Summary

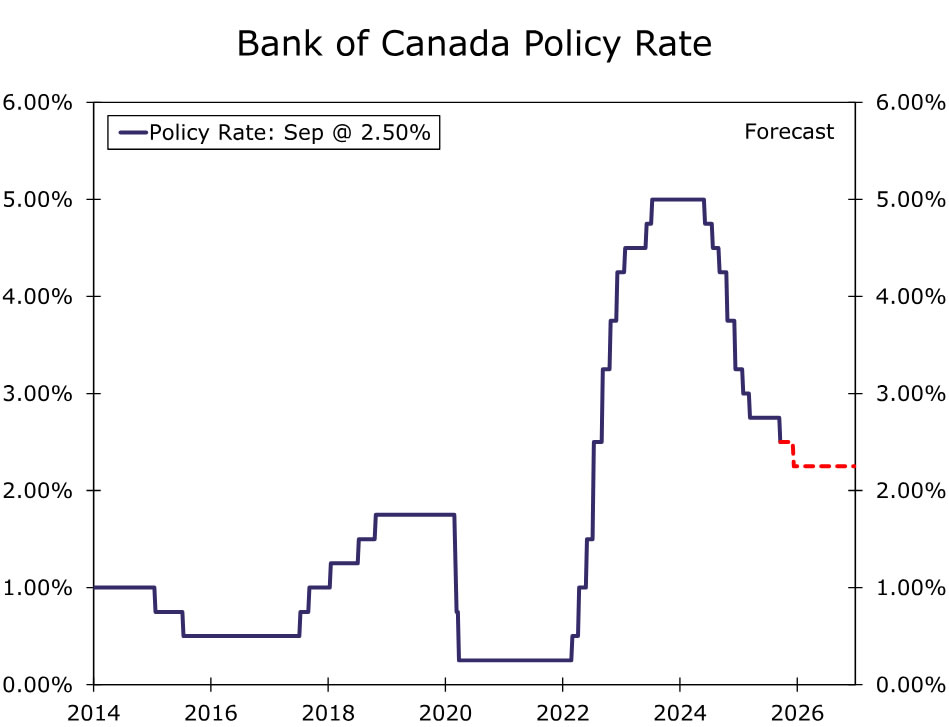

- The Bank of Canada (BoC) resumed its monetary easing at today’s announcement, lowering the policy rate by 25 bps to 2.50%. The central bank said a weaker economy, combined with less upside risk to inflation, justified today’s rate cut.

- While the central bank’s assessment of the economy’s prospects and inflation risks has softened, the BoC did not offer an explicit signal of a possible further reduction of interest rates at today’s announcement. In that context, for now, we lean against the central bank delivering a back-to-back rate cut in October. Instead, we anticipate the next 25 bps rate cut will come at the BoC December announcement, which would take the BoC’s policy rate to a cycle low of 2.25%.

- From a broader perspective, however, we acknowledge that the balance of risks around our Bank of Canada outlook is likely tilted toward earlier or more monetary policy easing. Among the key upcoming releases, should September see yet another decline in employment, Q3 business confidence show a further softening, and September inflation show reasonably benign price pressures, that could be enough for the central bank to lower interest rates again in October.

Bank of Canada Resumes Rate Cuts

The Bank of Canada (BoC) resumed its monetary easing at today’s announcement, lowering its policy rate by 25 bps to 2.50%. The rate cut was widely expected by market participants, although we had leaned towards the BoC extending its monetary policy pause and holding rates steady. In deciding to lower interest rates, BoC policymakers noted both softening growth and diminishing upside inflation risks. Among the main aspects of today’s announcement, the BoC said:

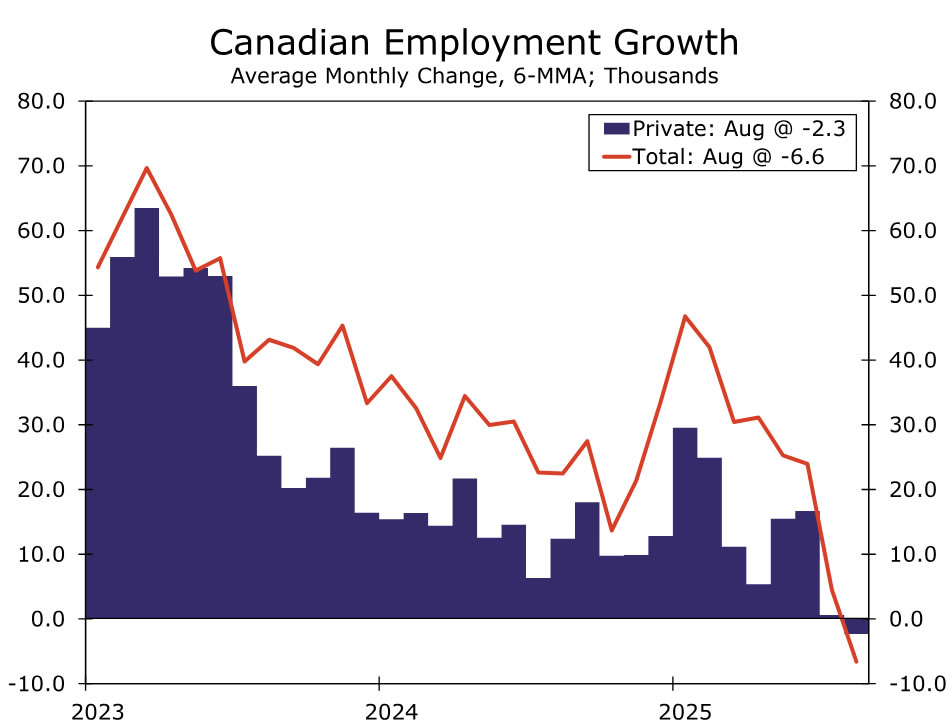

- Canada’s Q2 GDP declined as expected in the second quarter, with both exports and business investment weaker. Consumer spending grew at a healthy pace, but weakness in the labor market will likely weigh on household spending in the months ahead.

- Employment has fallen in the past two months, with job losses concentrated in trade-sensitive sectors. Unemployment has risen, and wage growth has continued to ease.

- While core inflation has been around 3% in recent months, on a monthly basis the upward momentum seen earlier this year has dissipated. A broader range of indicators suggests underlying inflation is running around 2½%. In addition, the government’s decision to remove most retaliatory tariffs on imports from the United States should mean less upward price pressure moving forward.

The central bank said that with “a weaker economy and less upside risk to inflation, Governing Council judged that a reduction in the policy rate was appropriate to better balance the risks.” The BoC reiterated that it is “proceeding carefully, with particular attention to the risks and uncertainties” and that it will “be assessing how exports evolve in the face of US tariffs and changing trade relationships; how much this spills over into business investment, employment, and household spending; how the cost effects of trade disruptions and reconfigured supply chains are passed on to consumer prices; and how inflation expectations evolve.” Notably, and in contrast to the July announcement, the BoC did not offer an explicit signal of a possible further reduction in interest rates.

Ahead of today’s announcement, our view had been the Bank of Canada would ease monetary policy further, with the main question being one of timing. With the Bank of Canada not offering an explicit easing signal, for now we lean against the central bank delivering back-to-back rate cuts with another move at its October announcement, and instead anticipate the next 25 bps rate cut will come at the BoC December announcement, which would take the BoC’s policy rate to a cycle low of 2.25%. That said, both ourselves and the Bank of Canada are in “data-dependent” mode, and the key releases we will be watching in the coming weeks are the:

- September labor market report (released 10 October)

- Q3 Business Outlook Survey (released 20 October)

- September CPI (released 21 October)

Should September see yet another decline in employment, Q3 business confidence show a further softening, and September inflation show reasonably benign price pressures, that combination may well be enough for the central bank to lower interest rates again in October. Indeed, we acknowledge that from a broader perspective and in the event of sustained weakness in Canada’s economy, the balance of risks around our Bank of Canada outlook is likely tilted toward earlier or more monetary policy easing, with a terminal policy rate of 2.00% or even lower not out of the question.

resumed its monetary easing at today's announcement, lowering the policy rate by 25 bps to 2.50%. The central bank said a weaker economy, combined with less upside risk to inflation, justified today's rate cut.){kind=link}