Sample Category Title

UK’s Retail Sales Plunged In September

For the 24 hours to 23:00 GMT, the GBP declined 0.41% against the USD and closed at 1.3155, following weaker-than-expected UK retail sales figures.

Data showed that Britain's retail sales declined more-than-expected by 0.7% on a monthly basis in September, suggesting that accelerating inflation is squeezing household incomes and holding back the growth of retail sector. Retail sales had registered a revised advance of 0.9% in the prior month, while investors had envisaged for a drop of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.3101, with the GBP trading 0.41% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3060, and a fall through could take it to the next support level of 1.3019. The pair is expected to find its first resistance at 1.3182, and a rise through could take it to the next resistance level of 1.3263.

Moving ahead, traders would direct their attention to the UK's public sector net borrowing data for September, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.42% against the JPY and closed at 112.56.

On the data front, Japan’s final machine tool orders climbed 45.0% YoY in September, and revised lower from a preliminary print indicating a gain of 45.3%. Machine tool orders had risen 36.2% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 113.21, with the USD trading 0.58% higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.57, and a fall through could take it to the next support level of 111.93. The pair is expected to find its first resistance at 113.58, and a rise through could take it to the next resistance level of 113.95.

Looking ahead, a speech by the BoJ Governor, Haruhiko Kuroda, due in a few hours, will be eyed by traders. Also, market participants will closely monitor Japanese general election, due over the weekend, wherein the Japanese Prime Minister, Shinzo Abe’s ruling party is expected to secure a majority.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s Trade Surplus Rose In September

For the 24 hours to 23:00 GMT, the USD declined 0.51% against the CHF and closed at 0.9762.

In economic news, Switzerland's trade surplus widened to CHF2.9 billion in September, after recording a revised surplus of CHF2.2 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9822, with the USD trading 0.61% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9757, and a fall through could take it to the next support level of 0.9691. The pair is expected to find its first resistance at 0.9868, and a rise through could take it to the next resistance level of 0.9913.

Going ahead, Switzerland's ZEW expectations index and the UBS consumption indicator, due to release next week, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading Lower, Ahead Of Canada’s Inflation And Retail Sales Data

.

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CAD and closed at 1.2485.

In the Asian session, at GMT0300, the pair is trading at 1.2518, with the USD trading 0.26% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2473, and a fall through could take it to the next support level of 1.2428. The pair is expected to find its first resistance at 1.2541, and a rise through could take it to the next resistance level of 1.2564.

This afternoon will bring two crucial Canadian releases, namely the consumer price index for September and retail sales figures for August.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

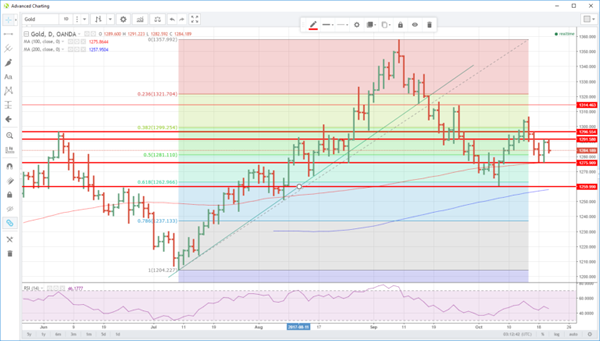

Gold Tumbles In Asia As U.S. Senate Rallies The Dollar

Gold tumbles as the U.S. Senate causes yields and the dollar to rise across the board.

Gold has fallen 0.50% or some six dollars from its close in New York as Asia erases almost all of the gains it made yesterday. Gold is wilting as the U.S. dollar surges in Asia after the U.S. Senate adopted an FY18 budget resolution. It has seen Treasury yields edge higher pushing the dollar up across most currencies with the US Dollar Index higher by 0.40% in Asia. Along with the odds of the new Federal Reserve Chairmen shortening to make a more hawkish Jerome Powell the frontrunner, none of this is good news for gold.

Having closed at 1289.00 gold is now trading at 1283.50 with double top resistance at 1291.30 followed by the 1296.00 area. Significant support, however, is just below at 1276.00, a double bottom from Wednesday and Thursday and also the 100-day moving average. A break would open up further falls to the 1260.00 regions and the nearby 200-day moving average at 1258.00. It would most likely a significant rush for the exit door by traders if it were to give way.

The key to the remainder of the session is whether the U.S. dollar gains and higher Treasury yields are sustained into Europe and New York. If the moves correct then gold may get a reprieve, if Europe continues to run with this baton, it could be a long day for bullish gold traders.

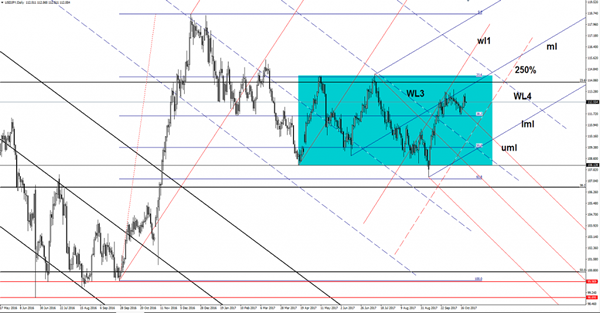

USD/JPY Upside Paused

USD/JPY increased little in the first hour and is fighting hard to stay higher and to recover after the yesterday’s drop. Price decreased and failed to reach and retest the median line (ml) of the blue ascending pitchfork, signaling an exhaustion. The Yen increased as the Nikkei stock index dropped after the impressive rally. USD/JPY is trading right above the 112.50 level and could move in range on the short term before will recapture more directional energy to be able to climb much higher.

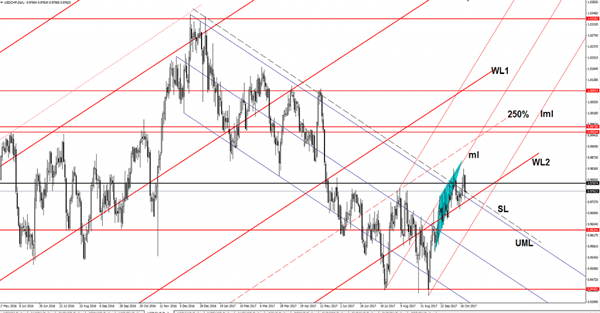

USD/CHF Valid Or False Breakout?

The rate plunged and dropped much below the sliding parallel line (SL) of the descending pitchfork, but failed to stay there and has squeezed a little. Price continues to pressure the sliding line (SL), maybe will be better to stay away from this pair right now because we don’t have any trading opportunity. A buying opportunity could appear if the rate will retest the confluence area formed between the WL2 with the SL.

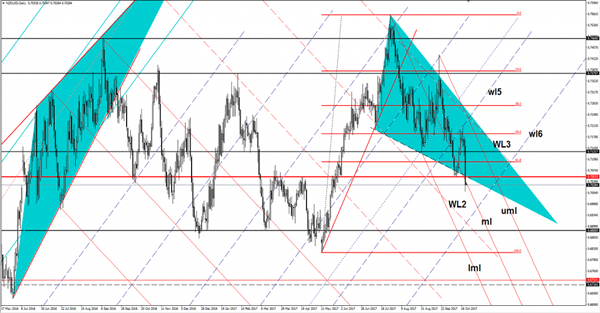

NZD/USD Erases Everything

The NZD/USD plunged aggressively in the yesterday's trading session and erased the last week's gains. Price ignored several downside obstacles and closed much below the 0.7055 previous low. However, remains to see if this is a valid breakdown, or the rate will come back higher. Technically, it could come to retest the broken levels before will resume the downside movement.

Is on a declining path and could reach fresh new lows in the upcoming weeks, this scenario will take shape only if the USDX will have enough energy to climb higher again.

The NZD/USD dropped somehow surprisingly as the USDX has dropped significantly on Thursday. The dollar index moves in range on the short term and still maintains a bullish bias despite the last day's drop. I've said in the previous days that the USDX could decrease a little again because I don't believe that will have enough directional energy to take out the 93.81 static resistance.

Price dropped like a rock and now stands below the 0.7055 previous low and below the median line (ml) of the minor descending pitchfork. A valid breakdown below the median line (ml) signals a further drop in the upcoming period, but a fakeout will drive the rate towards the 0.7055 level again. I've said in the last days that technically it should come down to retest the median line (ml) after the retest of the wl5 and after the failure near this level and above the 50% Fibonacci level.

We Won’t Back Down

We Won't Back Down

The Dow managed to scrimp out a new record high as investors vote for higher earnings over superstition while nudged along by Fed speculation.

It's been a testy 24 hours for investors as global market toppled on a cascade of risk aversion flashpoints and despite a potpourri of explanations floating around, PBoC Governor Zhou's warning against “excessive optimism” seems the most likely trigger.

The Hang Seng led the global route falling more than 2 % at one point closing down -1.9 % However suspected intervention to prevent any awkwardness during the Party Congress saw Mainlands SHCOMP only down .34%

But Risk aversion accelerated as the Spain/Catalonia conflict came oh so close to crossing the Rubicon or should I say Ebro. Spanish Newswires were ablaze with headlines that Article 155 is now extremely likely to be triggered. Predictably, that sent a wave of panic across all asset classes. Oil prices fell off the cliff, Euro wobbled, USDJPY dropped like a stone, and US yields took a hit.

The veracity of the moves was a bit peculiar, but the expanse of the movement is a graphic reminder just how thin traders are positioning these days given the uncertainties surrounding US politics, the Fed Chair race, Spain, Brexit and China's Congress.

As for today, we should expect another session of headline risk via the protraction of current market narratives.

Politico reports: “Federal Reserve Governor Jerome Powell is the leading candidate to become the chair of the US central bank after President Donald Trump concluded a series of meetings with five finalists Thursday, three administration officials said” .I think what we can glean from this release is its either Powell or Taylor.

The headline saw the USDJPY drop to 112.41 ( -25 pips)in thinly traded markets, but if anything this move could foreshadow the market lean on a Powell nomination as he is perceived less hawkish than co front-runner Taylor.

The New Zealand Dollar

Investors were spooked by a potential shift in RBNZ policy. Both Labour and NZ First are looking to revamp the Central Bank by appointing outside director while moving away from the single decision-maker model. While the markets were shellshocked, but in a world of political upheaval, perhaps it best to expect the unexpected. However, the profundity of this political swing is no small matter as the coalition could bring about a dual mandate for the RBNZ incorporating a full employment target alongside the traditional inflation target an likely currency consequences. So far there has been little appetite to buy the dip while traders remain in ” sellindipity” mode expecting an extension of the current trend

The Japanese Yen

Appears to be a short-term shake out with risk aversion ratcheting higher and likely accelerated by a sharp drop in oil prices. Short term traders were caught long on the USDJPY momentum trade heading into Sunday's election. Longer term positioning came under little threat so far, and the market remains tentatively bid on dips

The long dollar trade looked so much clearer yesterday, but with EU risk simmering and Fed musical chair headlines still looming large, its difficult to envision a push higher on USDJPY into the weekend despite an expected strong showing from Abe on Sunday

The British Pound

The Pound got pounded after UK retail sales hit a four year low. And to rub salt in the wounds, the August figures were all revised lower too. It has been an intense week for Sterling traders who will be happy to hear the closing bell as politics continue to make things messy. Brexit remains the primary focus, but the political confusion makes for an awful market to trade.

The Euro

Have we seen the worst of the Catalan fallout? Probably not as currency headwinds are likely to remain high to gusty. However, as we've seen so often when EU political risk looks to be nearing the point of no return, it has an uncanny way of working out favourably for the market. As cooler heads prevailed the market reaction overnight was widely considered way overdone and a modicum of risk appeal has filtered back into the EU markets.

Politics And Powell

We were once again reminded that this is the era of political-driven trading after a surprise coalition formed in New Zealand. The euro and Swiss franc led the way while the kiwi lagged badly. On the Fed, the latest report is that Trump is leaning towards Powell. The long EURUSD Premium trade was closed for 110 pips, while the other EUR trade remains in progress, currently 110 pips in the green.

The anniversary of Black Monday had a fitting end for 2017 with the S&P 500 finishing higher after earlier worries were wiped away. The early tone was risk aversion on China concerns and a 2% fall in Hong Kong stocks.

NZDUSD had its bigggest 1-day drop in over 2 years after the Labour Party was able to throw together a coalition with the help of the Greens and First Party. That means Bill English will and his National Party – which got 44.4% of the vote – will be in opposition. The kiwi fell more than 150 pips on the surprise turn. More broadly, it's a reminder of the discontent in the air and the sudden willingness almost everywhere to try new things.

We contrast that with China where Communist Party leadership and Xi in particular are strengthening their leadership. In the long-term, it's a signal about the rise of China and emerging markets and the frustration in the developed world.

Meanwhile in the US, hopes for many voters for a radical change in monetary policy may be dashed. A Politico report said Fed Governor Jerome Powell is the favourite to replace Yellen. He's done little to publicly separate himself in more than 5 years at the Fed with most of his focus on regulation. The thinking is that he will be a continuation of the Bernanke-Yellen era, sticking with the same policies and prescriptions. The stock market responded with a small flurry at the end of the day and the US dollar dipped.

Looking ahead, news from the Party Congress is likely to be the main driver but Kuroda also speaks at 0635 GMT and later in North American trade, Canadian retail sales and CPI numbers are due.