Sample Category Title

WTI Oil – Daily Cloud Base Holds for Now But Risk for Further Weakness Persists

WTI oil remains in red on Thursday as negative sentiment increased after downbeat supply data on Wednesday, which added to existing pressure on concerns over possible trade war. Fresh downside attempts on Thursday were so far contained by the base of thick daily cloud ($60.91) after previous day's dip to below cloud base was short-lived. Techs continue to work in favor of bears as daily MA's returned to bearish setup and 14-d momentum is probing into negative territory. Bears look for eventual close below cracked support at $61.32 (Fibo 61.8% of $60.12/$63.26 upleg) to generate fresh bearish signal which would be reinforced by close below cloud base, for final push towards key support at $60.12 (02 Mar trough). Immediate downside risk would remain on hold while cloud base hold, but close above broken 20SMA ($61.55) is needed generate initial bullish signal.

Res: 61.55; 61.91; 62.25; 62.63

Sup: 60.91; 60.57; 60.12; 59.48

Sunset Market Commentary

Markets

German Bunds opened in positive territory, but gradually returned the initial gains as global sentiment on risk improved. Investors were also looking forward to the ECB policy announcement. In the policy statement, the ECB omitted its easing bias as it didn't repeat its intention to increase bond buying if necessary. European yields jumped up to 4 bp higher upon the publication of the statement. During the ECB press conference, the 2018 growth forecast was revised slightly higher but the bank decreased the inflation forecast for 2019. The ECB president admitted that the change in the language on QE was unanimous, but at the same time said that no victory can't be declared on inflation yet. The initial rise in EMU interest rates was reversed during the press conference. At the time of writing, German yields are little changed across the curve. On the intra-EMU bond markets, yield spread chances versus Germany mostly narrowed further with Greece (-10bp), Spain and Portugal (-6/-5bp) outperforming and Italy (+4bp) underperforming. The changes in US Treasury yields are much more contained. Markets' angst on an outright trade war eased, but the issue of the US putting import tariffs in place isn't out of the way yet. US yields decline between 0.6 bp (2-y) and 3.0 bp (30-y) in rather volatile trading.

The dollar gained modest ground against the euro and yen as risk sentiment on improved. Investor fears on an outright trade war eased as the White House indicated that import tariffs could be applied in a selective way. The euro jumped temporary higher as the ECB dropped its indication that it could still raise the amount of asset purchases if needed. However, the euro strength was short-lived as other elements in the ECB assessment were little changed. Draghi indicated that the removal of this easing bias should be considered as mostly backward looking. The ECB president also said that the EBC is monitoring FX volatility as a factor in its policy assessment. In line with EMU yields, the euro reversed initial gains during the press conference. EUR/USD trades currently in the 1.2350 area, slightly lower on a daily basis. USD/JPY is little changed hovering near the 106 level.

Sterling trading was mostly driven by global factors today as there were no important UK eco data. EUR/GBP mostly followed the intraday swings of the single currency due the ECB policy statement and during the ECB press conference. The pair trades marginally lower on a daily basis. (currently 0.8915 area). The post-Drahgi reversal of EUR/USD is also slightly weighing on cable. The pair trades currently in the 1.3850 area.

News Headlines

German factory orders declined a bigger than expected 3.9% M/M in January. The consensus estimate only expected a decline of 1.8% M/M. Orders for German factories were still 8.2% higher compared to the same month last year. A sharp fall in orders from other EMU countries was the culprit behind the decline. Statistical issues with respect to year-end factory closures might have distorted the data.

Ratings agency Moody's cut Turkey's sovereign rating one notch further into junk territory. The rating was put at Ba2 with a stable outlook. Moody's said the government appears to be focused on short-term measures. It also mentioned erosion of the strength of the country's institutions and the increased risks from its current account deficit.

The Italian League Party is rumoured to hold informal talks with dissidents of the center-left Democratic Party to seek support for a governing alliance. Both parties didn't answer questions on the issue.

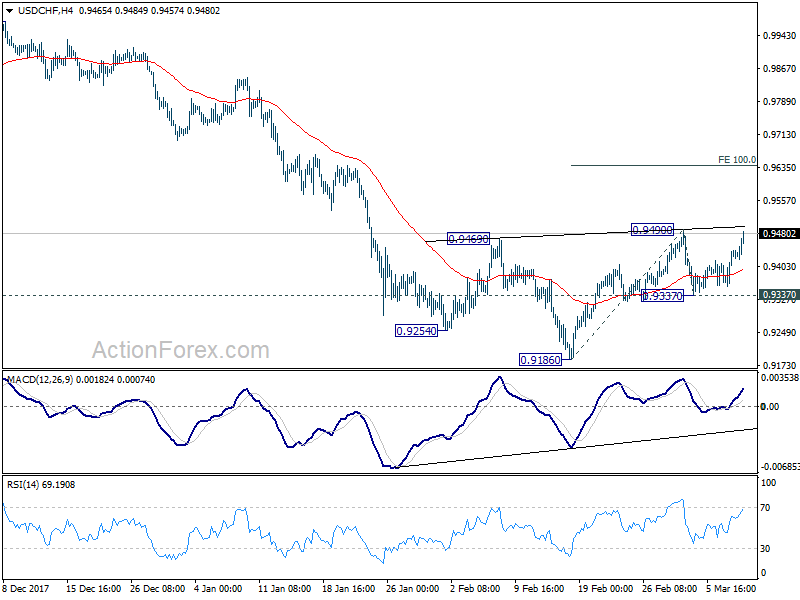

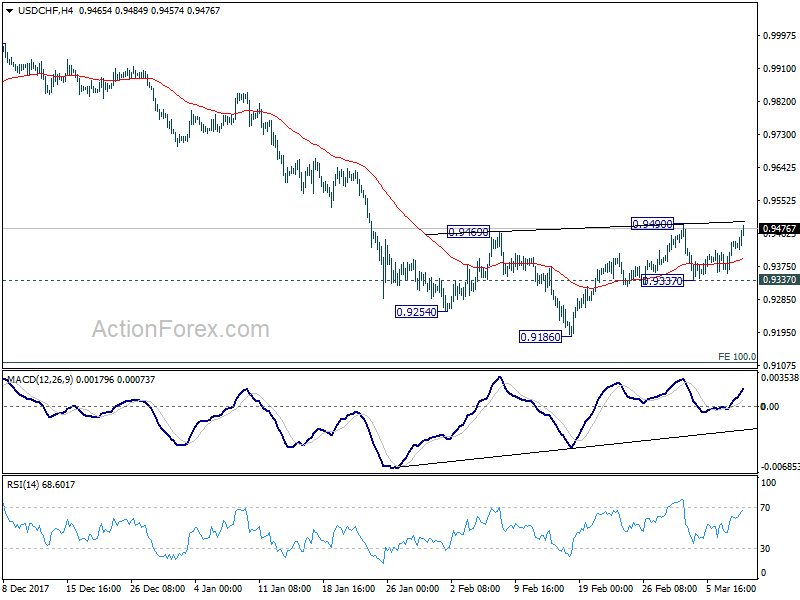

USD/CHF forming head and shoulder bottom

USD/CHF is a pair to watch for the rest of US session as it's pressing 0.9490 resitsance. Break there will complete a head and shoulder bottom pattern. LS: 0.9254, H: 0.9186, RS: 0.9337. In that case, further rise would be seen to 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9464. And as USD/CHF could have reversed its down trend, there would be prospect of a test on 0.9977 further down the road. But agian, that's subject to a solid break of 0.9490 first.

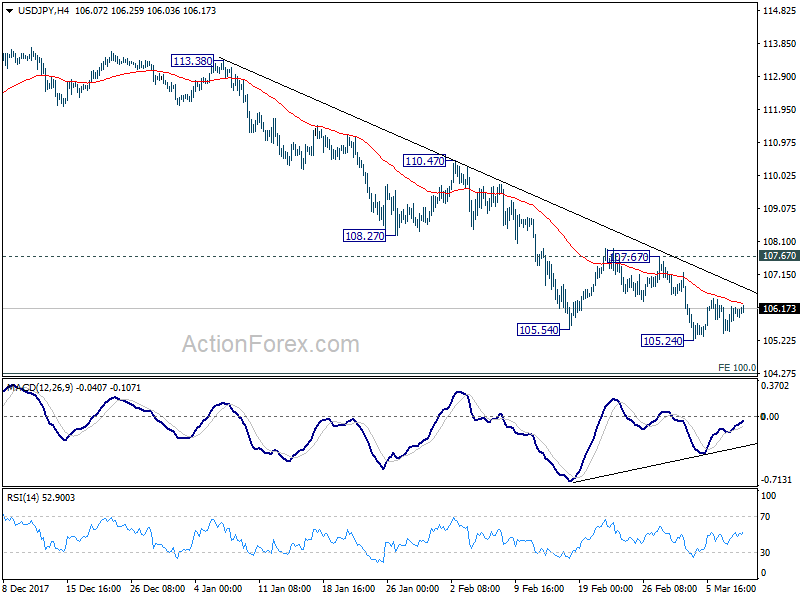

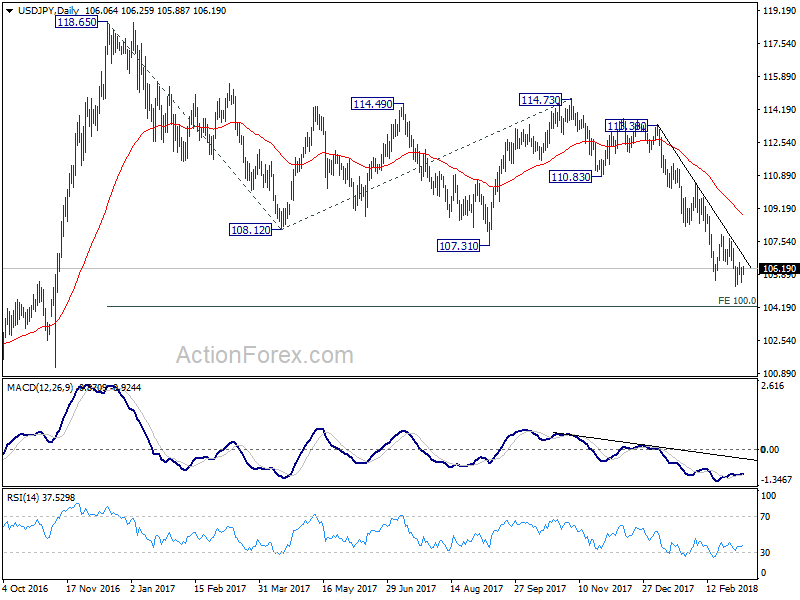

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.60; (P) 105.91; (R1) 106.37; More...

USD/JPY continues to be bounded in consolidation above 105.24 and intraday bias remains neutral. With 107.67 resistance intact, near term outlook stays bearish and further fall is expected. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. However, break of 107.67 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 55 day EMA (now at 108.93) first.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

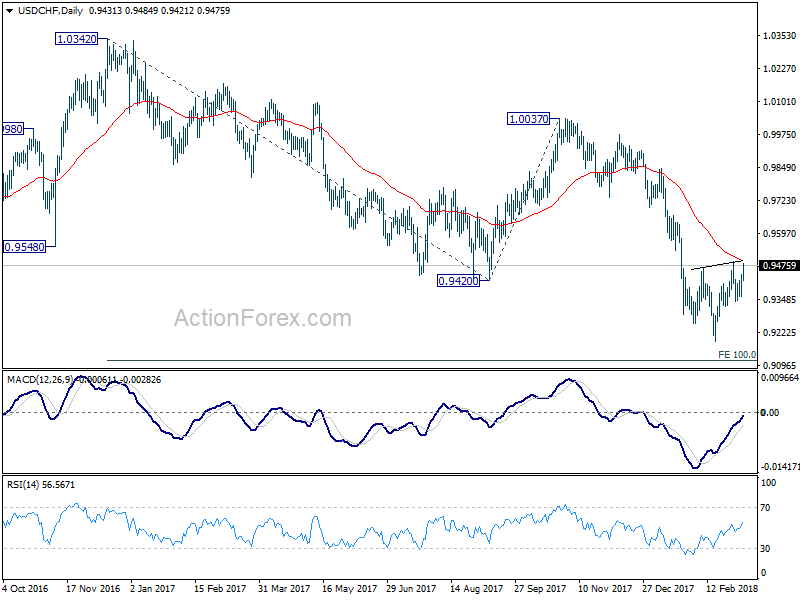

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9380; (P) 0.9411; (R1) 0.9465; More...

USD/CHF rises to as high as 0.9484 and focus in now on 0.9490 resistance. Break till revive the case of near term reversal. And that is supported by head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). In that case, near term outlook will be turned bullish for a test on 1.0037 resistance. Nonetheless, break of 0.9337 should send USD/CHF through 0.9186 to resume larger down trend to 0.9115 projection level.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

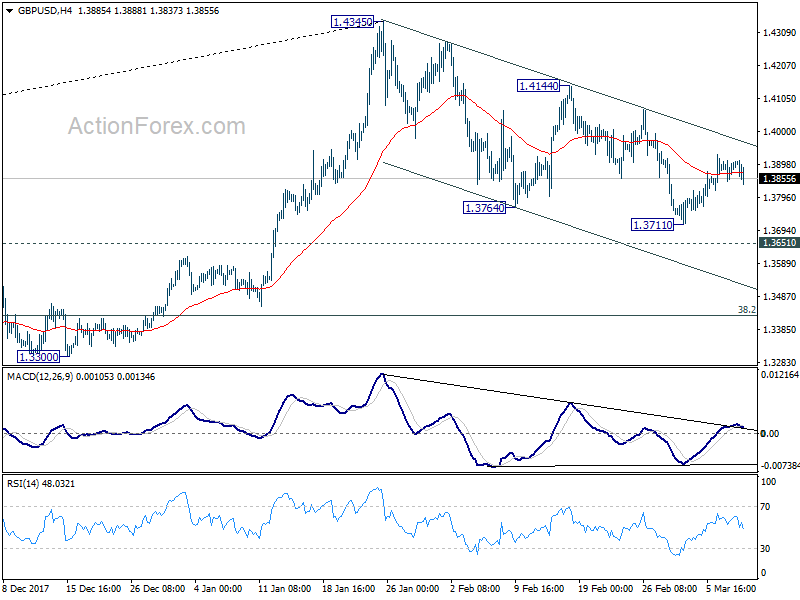

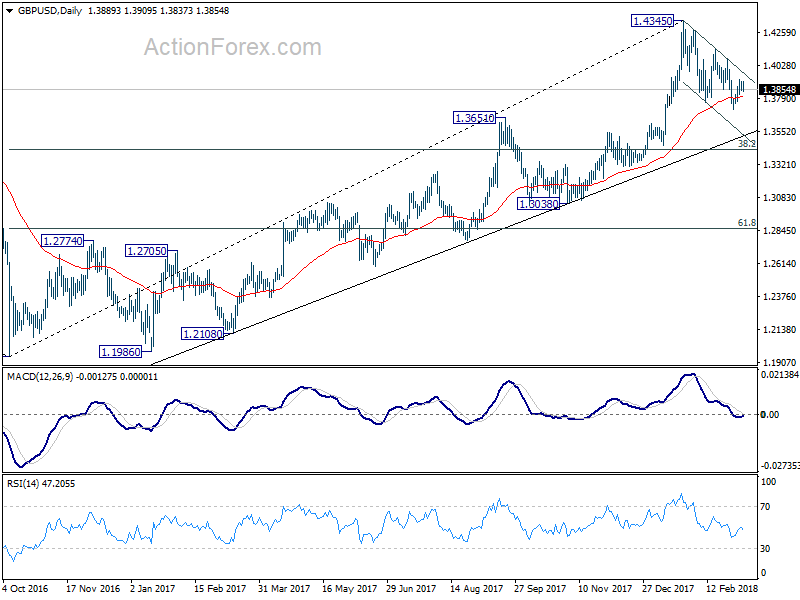

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3862; (P) 1.3887; (R1) 1.3928; More....

GBP/USD is struggling to stay above 4 hour 55 EMA but for the moment it's kept well above 1.3177 temporary low. Intraday bias remains neutral first. As noted before, decline from 1.4345 is in favor to extend with 1.4144 resistance intact. Below 1.3711 will resume the fall from 1.4345 through 1.3651 resistance turned support. We'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

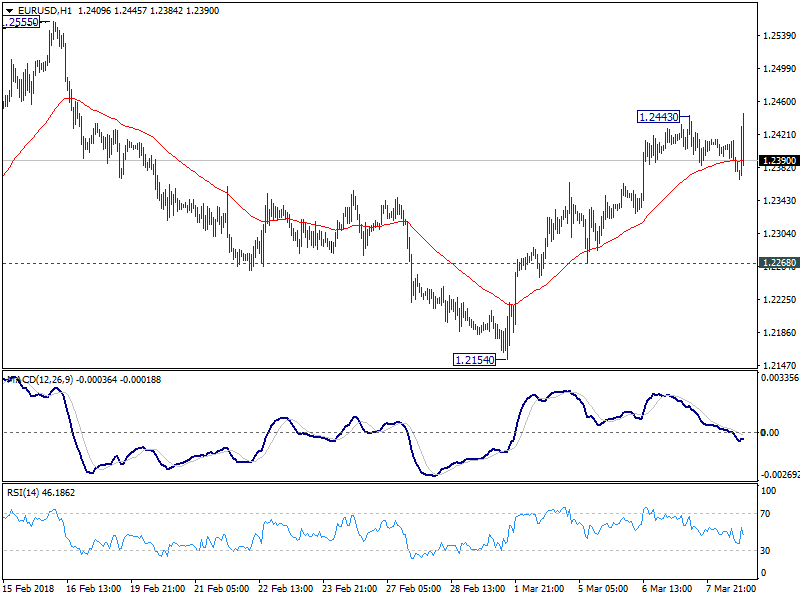

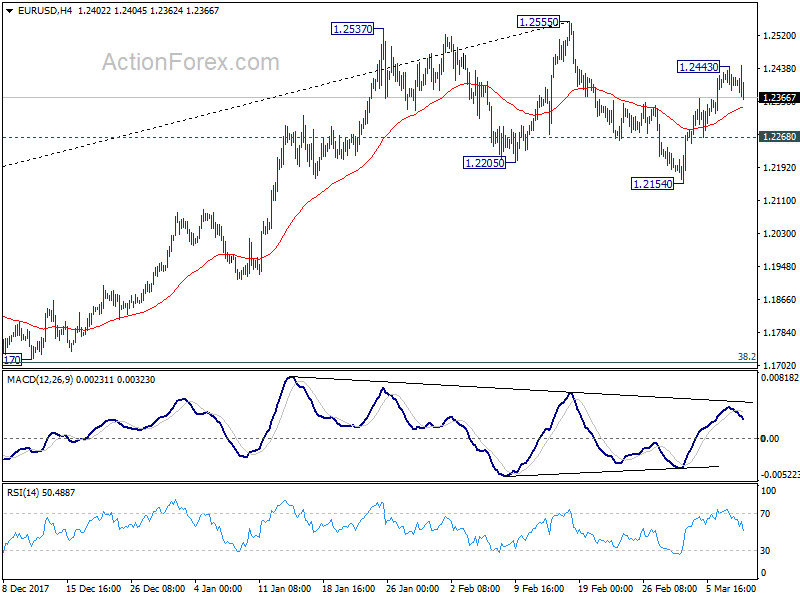

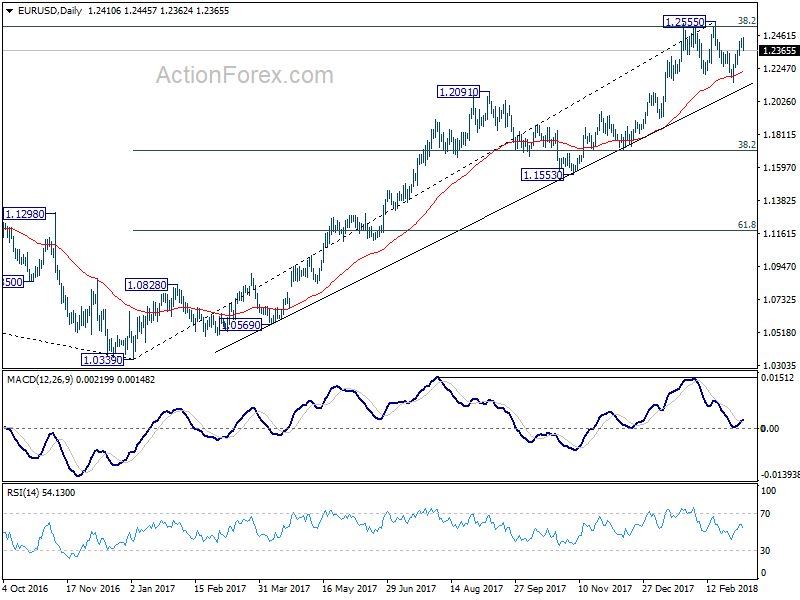

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

EUR/USD edges higher to 1.2445 but fails to sustain gain above 1.2443 temporary top. Intraday bias remains neutral first and some more consolidative could be seen. For now, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corr

ective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

ective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Euro Struggles to Gain as ECB Draghi Talks Down Even Tiny Step of Exit

Euro is initially short up as ECB turned a bit less dovish in the statement after keeping monetary policy unchanged. However, the common currency cannot extend gains as there is no follow through buying. More importantly, ECB President Mario Draghi tries to tone down the significance of the change in the post meeting pressing conference. For now, EUR/USD is still trading below 1.2443 minor resistance, EUR/GBP below 0.8967, EUR/JPY below 132.01. The only exception is EUR/CHF, which is marching on 1.17 today and is on course for 1.1821 key resistance.

Elsewhere, Canadian Dollar is trading as the strongest major currency today on relief that Canada will be exempted from US President Donald Trump's steel and aluminum tariff. Dollar trading seems to be relieved too as the greenback is following the Loonie as the second strongest for today. DOW opens the day higher and is up around 100 pts at the time of writing. It could be having a taken of the difficult 25000 handle again.

ECB takes tiny step in exit, but Draghi still talks it down

ECB left the main refinancing rate unchanged at 0.00% today as widely expected. The marginal lending facility rate and deposit facility rate are held at 0.25% and -0.40% respectively. The program to buy EUR 30b assets per month till September is also held unchanged. The most important part of the policy statement is that the option to "expand" the asset program is taken out. That is, the following texts are omitted from today's statement:

"If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration."

But later in the post meeting press conference, Draghi tried to tone down the change. . While the decision was unanimous, Draghi emphasized that it's just removing "explicit reference" to the chance of increasing the size of the APP again. However, firstly, ECB will keep interest rate at the current level for an extended period after the APP ends. And secondly ECB is still keeping the option to "extend" the APP beyond September.

ECB also released updated economic projections. There are little changes except that growth in 2018 is expected to be slightly faster at 2.4%. 2019 inflation projection is lowered by 0.1% to 1.4%.

GDP

- 2018 at 2.4% vs 2.3% prior

- 2019 at 1.9% vs 1.9% prior

- 2020 at 1.7% vs 1.7% prior

Inflation

- 2018 at 1.4% vs 1.4%

- 2019 at 1.4% vs 1.5%

- 2020 at 1.7% vs 1.7%

Released earlier in European session, German factory orders dropped -3.8% mom in January. Swiss unemployment rate was unchanged at 2.9% in February.

Trump's tweet in-line with expectation of exemptions of Canada and Mexico in tariff

Trump will be formally signing the order on 25% steel and 10% aluminum tariff today. Trump tweeted this morning that "looking forward to 3:30 P.M. meeting today at the White House. We have to protect & build our Steel and Aluminum Industries while at the same time showing great flexibility and cooperation toward those that are real friends and treat us fairly on both trade and the military."

The message is so far in line with market expectations that Canada and Mexico will be given temporary exemption on the tariffs while NAFTA negotiation is carrying on.

Released from US, initial jobless claims rose 21k to 231k in the weekended Mar 3. Prior week's 210k was the lowest since 1969. Four week moving average rose 2k to 222.5k. Continuing claims dropped 65k to 1.87m in the week ended February 24.

From Canada, housing starts rose to 229.7k in February, above expectation of 220k. New Housing price index rose 0.0% mom in January versus expectation of 0.1% mom. Building permits rose 5.6% mom in January versus expectation of 1.3% mom.

Australia recorded massive AUD 1.06b trade surplus in January

Australia recorded massive trade surplus of AUD 1.06b in January, a turnaround from December's AUD -1.15b trade deficit. Exports jumped 4% mom to AUD 33.9b, with 4% rise in non-rural goods, 54% rise in non-monetary gold. Much more than offsetting -8% fall in rural goods. Imports, on the other hand, dropped -2% to AUD 32.9b. Consumption goods dropped -7%, non-monetary gold dropped -19%, capital goods dropped 1%.

China pledges "justified and necessary response" to trade wars"

China Foreign Minister Wang Yi pledged to have "justified and necessary response" to trade wars. He said that "A trade war has never been the right way to solve the problem, especially under globalization." And, these conflicts "will only harm everyone and China will surely make a justified and necessary response."

At the same time China's trade surplus widened to USD 33.7b in January, or CNY 225b. Both were way better than expectation of USD -8.5b or CNY -71b deficit. Exports rose 44.5% yoy. Imports rose 6.3% yoy.

From Japan, Q4 GDP was finalized at 0.4% qoq, revised up from 0.1% qoq. GDP deflator was revised up to 0.1% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

EUR/USD edges higher to 1.2445 but fails to sustain gain above 1.2443 temporary top. Intraday bias remains neutral first and some more consolidative could be seen. For now, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q4 | 2.80% | 0.50% | ||

| 23:50 | JPY | Current Account (JPY) Jan | 2.02T | 1.76T | 1.48T | 1.68T |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 0.10% | 0.00% | 0.00% | |

| 00:01 | GBP | RICS House Price Balance Feb | 0% | 7% | 8% | |

| 00:30 | AUD | Trade Balance Jan | 1.06B | 0.22B | -1.36B | -1.15B |

| 02:00 | CNY | Trade Balance (USD) Feb | 33.7B | -8.5B | 20.3B | |

| 02:00 | CNY | Trade Balance (CNY) Feb | 225B | -71B | 136B | |

| 06:45 | CHF | Unemployment Rate Feb | 2.90% | 2.90% | 3.00% | |

| 07:00 | EUR | German Factory Orders M/M Jan | -3.90% | -1.60% | 3.80% | 3.00% |

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -4.30% | -2.80% | ||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:15 | CAD | Housing Starts Feb | 229.7K | 220K | 216K | 215.3K |

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.00% | 0.10% | 0.00% | |

| 13:30 | CAD | Building Permits M/M Jan | 5.60% | 1.30% | 4.80% | 2.50% |

| 13:30 | USD | Initial Jobless Claims (MAR 3) | 231K | 216K | 210K | |

| 15:30 | USD | Natural Gas Storage | -58B | -78B |

Euro staying in range as Draghi tones down language change

Euro fails to extend gain as Draghi tried to tone down the change in language. While the decision was unanimous, Draghi emphasized that it's just removing "explicit reference" to the chance of increasing the size of the APP again. However, firstly, ECB will keep interest rate at the current level for an extended period after the APP ends. And ECB is still keeping the option to "extend" the APP beyond September.

Here are the updated economic projections:

GDP

- 2018 at 2.4% vs 2.3% prior

- 2019 at 1.9% vs 1.9% prior

- 2020 at 1.7% vs 1.7% prior

Inflation

- 2018 at 1.4% vs 1.4%

- 2019 at 1.4% vs 1.5%

- 2020 at 1.7% vs 1.7%

EUR/USD fails 1.2443 so far. Draghi’s press conference script.

EUR/USD tries to break 1.2443 as ECB turned less dovish in the statement. But no follow through buying seen yet.