Sample Category Title

USD/CHF Elliott Wave Analysis

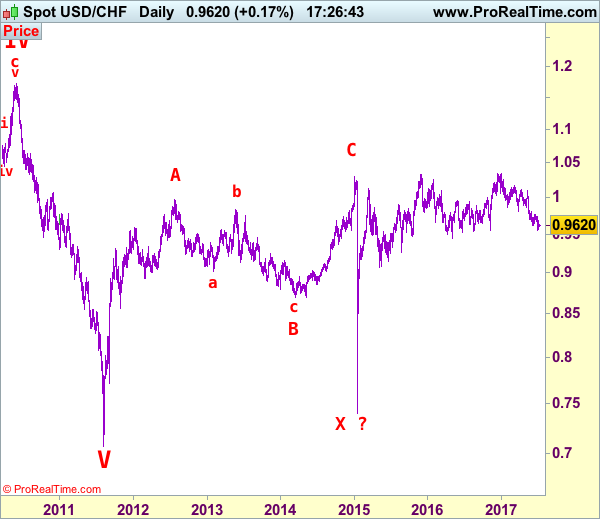

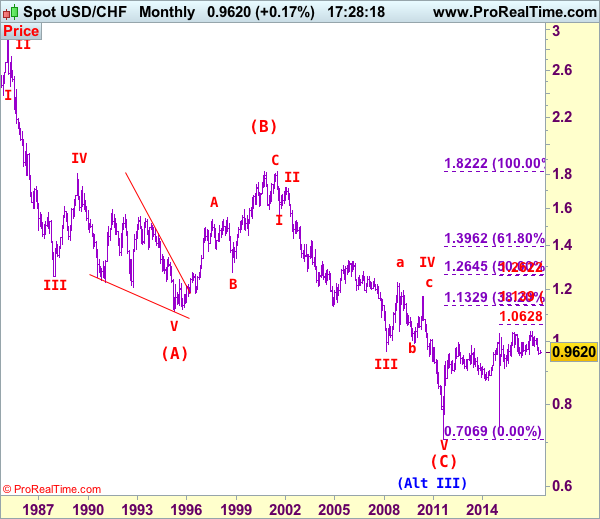

USD/CHF – 0.9619

USD/CHF – Wave IV ended at 1.1730 and wave V has possibly ended at 0.7068

The greenback found support at 0.9552 last week and has rebounded, suggesting minor consolidation above this level would be seen and above 0.9700 would bring recovery towards resistance at 0.9771, however, reckon resistance at 0.9808 would attract renewed buying interest and bring another decline later. Below said support at 0.9552 would signal the decline from 1.0344 top has resumed and may extend weakness to 0.9500 but loss of downward momentum should prevent sharp fall below previous support at 0.9444 (2016 low) and reckon 0.9390-00 would hold, bring rebound later.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the upside, above 0.9700 would bring a stronger recovery to 0.9771 but reckon upside would be limited to resistance at 0.9808, bring another decline later. A daily close above 0.9808 would suggest a temporary low has been formed, bring retracement of recent decline to 0.9850-60 and later towards 0.9900-10 but price should falter well below 1.0000 psychological level.

Recommendation: Stand aside for this week.

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

EUR/USD Analysis: Pushed Higher By Fundamentals

On Friday morning the common European currency traded above the 1.14 mark against the US Dollar. The reason for that was the fact that instead of bouncing off the upper trend line of the short term pattern the currency exchange rate broke through the trend line. From a technical perspective it was done by the support of the 55 and 200-hour SMAs together with the weekly PP near the 1.1350 mark. However, the pair continued to surge until midnight. Due to that reason the fundamentals need to be examined. At 11:30 GMT on Thursday the ECB meeting accounts were published. It is most likely that in the minds of the market participants the rhetoric of the ECB officials has caused the strengthening of the Euro. Due to that reason once can expect the pair to reach for the 1.15 mark soon.

Technical Outlook: USDJPY Rallies Above 113.50 Barrier Ahead Of US NFP Data

Fresh strength on Friday eventually broke above 113.50 resistance zone, signaling bullish continuation.

The pair was congested within narrow consolidation in past three days, signaling strong indecision on triple Doji candles.

Firmly bullish studies on daily chart support the price for attempts through 114.00 barrier towards targets at 114.36 (10 May peak) and 114.65 (Fibo 61.8% of 118.65/108.16 descend).

Rising 10SMA continues to track broader advance, offering strong support at 112.80.

US jobs data are eyed for further signals, with acceleration through 114.36/65 targets expected on upbeat results and return towards 112.00/111.80 supports on NFP miss scenario.

Res: 114.00, 114.36, 114.65, 115.00

Sup: 113.54, 113.10, 112.80, 112.65

ADP Releases Weaker Than Expected Employment Report For June

'As the labor market continues to tighten that will nudge wages up, which will in turn bolster inflation.' -Mark Zandi, Moody's Analytics

The US private sector created less than expected jobs last month, suggesting that job creation started to cool after strong gains registered earlier. The ADP National Employment Report released on Thursday showed companies added 158K new jobs to the economy in June, following the preceding month's downwardly revised figure of 230K and surpassing analysts' expectations for an 185K increase. The second-weakest report within this year indicated that businesses decided to put off expansion projects until the Trump administration's plans are realised. Moreover, experts suggested that companies would continue to face difficulties of finding skilled workers as the labour market is expected to tighten further. The report is closely followed by the Federal Reserve, which remained cautious about job creation and its impact on wage growth. Notwithstanding weak inflationary pressures, the Federal Reserve is likely to raise interest rates at least one more time in 2017 as promised. The ADP figures came out ahead of the NFP report, which is expected to show a gain of 175K new jobs, following May's increase of 138K.

Canadian Trade Balance Worsens Unexpectedly In May

'How Canada's trade picture is tracking into the second quarter will put yet more wind into the Bank of Canada's sails.' -Derek Holt, Scotiabank Economics.

Canada's trade deficit widened almost two times fueled by gains in aircraft imports. Statistics Canada reported that the country's trade gap came in at C$1.1B in May, up from the preceding month's downwardly revised deficit of C$0.6B. However, the reading missed market projections for a C$0.5B trade deficit for the month. The trade balance report showed that the total value of exports posted a 1.3% monthly increase to C$48.7, while imports rose 1.3% to C$49.8 in May. On a yearly basis, exports rose 10.2% amid higher demand for unwrought gold from the United Kingdom. Meanwhile, total exports jumped 17.8% for the year due to more shipments of aircrafts, motor vehicles and parts. Imports from the United States grew to a record high of C$32.7B, while shipments to the southern neighbour fell 0.3% to C$36.3B. The weak data is expected to disappoint the Bank of Canada and postpone monetary policy tightening. However, businesses expressed optimism over the outlook for Canadian trade, while surging demand is set to lead to higher investment and hiring.

All Eyes On US Employment Data

Today, all eyes will be on the US employment report for June. The forecast is for nonfarm payrolls to have risen by 179k, more than the 138k in May. The unemployment rate is expected to have remained unchanged at 4.3%, while average hourly earnings are expected to have accelerated in monthly terms.

Overall, this would be another employment report consistent with further tightening in the labor market, which will be pleasant news for FOMC policymakers. Despite agreeing on raising the Federal funds rate in June, they were split on the outlook for inflation, how it might affect the future pace of interest rates, and when they should start normalizing the Bank's enormous balance sheet, according to the minutes of the latest gathering. Market expectations remained unaffected after the minutes' lack of clarity with regards to the timing of the next rate increase.

Therefore, if the June jobs report is indeed as robust as expected, it could bring forth those expectations and thereby, support the dollar. Having said that though, we would stay mindful as to whether the outcome will have lasting effects as a few hours later, the Federal Reserve will release its semi-annual monetary policy report to Congress, which could also impact market pricing with regards to the next increase in borrowing costs. After the minutes from the latest Fed gathering failed to provide extra hints with regards the future path of monetary policy, investors may dig into this report looking for such hints.

XAU/USD has been trading in a short-term downtrend since the 6th of June. On the 3rd of July, the precious metal dipped below the longer-term upside support line taken from the low of the 27th of January, something that trigger steeper declines. Nevertheless, the metal's tumble was halted once again by the 1217 (S1) zone, where we believe it settled waiting for the NFPs today. If the US jobs report comes in encouraging, the bears may take in charge again and perhaps drive the battle below the 1217 (S1) line, initially aiming for 1210 (S2). Another break below 1210 (S2) is possible to open the way for the psychological zone of 1200 (S3).

BoJ bond buying brings the yen under selling interest

Overnight, the Bank of Japan stepped in to the bond market, in order to put a lid on JGB yields after the 10 yr. yield had risen to 0.105%. The Bank bought 500bn yen of 5 to 10 JGBs, more than the 450bn in its prior operation. This is a move consistent with its yield-curve control policy, according to which the Bank aims at keeping the 10yr. yield at around 0%. The result as far as the FX market is concerned was a weakening yen.

USD/JPY spiked up during the Asian morning, breaking above the resistance now turned into support of 113.45 (S1) and clearing the longer-term downside resistance line drawn from the peak of the 11th of January. In our view, the overnight rally signals the continuation of the short-term uptrend that has been in place since the 15th of June. A decisive break above the resistance level of 113.90 (R1) is possible to open the way for our next obstacle of 114.40 (R2), marked by the peak of the 10th of May.

As for the rest of today's events:

Global leaders gather In Hamburg, Germany, for the 12th G20 summit. The leaders of the world's top economies will discuss terror attacks, free trade, and climate change.

As for the economic indicators, in the UK we have industrial production data for May. Expectation are for the IP to have accelerated, something that could prove positive for the pound.

At the same time we get the US employment report, we have jobs data from Canada as well. The forecast is for the unemployment rate to have held steady and for the net change in employment to have remained in positive territory. These data will be closely tracked amid recent signals from BoC policymakers that a tightening move may be on the cards soon. Another month of solid employment gains could add fuel to such speculation.

As for the speakers, BoE Governor Mark Carney speaks. Following his hawkish remarks last week, it will be interesting to see whether he continues to share the same view.

XAU/USD

Support: 1217 (S1), 1210 (S2), 1200 (S3)

Resistance: 1230 (R1), 1240 (R2), 1248 (R3)

USD/JPY

Support: 113.45 (S1), 112.90 (S2), 112.50 (S3)

Resistance: 113.90 (R1), 114.40 (R2), 114.90 (R3)

GBPJPY Maintains Uptrend But Reaches Overbought Levels On 4-Hour Chart

GBPJPY has been in an uptrend since rising from the June 12 low of 138.65. The pair hit a high of 147.60, nearing a one-month high. The May 10 high of 148.09 is in sight as the next target.

The RSI is approaching overbought levels on the 4-hour chart which suggests that GBPJPY may consolidate or pullback in the near term.

The 20-period moving average, currently located at 146.53, could act as a potential support level for any downside moves. Below this, important support comes into view at 146.00. This level has been tested several times in the past week and is considered to be a strong support mark. If it fails to hold, prices could fall towards another key level at 145.00. A drop from here opens the way towards support at 144.20 (June 27 high) and 143.25 (June 28 low). A deeper decline would change the current uptrend and the bias would turn bearish.

Alternatively, if GBPJPY regains upside momentum, a break of 147.60 could accelerate a move higher and strengthen the uptrend with scope to reach the May 10 high of 148.09 and from here the 150 handle would be targeted. The short-term outlook remains bullish as long as the market is trading above the moving averages.

Yen Falls On BoJ Bond Purchases, Dollar Gains Ahead Of Jobs Report

During the Asian trading session, the yen fell against the dollar amid the latest Bank of Japan bond intervention. This helped the greenback reverse its losses against the yen following yesterday's disappointing set of data out of the US. The focus of the day will be on the key jobs report to be released later in the day by the US Labor Department.

The yen weakened against its major counterparts after the BoJ announced it was ready to purchase an unlimited amount of Japanese government bonds in a move aimed at capping a rise in yields. Dollar/yen rose to half a percent to its highest level since mid-May during the Asian trading session. The pair was last trading at 113.71. Euro/yen rose to its highest level in 17-months, reaching an intra-day high of 129.91.

The dollar index, a broad measure of the greenback's strength, rose 0.11%, retracing some of yesterday's weakness, last trading at 95.91 as the Asian session was coming to a close.

Investors are eyeing the US nonfarm payrolls report for June, to be released later in the day. A weak reading could confirm investors' concerns about a potential change in the Federal Reserve's current thinking about further monetary policy tightening. Economists are expecting US employers to have added 179 thousand jobs last month, above May's gain of 138K. At the same time, unemployment is forecasted to remain at 4.3% and average earnings to increase 0.3% month-on-month.

The euro has been under pressure against the dollar, falling to $1.1415 towards the end of the Asian session. An upbeat German industrial production figure provided some support to the euro, though it was short-lived. Production rose 1.2% in May, month-on-month, well above the expected 0.3% and the prior month's 0.7% gain, potentially signalling a strong second quarter.

Sterling also weakened against the dollar, after two days of gains, last trading at $1.2953 ahead of the European session. A surprise in May's industrial production in the UK could lead to significant moves in pound/dollar when it gets released at 8:30 GMT. Economists are expecting a gain of 0.5% month-on-month, up from April's 0.2%.

Oil prices continued to be under pressure for the third consecutive day. West Texas Intermediate tumbled 1.3% to $44.94 a barrel, while Brent crude fell 1.1%, to last trade at $47.6 a barrel.

Gold slipped to 1,221.85 an ounce. The precious metal has not managed to recover following its plunge on Monday, making this week's loss its worst performance since early May.

Traders could also focus on a two-day G20 summit in Germany that starts today for clues about the economic policy of the world's major economies.

EURUSD Recovers, Back To 1.1400

The US dollar fell yesterday after nearly four straight sessions of the gains. The declines came as the ADP private payrolls rose less than expected. While economists were expecting a headline print of 184k, ADP/Moody's data showed that private payrolls rose just 158k. The jobs numbers for May were also revised down to 230k. Later in the day, the ISM non-manufacturing index rose to 57.4, beating estimates of 56.5 and up from May's 56.9. But the data couldn't help the greenback to recover.

Looking ahead, the US nonfarm payrolls data will be coming out later today. Expectations are for a headline jobs print of 175k, while the average earnings are expected to rise 0.3% on the month. The US unemployment rate is expected to remain steady at 4.3%. Canada will also be releasing the jobs report. Canadian unemployment rate is expected to stay put at 6.6%, unchanged from the previous month, while the Canadian economy is expected to add 11.4k jobs during June.

The BoE Governor, Mark Carney will also be speaking later in the day, followed by Canada Ivey PMI data.

EURUSD intraday analysis

EURUSD (1.1419): The EURUSD recovered sharply to regain the $1.1400 handle. The gains came as the ECB policy meeting minutes showed that members of the governing council were considering to remove the pledge for further easing. So far, the euro is reacting positively to any hints of hawkish messages from the ECB. The rally to 1.1400, however, comes with risk. A possibility of a lower high forming here could signal a longer-term decline back to 1.1300 and potentially to 1.1129. This bearish bias could however change should the EURUSD manage to hold at the current levels and push past the previous highs of 1.14450.

GBPUSD intraday analysis

GBPUSD (1.2972): The British pound continued to edge higher with price action seen testing the resistance level at 1.2975. If the resistance level holds out here, we could expect a reversal to the downside. GBPUSD could be potentially testing the support at 1.2800 which previously served as resistance. On the 4-hour chart, the current rally to 1.2875 signals a lower high in the making. It is best to wait for a reversal pattern here before considering the correction towards 1.2800. The BoE Governor Carney’s speech today could add some volatility, although the broader expectations are that the comments could be hawkish

USDJPY intraday analysis

USDJPY (113.65): The USDJPY is seen attempting to break above the 113.36 handle. This level marks the completion of the bullish flag pattern. Price action could be seen consolidating at the current levels with the risk to the downside. Failure to post a convincing close above 113.36 on a daily basis could signal a correction towards 112.00 - 111.72 level of support. On the daily chart, price action has already showed a few sessions closing nearly flat which suggests that the upside momentum could be fading. Today's nonfarm payrolls report could be crucial as this could help push the currency pair higher. Watch for an intraday break below 113.36 to confirm the correction to 112.00.

Technical Outlook: GBPUSD Remains Tall After Thursday’s Rally, US NFP In Focus For Fresh Signals

Cable is holding narrow range on Friday, awaiting US NFP report. Thursday's rally on weaker dollar moved the pair away from 1.2900 zone, where daily cloud top offered support and contained recent pullback from 1.3029 peak.

Bullish technical studies favor further upside, however, US jobs data are seen as key driver on Friday.

Scenario of lower than expected US jobs numbers in June would boost sterling for fresh probes above 1.3000 barrier, with break above recent tops at 1.3029/47 to open next key resistance at 1.3109 (Fibo 38.2% of larger 1.5016/1.1930 descend.

Conversely, upbeat NFP release could depress pound for renewed attack at pivotal 1.2904/1.2893 supports (daily cloud top / 05 July correction low), violation of which would trigger deeper pullback and expose next supports at 1.2873 (55SMA) and 1.2837 (30SMA).

Res: 1.2983, 1.3000, 1.3029, 1.3047

Sup: 1.2948, 1.2904, 1.2893, 1.2873