speculation remains elevated over the central bank dropping its “easing bias”. This move is likely to be interpreted as an early step towards policy normalization – ultimately supporting the Euro. While the ECB could continue expressing optimism over the Eurozone economy, concerns over low inflation and an unwelcome return of political risk in Europe have the ability to keep the central bank on standby.

Investors will direct their attention towards Mario Draghi's press conference later in the day for fresh insight on what could happen after September, when QE is expected to come to an end. With political risk in Europe weighing on sentiment and trade war fears lingering in the background, Draghi could end up disappointing markets today.

Focusing on the technical perspective, the EURUSD edged lower on Thursday, with prices trading around 1.2390 as of writing. Any signs of Draghi striking a cautious tone during his conference could weaken the Euro. A decisive breakout and daily close above the 1.2440 level could encourage an incline higher towards 1.2500. Alternatively, a failure for bulls to conquer 1.2440 could result in a decline lower towards 1.2300.

Dollar attempts to claw back losses

The Dollar edged higher against a basket of major currencies on Thursday, as investors attempted to look beyond the unexpected resignation of White House's chief economic advisor Gary Cohn -focusing on Friday's NFP instead. Bulls could be instilled with fresh inspiration to elevate the Greenback, if NFP and wage growth figures exceed market expectations. While speculation of higher US interest rates may push prices higher, anxiety over a potential trade war has the ability to limit upside gains. Dollar volatility is likely to become a dominant market theme, as investors continue to tussle with the conflicting fundamental themes driving the currency.

From a technical standpoint, the Dollar Index remains at threat of extending losses if bulls are unable to push prices back above 90.00.

Commodity spotlight – Gold

Gold edged slightly lower on Thursday, with prices trading towards $1324.50 as of writing.

It has certainly been a rollercoaster week for the yellow metal, as the combination of political uncertainty and US rate hike expectations attracted both buyers and sellers. Much attention will be directed towards Friday's NFP report, which could play arole in how Gold concludes this week. A strong US jobs report may encourage bears to drag prices below $1324. From a technical standpoint, sustained weakness below $1324 could invite a decline towards $1310 and $1300, respectively. Alternatively, if bulls can defend $1324 then $1340 is on the cards.

CRUDE OIL Decreasing Below 61.50

Crude oil upward trend is fading after reaching the 64 range. The pair exited the short-term upward trend channel, heading for hourly support at 59.72 (15/02/2018 low). Hourly resistance remains at 64.77 (11/01/2018 high). The technical structure suggests further shortterm decline.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Short-Term Decline Continues

Silver coninues its descent, trading below 16.50 and approaching hourly support at 16.25 (01/12/2017 low). Hourly resistance at 16.98 (15/02/2018 high) remains. The short-term technical structure suggests further short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).