Recent softening in North American labour market data has brought back prospects for additional and earlier interest rate cuts from central banks.

The U.S. Federal Reserve is now widely expected to cut rates on Wednesday for the first time since December in the wake of softening job reports over the summer. U.S. job growth has essentially stalled since April, leaving a much less resilient backdrop to initial tariff impacts than previously estimated. It’s also overriding concerns about inflation holding above the Fed’s 2% objective.

In Canada, we expect the decision will be a closer call, and closer than the high likelihood of a cut currently priced into markets. The Bank of Canada is weighing signs of softening in the economy (higher unemployment, lower exports) against broader inflation concerns. We look for the central bank to narrowly opt for a hold on interest rates. Although, that will also depend on the August consumer price data out on Tuesday—the day before the decision.

Economic data in Canada has deteriorated, but not significantly more than the BoC expected. A 1.6% decline in Q2 gross domestic product was broadly in line with the 1.5% decline assumed in the July Monetary Policy Report. Early data for Q3 suggests that the Q2 decline—driven largely by a pullback in net trade, and concentrated in the manufacturing sector—is unlikely to be repeated. Export volumes stabilized into July, and the preliminary estimate of July’s manufacturing sales showed a 1.8% increase.

There are still sectors that are being significantly impacted by trade disruptions, but that has yet to spread broadly across the economy. Labour markets have softened, but with job losses largely concentrated in heavily trade-exposed sectors. There is clearly an argument for policy support to those sectors, but fiscal policy (federal and provincial government spending) is better suited to provide targeted and timely support than across-the-board interest rate cuts.

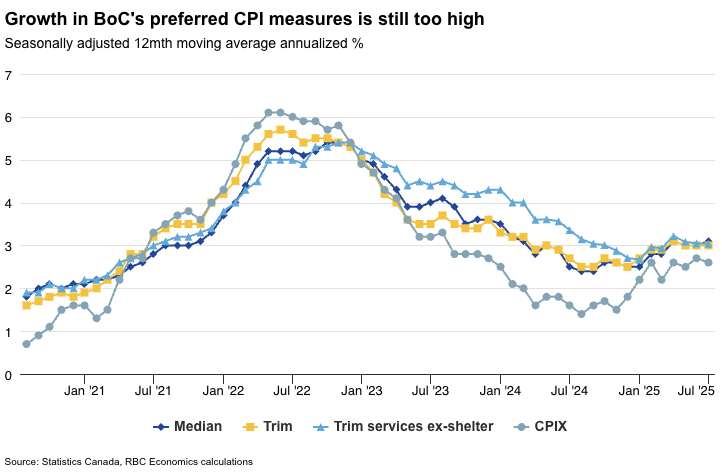

Inflation reading could be the decider

Federal and provincial spending plans are already ramping up, and lowering interest rates further risks adding to inflation pressures in other parts of the economy where activity has been more resilient. Consumer spending grew sharply in Q2 despite an overall GDP decline, and housing markets have been showing signs of life.

August’s CPI could be the deciding factor between a cut and hold for the BoC. Year-over-year CPI growth is still being biased lower by a drop in energy prices, in large part due to the removal of the consumer carbon tax from gasoline prices in most provinces in April. But, we expect headline price growth to tick up to 2.1% from 1.7% in July, and for price growth, excluding food and energy products, to rise to 2.8%. The BoC’s own preferred median and trim core CPI measures are expected to have held around 3% (the top end of the central bank’s inflation target), extending the trend seen over the summer.

Week ahead data watch:

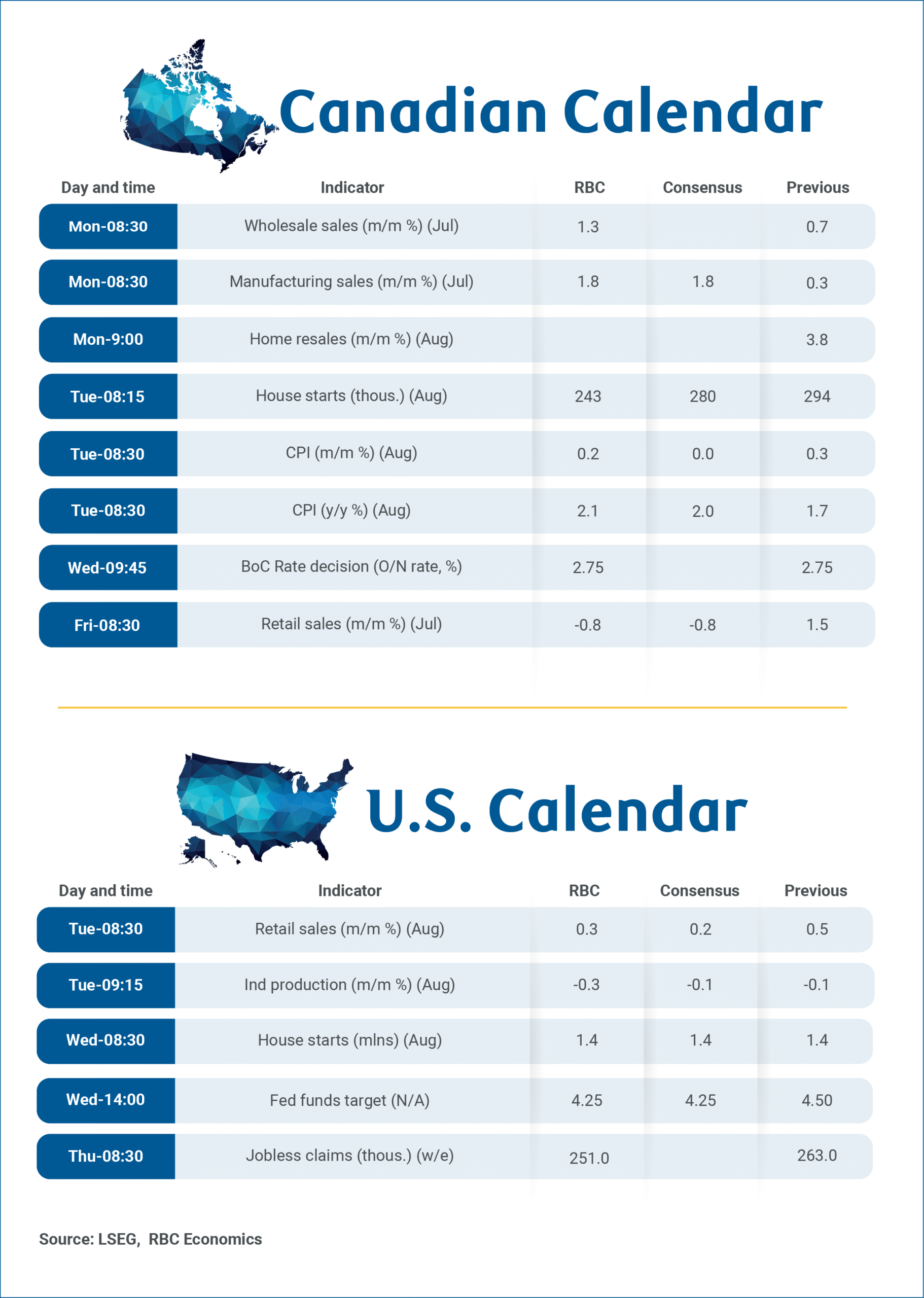

The early estimate of July Canadian manufacturing sales showed a 1.8% increase from June. Producer price index data for July suggests roughly a percentage point of that increase came from higher prices

The early estimate of Canadian July retail sales was down 0.8% – partially retracing a 1.5% increase in June and with details that we expect will remain broadly consistent with resilient consumer spending trends in the spring extending into the summer. We expect core (excluding the volatile motor vehicle and gasoline components) was stronger with sales at both auto dealerships and gasoline stations tracking lower in July.

We expect U.S. retail sales edged higher (+0.3%) in August but production in the heavily trade exposed manufacturing sector is expected to continue to show the strain from tariffs. Manufacturing hours worked fell by 0.5% in August and we expect industrial production declined 0.3%.

Canada’s August home resales report should show further signs of stabilization in housing markets over the summer based on early market reports.

{kind=link}