Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

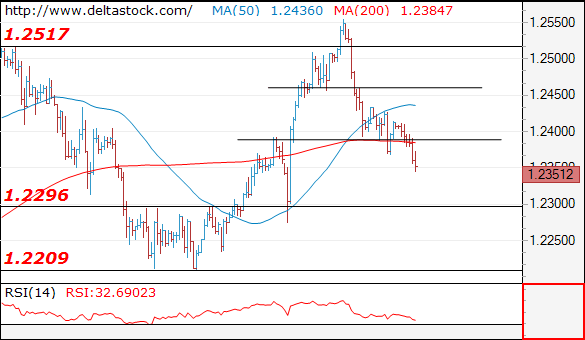

EUR/USD

Current level - 1.2351

The bias is still negative, with a risk of a slide towards 1.2290 support area. A rebound above 1.2410 will signal a reversal for another rise towards 1.2550.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2410 | 1.2650 | 1.2290 | 1.2290 |

| 1.2460 | 1.2870 | 1.2290 | 1.2210 |

USD/JPY

Current level - 107.18

The outlook is positive above 107.80, for a rise towards 108.00 resistance area. Crucial on the downside is 106.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.50 | 108.30 | 106.80 | 105.40 |

| 108.30 | 110.40 | 106.40 | 102.40 |

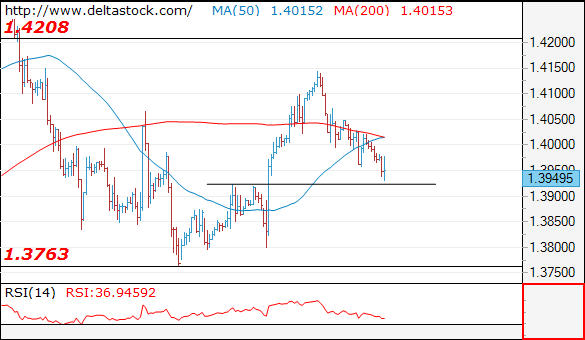

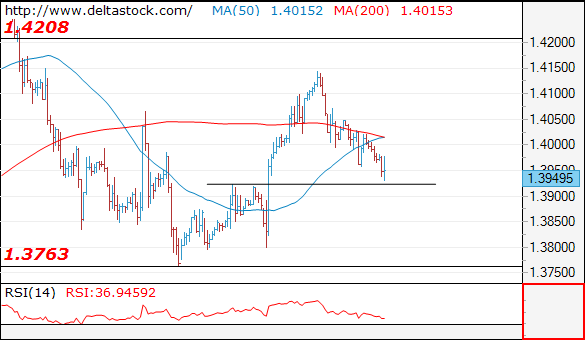

GBP/USD

Current level - 1.3949

The slide has reached 1.3920 support and my outlook is already bullish, for a rise towards 1.4280 are. Trigger on the upside is 1.4060.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4060 | 1.4280 | 1.3920 | 1.3760 |

| 1.4185 | 1.4340 | 1.3800 | 1.3620 |

Market Update – European Session: German ZEW Survey Moves Off From Record Highs, EU Said To Offer Flexibility To...

Notes/Observations

Eurogroup nomination of Spain’s de Guindos as the next ECB Vice-Chair allows the potential successor to Draghi to come from a core northern European country

EU said to be more willing to call for more flexibility in future relationship talks with Britain

Asia:

RBA Feb Minutes reiterates that low interest rates was helping reduce unemployment and help raise inflation further. Further progress on inflation likely to be only gradual and saw underlying inflation rising to 2.25% by mid-2020. Reiterated view that rising AUD currency would impede pickup in economic growth and inflation

Japan Fin Min Aso: Expect BOJ to keep working with govt to beat deflation; reaching 2% inflation is a way to prove Japan has beat deflation

Europe:

Eurogroup formally nominated Spain's Luis de Guindos for ECB vice president role (as expected)

Spain Econ Min de Guindos stated that he would resign as Econ Min within days after being chosen as ECB VP. Reiterated view that steps need to be taken to deepen economic and monetary union and vowed to defend ECB independence

Eurogroup chief Centeno: Greece has only 2 prior actions outstanding before disbursement of new loans; technical work on debt relief measures for Greece has already start (in-line with recent press reports)

PM May said to have a contingency plan to withhold payments of the £40B Brexit bill if EU leaders backtrack on their post-Brexit free trade deal. Fall-back option that could be triggered if negotiations go wrong

UK Brexit Min Davis upcoming speech to reassure the European Union that the U.K. won’t try to undercut the bloc by tearing up regulations after the split, making the case for mutual trust between regulators on each side

ECB has purchased €1.924T worth of bonds in public sector purchase program (PSPP, QE) as of w/e Feb 16th v €1.919T prior week

Energy:

OPEC Sec Gen Barkindo: Jan compliance seen at 133% for OPEC/Non-Opec members on production cut agreement. Rebalancing of market gaining massive momentum

Economic Data:

(JP) Japan Jan Final Machine Tool Orders Y/Y: 48.8% v 48.8% prelim

(DE) Germany Jan PPI M/M: 0.5% v 0.3%e; Y/Y: 2.1% v 1.8%e

(CH) Swiss Jan Trade Balance (CHF): 1.3B v 3.4B prior, Exports Real M/M: -5.1 v +3.3% prior; Imports Real M/M: 3.8% v 1.0% prior

(FI) Finland Jan Unemployment Rate: 8.8 v 8.4% prior

(ZA) South Africa Dec Leading Indicator: 104.6 v 105.2 prior

(DK) Denmark Feb Consumer Confidence Indicator: 8.5 v 8.0e

(TR) Turkey Feb Consumer Confidence: 72.3 v 72.3 prior

(JP) Japan Jan Convenience Store Sales Y/Y: +0.1 v -0.3% prior

(HU) Hungary Dec Average Gross Wages Y/Y: 13.5% v 14.2%e

(SE) Sweden Jan CPI M/M: -0.8% v -0.7%e; Y/Y: 1.6% v 1.8%e

(SE) Sweden Jan CPIF M/M: -0.9% v -0.7%e; Y/Y: 1.7% v 1.9%e, CPI Level: 322.51 v 322.92e

(ES) Spain Dec Trade Balance: -€2.1B v -€1.6B prior

(PL) Poland Jan Sold Industrial Output M/M: 4.1% v 3.7%e; Y/Y: 8.6% v 8.5%e, Construction Output Y/Y: 34.7% v 20.4%e

(PL) Poland Jan PPI M/M: 0.1% v 0.1%e ; Y/Y: 0.2% v 0.1%e

(PL) Poland Jan Retail Sales M/M: -20.5% v -21.2%e; Y/Y: 8.2% v 6.9%e, Real Retail Sales Y/Y: 7.7% v 6.5%e

(GR) Greece Dec Current Account Balance: -€1.2B v -€1.0B prior

(DE) German Feb ZEW Current Situation Survey: 92.3 v 93.9e; Expectations Survey: 17.8 v 16.0e

(EU) Euro Zone Feb ZEW Expectations Surveys: 29.3 v 29.0 prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) opens book to sell Oct 2048 bonds; guidance seen +107bps to mid-swaps with order book over €22.5B

(ID) Indonesia sold total IDR8.475 in 6-month Islamic Bills; 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2030, 2037, 2041 and 2048 bonds

(ES) Spain Debt Agency (Tesoro) sold total €1.31B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 378.3, FTSE -0.5% at 7213, DAX -0.1% at 12373, CAC-40 flat at 5257 , IBEX-35 +0.2% at 9829, FTSE MIB +0.1% at 22582 , SMI flat at 8907, S&P 500 Futures -0.8%]

Market Focal Points/Key Themes: European Indices trade mostly higher across the board following the weakness seen yesterday, with the FTSE under performing being weighed on by HSBC and BHP Billiton following results. Also weighing on the FTSE is shares of IHG trading over 4% lower after announces results and a cost cutting plans. Elsewhere, HeidelbergCement, Covestro trade higher in Germnay following results, with Edenred also rising. In the M&A space Fidessa trades sharply higher after confirming an approach by Temenos. Looking ahead notable earners include Home Depot, Duke Energy, Genuine Parts and MGM Resorts.

Movers

Consumer Discretionary [ Edenred [EDEN.FR] +7.4% (Earnings), Sports Direct [SPD.UK] +3% (Share buyback), IHG [IHG.UK] -4.6% (Earning), Dunelm [DNLM.UK] -10% (Earnings)]

Materials [ BHP [BLT.UK] -3.3% (Earnings) ]

Industrials [HeidelbergCement [HEI.DE] +1.8% (Earnings)]

Healthcare [ Covestro [1COV.DE] +1.8% (Earnings)]

Financial [ HSBC [HSBA.UK] -4.2% (Earnings), Fidessa [FDSA.UK] +23% (Confirms takeover approach)]

Speakers

European Parliament said to be preparing a "detailed," 60-paragraph resolution which will call for more flexibility in future relationship talks with Britain. European Parliament said to call for Britain to have 'privileged' single market access after Brexit

ECB's Rimsevics (Latvia): All allegations against me wee false; never asked for or receive a bribe

EU's Moscovici: stated that had questions on US policy and WTO rules. Tax dumping was not the right answer to US tax reform

Germany Fin Min Altmaier: EU to keep a close watch on US tax reform

Sweden Fin Min Andersson stated that Sweden to vote no to EU budget discharge; hoped for further improvements. Positions on bank union risk sharing was locked; discussion on how to measure risks included govt bonds

Luxembourg Fin Min Gramegna: stated that EU should be united on tax reform. UK would be a reliable partner after Brexit

German CDU Parliamentary Whip Grosse-Broemer: Markel could be voted in 2nd week of March with SPD vote

ZEW Economists: Inflation expectations for both Germany and the Euro Zone had increased; Domestic economy expected to improve in coming months -

Japan PM Abe: Must consider steps on demand swings from sales-tax hike (**Note: The 1st phase was in Apr 2014 and the 2nd phase is planned for Oct 2019

OPEC Committee said to see pace of oil rebalancing quickening

UAE Energy Min Mazrouei: Oil market monitoring beyond 2018 was minimum we could do. OPEC had draft charter for future cooperation with allies (OPEC and non-OPEC members). Hoped OPEC and allies framework cooperation to be presented to all members in June

Currencies

The USD recovered from recent 3-year lows by having its best run in two months over the past few sessions as participants scaled back dollar shorts. One analyst believed that the USD correction should remain limited and was mainly driven by technical factors

EUR/USD was off 0.4% to test the 1.2350 area. The pair seemed to ignore the outcome of the ECB VP position to Spain’s de Guindos which now placed Bundesbank President Weidmann as one of the leading contenders to succeed Draghi in 2019

The GBP/USD pair recovered from initial losses as reports circulated that EU Parliament was preparing a "detailed," 60-paragraph resolution which would call for more flexibility in future relationship talks with Britain. Pair back testing the 1.40 area after testing 1.3930 earlier

Higher US yields helped the USD/JPY pair to move back above the 107 level.

Fixed Income

Bund Futures trades down 17 ticks at 158.12 after the German ZEW survey declines. Upside targets 158.85, while a continued move lower targets the157.25 level.

Gilt futures trade at 120.89 down 17 ticks as the Gilt spread over Bunds near a 2-month high sets to narrow. Support continues to stand at 120.75 then 120.15, with upside resistance at 121.75 then 122.25.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.854T from €1.863T prior. Use of the marginal lending facility rose to €47M from €98M prior.

Corporate issuance saw the primary market finish last week with ~$9B sold.

Looking Ahead

(DE) German SPD party begins membership ballot on coalition pact with CDU/CSU

(UK) House of Commons reconvenes after February Recess

(IL) Israel Feb CPI 12-Month Forecast: No est v 0.7% prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (EU) ECB allotment in 7-day Main Financing Tender

05:30 (DE) Germany to sell €5.0B in new Mar 2020 Schatz

06:00 (UK) Feb CBI Industrial Trends Total Orders: 11e v 14 prior, Selling Prices: No est v 40 prior

06:00 (IL) Israel Dec Manufacturing Production M/M: No est v % prior

06:00 (TR) Turkey to sell 2024 Floating Bonds; Yield: % v 6.18% prior

06:30 (EU) ESM to sell €2.0B in 6-month bills

06:30 (CL) Chile Central Bank Traders Survey

06:30 (SE) Sweden Central Bank ( Riksbank) Gov Ingves/Floden speech in New York

06:45 (US)Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Dec Wholesale Trade Sales M/M: 0.4%e v 0.7% prior

09:00 (NZ) Fonterra Global Dairy Trade Auction

09:00 (EU) Weekly ECB Forex Reserves

10:00 (EU) Euro Zone Feb Advance Consumer Confidence: 1.0e v 1.3 prior

10:30 (CA) Canada to sell 3-month, 6-month and 12-month BTF Bills

11:30 (US) Treasury to sell 4-Week Bills

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

13:00 (US) Treasury to sell 2-Year Notes

(IT) Italy Debt Agency (Tesoro) announcement for BTPei and CTZ auctions for Feb 23rd

15:00 (MX) Mexico Citibanamex Survey of Economists

16:00 (KR) South Korea Jan PPI Y/Y: No est v 2.3% prior

Technical Outlook: Cable Returns Above 1.40 On Media Report Regarding Brexit

Sterling bounced back above 1.40 barrier on media report saying that the EU parliament was preparing to call for giving Britain privileged single market access. The rally sidelined immediate downside risk after fresh bears probed below converged 10/30SMA's (1.3945) earlier today, however, the downside is expected to remain vulnerable while the price holds below 20SMA (1.4033).

Res: 1.4015, 1.4033, 1.4054, 1.4104

Sup: 1.3954, 1.3931, 1.3900, 1.3854

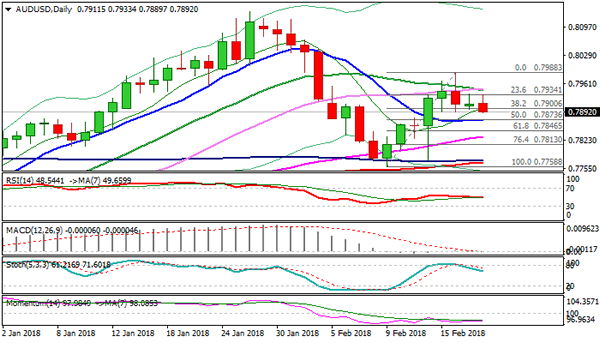

Technical Outlook: AUDUSD – Stronger Direction Signals On Break Below 10SMA (0.7871) Or Above 0.80 Zone

The Australian dollar stands at the back foot on Tuesday and probes below 0.79 handle, signaling extension of pullback from Friday's high and strong upside rejection at 0.7988, where recovery rally stalled just ahead of 0.7991 Fibo barrier (Fibo 61.8% of 0.8135/0.7758 pullback).

Mixed setup of daily MA's, neutral RSI/MACD and negative momentum show no clear near-term direction, with stronger bearish signals expected on violation of 10SMA (0.7871), or bullish on firm break above 0.7991 Fibo barrier.

Negative scenario would look for extension towards 0.7846 (Fibo 61.8% of 0.7758/0.7988 upleg) and 0.7832 (rising 55SMA) which would expose key supports at 0.7773/68 (converged 100/200SMA's) and 0.7758 (09 Feb correction low).

Bullish scenario requires sustained break above 0.80 zone to open way for further recovery towards 0.8046 (Fibo 76.4% of 0.8135/0.7758 downleg) and 0.8100 (round-figure barrier).

Res: 0.7935, 0.7947, 0.7988, 0.8046

Sup: 0.7873, 0.7846, 0.7832, 0.7800

USD/JPY: Japan’s Trade Balance

The Japan's Yen rose against the Greenback, following the report on the country's trade balance on Sunday. The USD/JPY exchange rate gained 13 base points or 0.12% to 106.27.

The Japan's exports grew ¥0.37T in January, surpassing forecasted ¥0.14T and showing 14th month of growth in a row. Meanwhile, the country's Ministry of Finance showed that a surge in imports put trade deficit in the red for the first time since May. However, higher imports indicating an improvement in domestic demand confirmed that the BoJ moved forward in efforts to set up a self-sustaining recovery of the Japan economy. Experts warned that the strengthening Yen is a risk, as it is likely to make imports cheaper, putting pressure on inflation.

EUR/USD: EZ Current Account

The Euro zone's currency advanced against the US Dollar on Monday on continuously growing surplus trend in the Eurozone's current account. EUR/USD showed strength and moved upwards 10 pips, or 0.08%, and continued rising with enough momentum to reach the 1.2417 level.

In December, the single currency bloc has recorded a €29.9B surplus, while economists expected to see it at €30.5B. Euro zone's current account surplus was 3.5% of the Euro area GDP over the past 12 months, compared with 3.4% a year earlier; however, this figure remained quite stable over the span of past two years. In its monthly release, the ECB also reported that November's unadjusted surplus has increased from €40.1B to €45.8B.

GBP/CHF 4H Chart: Trading Sideways

During the past few weeks, the British Pound has been depreciating heavily against the Swiss Franc. The depreciation occurred after the pair hit the weekly R1 at 1.3439.

The Pound Sterling has stopped its decline and has been in a period of consolidation. As can be observed on the chart, the currency pair has been trading inside a rectangle since February 9.

A breakout from the rectangle is expected to occur to either direction in the nearest time. In the meantime, technical indicators suggest that bears could grow stronger.

USD/CHF 4H Chart: Poised For A Breakout

The US Dollar has been constrained by a descending channel against the Swiss Franc after hitting a resistance at the 200—hour simple moving average on January 10.

The currency pair has been bouncing between the upper and lower boundaries of the junior channel. However, there could be a breakout through the upper boundary during the next trading days.

If the USD/CHF pair moves past a resistance cluster set by the combination of the 55- and 100– hour SMAs, the rate could be heading for the weekly R1 at 0.9397.

Technical Outlook: USDJPY – Extended Recovery To Be Ideally Capped By Daily Tenkan-Sen / 10SMA

The dollar extends recovery from 105.54 (last Friday's spike low) and probes above 107 handle in early Tuesday's trading.

Daily RSI and slow stochastic are heading north after reversing from oversold territory and signaling further recovery, however overall picture is bearish and sees current action as corrective and positioning for fresh shorts.

Recovery eyes initial resistances at 107.31/43 (former low of 08 Sep / Fibo 38.2% of 110.48/105.54 bear-leg) ahead of 107.65 barrier (falling 10SMA / daily Tenkan-sen) which is expected to ideally cap.

Stronger correction could be expected on firm break above 107.65 which could spark further recovery towards 108.44/51 (20SMA / daily Kijun-sen).

The greenback is in recovery mode after suffering losses in past two weeks, as a part of broader weakness and will be looking from fresh signals.

A number of Fed speakers are scheduled this week, along with release of minutes of FOMC latest meeting, which could give fresh signals for the dollar.

Res: 107.31, 107.43, 107.65, 108.00

Sup: 106.55, 106.20, 106.09, 105.54

EUR/USD Analysis: Fluctuates Around 1.24

As already expected, the common European currency remained stable against the US Dollar which was caused by lack of fundamental events that could introduce volatility in the market. Thus, the pair remained fluctuating around the weekly PP at 1.24 within the last 24 hours.

Even though the Euro was pushed slighty lower during the Asian session early on Tuesday, the market is expected to be guided by bulls, especially if the combined support of the 200-hour SMA and the 23.60% Fibo retracement is limiting the pair near the 1.2350 mark. Technical indicators are likewise supportive of the bullish scenario that should move the rate towards the 55– and 100-hour SMAs near 1.2450.

Given that no significant fundamentals are likewise apparent today, this resistance should not be breached.