Sample Category Title

Headline Disappointment Masks Solid Details for Q4 GDP

U.S. real GDP grew by 1.9% (annualized) in the fourth quarter according to the advance estimate, falling short of the median consensus estimate of 2.2%.

U.S. consumers, however, did not disappoint. Spending grew 2.5% (matching the median forecast for 2.5%), as spending on durable goods poster a third consecutive stellar quarter (10.9%). Spending on services was relatively weak, advancing only 1.3%, which was in part due to unseasonably warm weather depressing utility consumption.

Non-residential business investment accelerated in the fourth quarter. Total business spending grew 2.4%, as spending on equipment investment (3.1%) and intellectual property (+6.4%) outweighed a drop in structures (-5.0%).

Residential investment was also up a hearty 10.2%, after declining in the previous two quarters.

As expected, net-exports exerted a considerable drag on growth in the fourth quarter. Exports fell 4.3%, after jumping 10% in the third quarter, on a one time surge in soybean exports. More surprising was the 8.3% surge in imports. In total, net exports subtracted 1.7%-points from growth, after adding 0.9%-points in the third quarter.

Inventory investment was another big contributor to the headline, adding 1.0%-point.

Key Implications

While the fourth quarter growth headline came in short of expectations, much of the weakness stemmed from a larger-than-expected rebound in imports. The details on domestic demand were much stronger. Final domestic demand was up 2.5%, a step up from 2.1% in the previous quarter. Domestic demand is a better predictor of future growth than headline GDP, and the strength augurs well for the next year. Moreover, this estimate of GDP growth relies on incomplete information. There has been a consistent pattern of upward revisions to growth estimates over the past year, so this is not the final word on fourth quarter growth.

With all of 2016 now on the books, the economy grew by a modest 1.6% on an annual average basis, a step down from its 2.6% pace in 2015. However, this reflects a disappointing first half of the year. Looking at growth on a year-end to year-end basis, the U.S. economy grew by 1.9%, just slightly above the 2015 clip. We expect growth to accelerate above the 2.0% mark over the next year, supported by ongoing consumer spending growth and a firm rebound in business investment.

Today's report continues to show a U.S. economy that is still taking up economic slack, and warrants a gradual pace of rate hikes by the Fed. The Fed's preferred inflation measure was up a tame 1.3% in the fourth quarter, underscoring why the Fed can afford to be patient on rate hikes. In our recent Dollars & Sense publication, we outline that we expect the Fed to raise rates twice over the next year, raising its key policy rate every six months or so.

U.S. GDP Up 1.9% in Q4

- The advance estimate of U.S. Q4 GDP growth was 1.9%, down from 3.5% in Q3 but still marking a slightly 'above-trend' pace of growth.

- Net trade was the main source of drag in the quarter, although in part reflecting a reversal of a transitory food-led export gain in Q3. Excluding net trade and inventories, final sales to domestic purchasers rose 2.5%, marking the strongest increase since Q3/15.

Net trade subtracted an outsized 1.7 percentage points from Q4 GDP growth, although in part reflecting a reversal of a transitory jump in Q3 food exports. Overall exports declined by 4.3% in Q4 after jumping 10.0% in Q3. Imports jumped 8.2% in Q4 (the largest increase in 2 years). The import gain was consistent with stronger domestic demand with final sales to domestic buyers rising 2.5%, led by another strong gain in consumer spending (+2.5% in Q4 following a 3.0% increase in Q3), a modestly stronger increase in business investment (+2.4% in Q4 vs 1.4% in Q3) and a 10.2% jump in residential investment following two quarterly declines.

Our Take:

Although slower in Q4 than the increase in Q3, average growth in the second half of the year was nonetheless significantly improved from the disappointing 1.1% average increase in the first half. The composition of growth in Q4 was also, arguably, somewhat better than the Q3 gain. Net trade was somewhat disappointing with the drag in Q4 from that component more-than-retracing a jump in Q3 (much of which reflected a transitory jump in food exports that unwound in Q4); however, the typically more stable final sales to domestic buyers measure rose by its strongest pace in more than a year, in part reflecting a jump in residential investment but also a third consecutive rise in business investment. Early data on capital goods shipments released separately this morning point to the potential for further improvement in Q1 in that latter component. Although much uncertainty about the future of U.S. fiscal policy remains, we continue to expect that underlying economic activity continues to improve at a pace that should be sufficient to allow the Fed to continue hiking interest rates at a modest pace. Our forecast assumes 2 additional 25 basis point hikes to the fed funds target range this year.

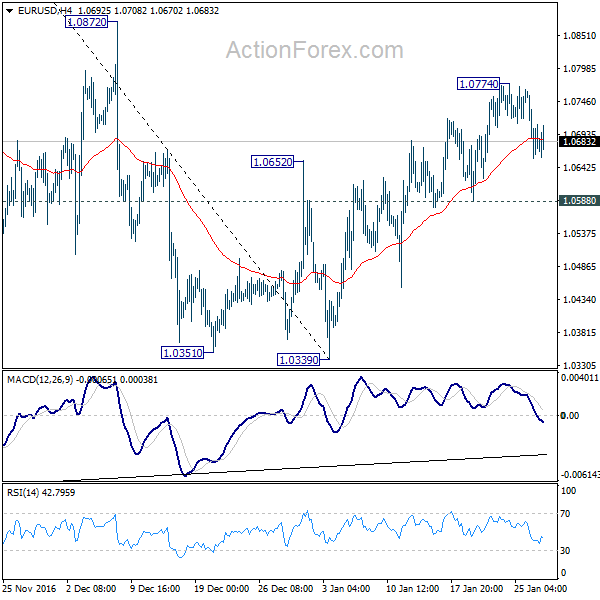

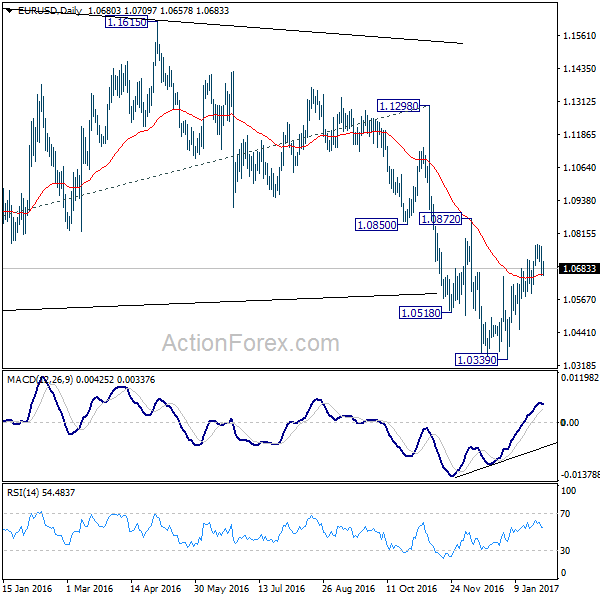

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0636; (P) 1.0701 (R1) 1.0744; More.....

Intraday bias in EUR/USD stays neutral for the moment. As noted before, choppy rise from 1.0339 is seen as a corrective move. Break of 1.0588 minor support will argue that it's completed and turn bias back to the downside for 1.0339 support. In case of another rise, upside should be limited by 1.0872 resistance.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2540; (P) 1.2607; (R1) 1.2657; More...

Intraday bias in GBP/USD remains neutral at this point. Rise from 1.1986 is seen as the third leg of the consolidation pattern from 1.1946. Break of 1.2414 support will indicate that it's completed and turn bias to the downside for retesting 1.1946 low. In case of another rise, upside should be limited by 1.2774 to limit upside and bring down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

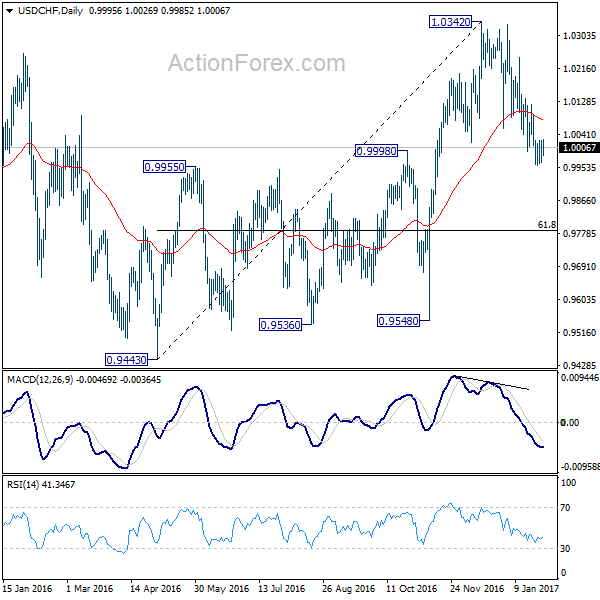

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9971; (P) 0.9999; (R1) 1.0029; More.....

Intraday bias in USD/CHF remains neutral for consolidation above 0.9958 temporary low. With 1.0121 minor resistance intact, deeper decline is still expected. As noted before, rise from 0.9443 has completed at 1.0342 already, after failing to sustain above 1.0327 key resistance. Fall from there would now target 61.8% retracement of 0.9443 to 1.0342 at 0.9786 and below. On the upside, break of 1.0121 resistance is needed to indicate short term bottoming. Otherwise, near term outlook will stay bearish in case of recovery.

In the bigger picture, rejection from 1.0327 resistance suggests that consolidation pattern from there is still in progress. Fall from 1.0342 is seen as the third leg and retest of 0.9443/9548 support zone could be seen. But we'd expect strong support from there to contain downside. At this point, we're still expect the larger rally to resume later to 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

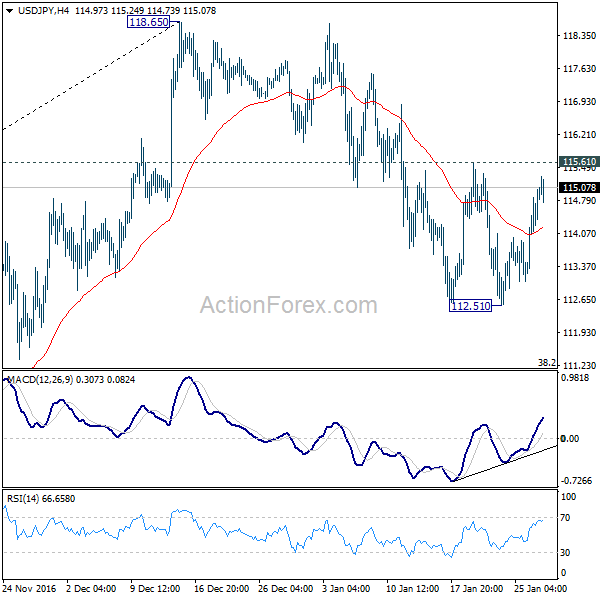

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.42; (P) 114.13; (R1) 115.23; More...

USD/JPY is still bounded in range of 112.51/115.61 and intraday bias remains neutral. No change in the view that choppy fall from 118.65 is a corrective move. Break of 115.61 will indicate that it's completed and will turn bias to the upside for retesting 118.65 resistance. Break will resume whole rise from 98.97 and target 125.85 key resistance. Below 112.51 will extend the decline but downside should be contained by 38.2% retracement of 98.97 to 118.65 at 111.13 to complete the correction and bring rebound.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

Dollar Recovery Lost Steam after Disappointing Q4 GDP

Dollar's recover lost steam quickly today and is set to end the week mixed. US GDP grew 1.9% annualized in Q4, below expectation of 2.2%. GDP price index rose 2.1%, met consensus. Durable goods orders dropped -0.4% in December, much lower than expectation of 2.6%. Ex-transport orders rose 0.5%, met expectations. UK prime minister Theresa May will meet US president Donald Trump in Washington today and that could be a focus. US futures point to a flat open and markets could turn into profit taking mode after record rerun in stocks.

Eurozone M3 rose 5.0% yoy in December versus expectation of 4.9% yoy. Bank loans to companies rose 2.3%, fastest since mid-2009. Household lending rose 2.0%, fastest since mid-2011. The set of data showed that ECB's cheap money is making its way through the economy. And such development could lift growth and inflation later down the road. Also from Eurozone, German import price index rose 1.9% mom, 3.5% yoy in December versus expectation of 1.3% mom, 2.7% yoy.

Yen falls broadly today on news that BoJ boosted JGB purchases. The move is seen as an act under the so called yield curve control to cap surge in yields, which touched 11 month highs earlier this week. The central bank said today that it would buy JPY 450b of JGBs with maturity of more than five to 10 years. That's nearly 10% above the prior size of JPY 410b. Released from Japan, national CPI core improved to -0.2% yoy in December, up from -0.4% yoy and above expectation of -0.3% yoy. Tokyo CPI core rose to -0.3% yoy in January, up from -0.6% yoy, and above expectation of -0.4% yoy. The set of inflation data showed mild improvement to inflation outlook. But it's still far from hitting BoJ's 2% target. Elsewhere, Australia PPI rose 0.7% qoq, 0.7% yoy in Q4. Import price rose 0.2% qoq in Q4.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.42; (P) 114.13; (R1) 115.23; More...

USD/JPY is still bounded in range of 112.51/115.61 and intraday bias remains neutral. No change in the view that choppy fall from 118.65 is a corrective move. Break of 115.61 will indicate that it's completed and will turn bias to the upside for retesting 118.65 resistance. Break will resume whole rise from 98.97 and target 125.85 key resistance. Below 112.51 will extend the decline but downside should be contained by 38.2% retracement of 98.97 to 118.65 at 111.13 to complete the correction and bring rebound.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Dec | -0.20% | -0.30% | -0.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jan | -0.30% | -0.40% | -0.60% | |

| 00:30 | AUD | PPI Q/Q Q4 | 0.50% | 0.20% | 0.30% | |

| 00:30 | AUD | PPI Y/Y Q4 | 0.70% | 0.50% | ||

| 00:30 | AUD | Import Price Index Q/Q Q4 | 0.20% | 0.40% | -1.00% | |

| 07:00 | EUR | German Import Price Index M/M Dec | 1.90% | 1.30% | 0.70% | |

| 07:00 | EUR | German Import Price Index Y/Y Dec | 3.50% | 2.70% | 0.30% | |

| 09:00 | EUR | Eurozone M3 Y/Y Dec | 5.00% | 4.90% | 4.80% | |

| 13:30 | USD | GDP (Annualized) Q4 A | 1.90% | 2.20% | 3.50% | |

| 13:30 | USD | GDP Price Index Q4 A | 2.10% | 2.10% | 1.40% | |

| 13:30 | USD | Durable Goods Orders Dec P | -0.40% | 2.60% | -4.50% | |

| 13:30 | USD | Durables Ex Transportation Dec P | 0.50% | 0.50% | 0.60% | |

| 15:00 | USD | U. of Michigan Confidence Jan F | 98.1 | 98.1 |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

Trump Effect Rekindles Global Risk Appetite

Global stocks marched into gains during trading this week after the renewed Trump fuelled optimism bolstered investor risk sentiment. Actions speak louder than words and the fact that Donald Trump has signed numerous executive orders since his inauguration continues to heighten hopes of the proposed fiscal stimulus measures materialising. Asian shares were mostly higher on Friday ahead of the Lunar year holiday while European markets edged lower amid profit taking. With the Trump effect back with a vengeance and optimism rapidly rising over Trump's pro-business policies elevating growth, Wall Street could maintain gains moving forward.

While the current gains displayed across global stocks are highly impressive, the lingering uncertainty could obstruct further upside in the longer term. Concerns are currently heightened over Trump's protectionist rhetoric while political risks across the globe weigh heavily on sentiment. Investors should remain diligent and be prepared to expect the unexpected this quarter when factoring the messy cocktail of market themes that may spark extreme levels of volatility.

Dollar Stabilizes above 100.00

The Greenback regained its dominant attitude on Thursday as prices stabilized above 100.00 after the Trump effect and optimism over the health of the US economy re-attracted bulls to install heavy rounds of buying. Sentiment has turned bullish towards the Dollar in the short term and further gains could be expected if buyers exploit the upside momentum created from fiscal stimulus-driven rally. Much attention may be directed towards Friday's fourth quarter GDP report which could offer some clues on how the US economy fared in 2016. A positive release that exceeds expectations may provide the Dollar an additional welcome boost that could propel the Dollar Index higher towards 101.00.

Although Donald Trump has revived the Dollar this week, there is a threat of him exposing the currency to downside risks in the future if the protectionist stance and overall uncertainty repels investor attraction. As of writing, the Dollar Index currently hovers around 100.63 with a breakout above 101.00 encouraging a further incline higher towards 102.00.

Sterling hovering around 1.2500

The Sterling bulls were exhausted on Thursday despite the positive fourth quarter UK GDP of 0.6% and such continues to highlight how the Brexit woes have damaged buying sentiment towards the currency. It has become very clear that the Brexit developments continue to dictate where the Sterling trades with uncertainty to likely limit upside gains. Sentiment remains firmly bearish towards the Pound with sellers potentially exploiting any further uncertainty or even a resurgent Dollar to drag the GBPUSD lower. Technical traders may pay close attention to how the prices react to the previous 1.2500 resistance level. A breakdown and daily close below 1.2500 could encourage a further selloff back towards 1.2350.

Commodity spotlight - Gold

Gold found itself exposed to painful losses this week after the renewed investor risk appetite from the Trump effect and Dollar's resurgence encouraged sellers to attack the metal incessantly. The yellow metal currently trades around a fresh two-week low at $1181 and is at risk of trading lower if the fourth quarter GDP for the United States exceeds expectations. The downside momentum is strong and a breakdown below $1180 could spark a further selloff towards $1160.

GBP/USD – May Hopes to Play Trump Card

GBP/USD has posted losses on Friday, continuing the downward movement in the Thursday session. Currently, the pair is trading at 1.2550. On the release front, there are no UK events on the schedule. Over in the US, it's a busy day, with the release of durable goods orders, UoM Consumer Sentiment and Advance GDP. The markets are expecting the GDP report, the first for Q4, to post a gain of 2.1 percent.

After the Brexit vote in June, many pundits predicted that the economy would tailspin. However, the economy has remained steady. On Thursday, Preliminary GDP beat the estimate, posting a strong gain of 0.6% in the fourth quarter of 2016. At the same time, negotiations with the European Union have not yet started, and even staunch Brexit supporters would be hard pressed to argue that the economy will not take a hit when Britain leaves the continental club, at least in the short term. On Friday, Prime Minister May meets President Trump in Washington, the first foreign leader to meet the new president. Trump has spoken glowingly about the Britain's decision to leave the EU, and May could use Trump's admiration and support to her advantage, in the form of a free-trade deal with the US. May will have to navigate through rough waters when she negotiates the terms of Brexit with the Europeans and is looking to return home with some progress towards a new trade agreement with the United States. Such a deal would be a key achievement for the British leader, who could then demonstrate to her opponents, both domestically and in Europe, that Britain can "go it alone" without the EU.

Barely a week into the presidency of Donald Trump, there are already signs of the economic approach the administration appears to be taking. Trump declared in his inauguration address that he would put "America first", and he has followed up with some protectionist measures. Trump formally withdrew the United States from the Trans-Pacific Partnership, a broad trade agreement that would have covered some 40 percent of gobal GDP. After announcing he would renegotiate the NAFTA agreement with Canada and Mexico, Trump took aim at his southern neighbor and announced that he would build a wall between the US and Mexico. Predictably, Mexico has reacted angrily to this move, and a scheduled meeting between Trump and Mexican President Enrique Peña Nieto has been cancelled. In the latest salvo in the growing crisis, the White House White House suggested imposing a 20 percent tax on Mexican imports to pay for construction of the wall. Trump's unconventional and disjointed approach to international trade could have major ramifications on global trade and could lead to financial instability in global markets.

EUR/USD – Euro Subdued As Markets Eye US GDP

EUR/USD is almost unchanged in the Friday session. Currently, the pair is trading just below the 1.07 level. On the release front, there are no major Eurozone releases. The US will release Advance GDP, with the estimate standing at 2.1 percent. We’ll also get a look at durable goods orders and UoM Consumer Sentiment.

There was positive news out of Germany, as consumer confidence continues to rise. The GfK Consumer Climate report rose to 10.2 points in December, climbing for a third consecutive month. Still, the Eurozone consumer is not as optimistic, as Eurozone Consumer Confidence, released earlier this week, was unchanged at -5 points. The Eurozone is showing some improvement, as manufacturing and inflation numbers continue to point upwards. On Thursday, an IMF report found that economic growth in the Eurozone was improving and projected growth of 1.6 percent in 2017 and 2018. However, the report also warned that political instability could on the Eurozone economy, with Britain’s departure from the EU and elections in several Eurozone countries where many voters are skeptical about European integration.

The Trump era is barely a week old, but there are already signs of the economic approach the administration appears to be taking. Trump declared in his inauguration address that he would put “America first”, and he has followed up with some protectionist measures. Trump formally withdrew the United States from the Trans-Pacific Partnership, a broad trade agreement that would have covered some 40 percent of gobal GDP. After announcing he would renegotiate the NAFTA agreement with Canada and Mexico, Trump took aim at his southern neighbor and announced that he would build a wall between the US and Mexico. Predictably, Mexico has reacted angrily to this move, and a scheduled meeting between Trump and Mexican President Enrique Peña Nieto has been cancelled. In the latest salvo in the growing crisis, the White House White House suggested imposing a 20 percent tax on Mexican imports to pay for construction of the wall. Trump’s unconventional and disjointed approach to international trade could have major ramifications on global trade and could lead to financial instability in global markets.