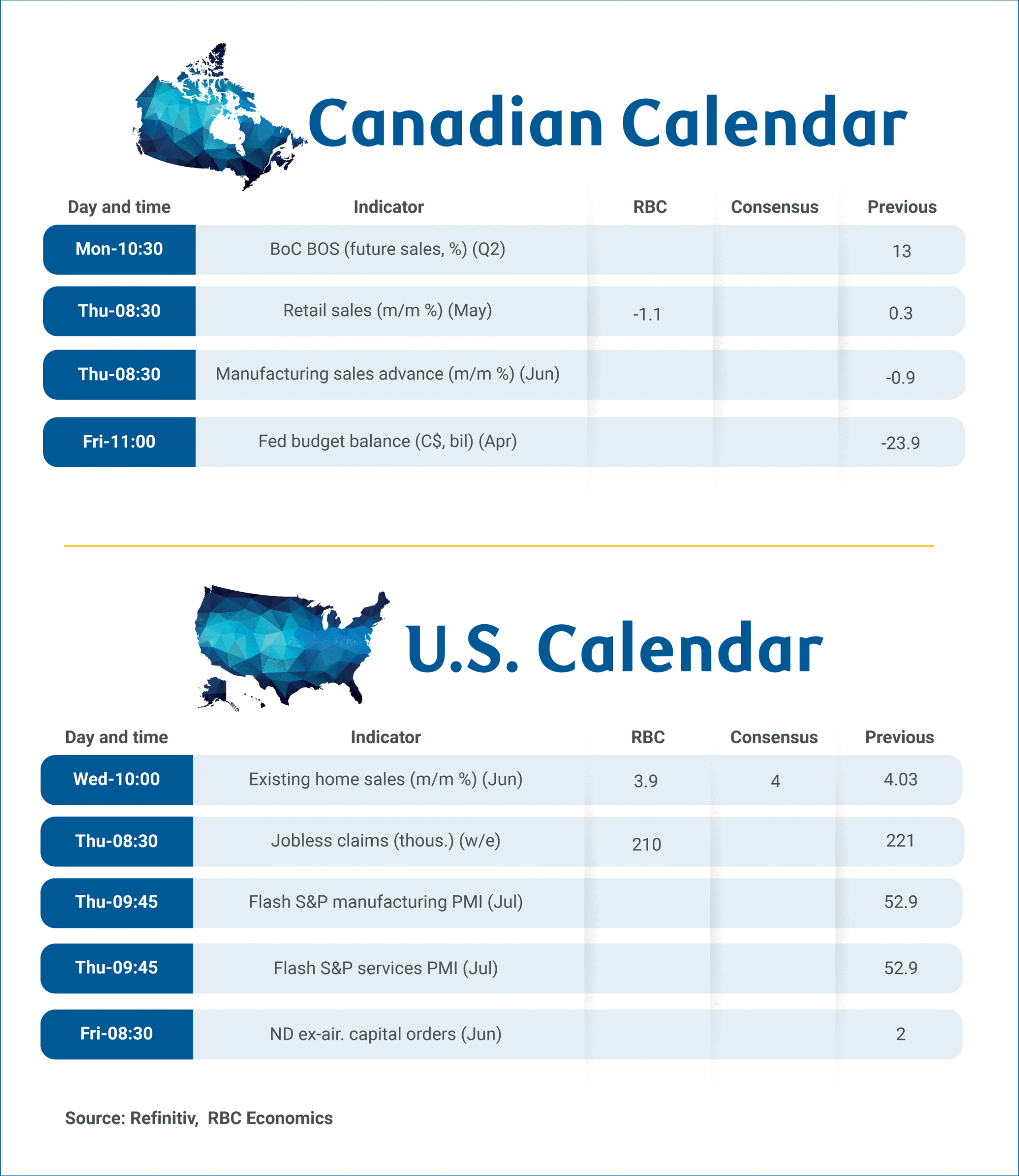

The Bank of Canada’s Business Outlook Survey on Monday is expected to show early signs of stabilization in businesses’ expectations for future sales, input prices and hiring in Q2.

The likely improvement follows marked deterioration in Q1, and was during a survey period (Q2 typically spans from early to late May) when threats specifically targeting Canada had receded.

Indeed, as much as Canada was a main focus of trade grievances earlier in Q1, it was excluded from the list of U.S. trade partners facing reciprocal tariffs in April. A duty-free exemption for trade compliant with the USMCA imposed in March also remains in effect.

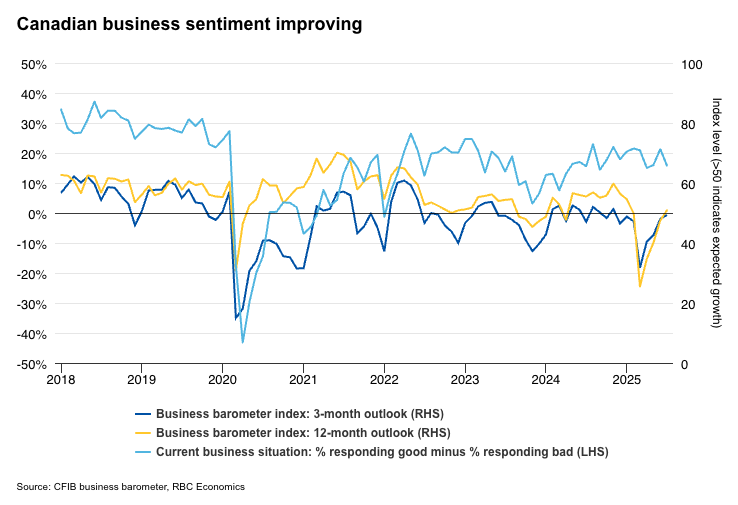

Indicators have broadly pointed to a stabilizing economic backdrop in Q2. Job openings from Indeed.com steadied into the summer following earlier declines. Business confidence in Canadian Federation of Independent Business surveys continued to improve in July after plunging in March.

We expect next week’s BOS will largely mirror these trends. More significantly, the survey could highlight a divergence between sectors directly exposed to trade headwinds (such as manufacturing and transportation), which will likely maintain a softer outlook, while other sectors, particularly consumer-facing businesses, that are more positive.

The BoC will be watching inflation expectations closely, after a string of mostly hotter consumer price index reports raised concerns that resilience in consumer spending is also leading to resilience in inflation.

Inflation expectations already drifted broadly higher for businesses and consumers in Q1. The early estimate of retail sales was a 1.1% decline in May from April, but to levels that are still resilient relative to low consumer confidence. Our tracking of card transactions pointed to further resilience in June.

Broadly, that kind of a backdrop—better than feared growth and higher than wanted inflation topped with in the prospect of significant fiscal stimulus spending in the year ahead —leaves an high bar for the BoC to make additional interest rate cuts this year. We do not expect further interest rate reductions from the BoC.

Week ahead data watch:

According to the StatsCan’s advance retail indicator, sales declined by 1.1% in May. By our count, much of this slowdown was driven by a decrease in auto sales during the month. Gas prices edged slightly lower on a seasonally adjusted basis, and we anticipate that sales at gas stations remained little changed during that month.

{kind=link}