Commodity currencies slipped in quiet trading today, with Aussie and Kiwi leading losses as regional equities pulled back. With Japan on holiday, volumes were thin, but risk sentiment deteriorated after both Chinese and Hong Kong tech stocks retreated from a month-long rally.

Australia’s PMI data added further weight to the currency. The September surveys showed softening momentum in both manufacturing and services, eroding confidence and fueling expectations that growth may be fragile heading into year-end. Markets widely expect the RBA to stand pat next week, but speculation lingers over whether policymakers will signal readiness to cut again in November.

Dollar, meanwhile, traded mixed. Investors are parsing a steady stream of Fed commentary following last week’s 25bps rate cut. New Governor Stephen Miran continued to push for larger moves, but other officials leaned more cautious, stressing that additional cuts are not automatic and depend on data.

Attention now turns to upcoming speeches from other Fed officials, with focus on Governor Michelle Bowman. Markets will be listening for her explanation of why she backed a 25bps reduction but resisted a deeper 50bps move last week. Chair Jerome Powell is also due to speak, though few expect him to deviate from the steady tone he struck just a week ago.

In performance terms, Loonie is the weakest performer so far this week, followed by Kiwi and Aussie. On the other side, Euro leads gains, with Swiss Franc and Sterling also firm. Dollar and Yen are positioned mid-pack. The tilt in momentum now favors Europe.

In Asia, at the time of writing, Hong Kong HSI is down -1.10%. China Shanghai SSE is down -1.22%. Singapore Strait Times is up 0.18%. Japan is on holiday. Overnight, DOW rose 0.14%. S&P 500 rose 0.44%. NASDAQ rose 0.70%. 10-year yield rose 0.004 to 4.122.

Fed’s Miran pushes for aggressive cuts, Bostic and others push back

New Fed Governor Stephen Miran defended his lone call for a 50bps rate cut last week, signaling he would back another such move if given the chance. In a speech overnight, Miran warned that the central bank is underestimating how tight policy is, putting the job market at risk without faster easing.

Miran argued that the appropriate federal funds rate should be in the “mid-2 percent area,” nearly 200 basis points below the current target. He said leaving policy this restrictive risks unnecessary layoffs and higher unemployment, with monetary settings “well into restrictive territory.”

His remarks highlighted the divide inside the FOMC. While Miran sees the economy requiring swift and decisive support, other Fed officials made clear they prefer a slower pace of adjustment.

Atlanta Fed President Raphael Bostic told the Wall Street Journal that inflation remains “too high for a long time” and warned against signaling premature victory. He flatly opposed another cut at the October meeting, indicating that “I today would not be…in favor of it.”

Cleveland Fed President Beth Hammack echoed caution, saying the policy rate is only a “short distance to neutral”. She warned that removing too much restriction could “start overheating again”, urging the Fed to tread carefully, and “stay restrictive to bring inflation back down to target.”

St. Louis Fed President Alberto Musalem said he backed last week’s 25bps cut as a “precautionary” measure to support employment but stressed there is only “limited room for easing further” without risking an overly accommodative stance.

Australia PMI composite hits three-month low at 52.1, confidence slumps

Australia’s private sector momentum slowed sharply in September, with PMI Composite falling from 55.5 to 52.1, its lowest in three months. Manufacturing eased from 53.0 to 51.6, while services slipped more heavily from 55.8 to 52.0, signaling a broad moderation in activity.

S&P Global’s Jingyi Pan noted that new business growth weakened after two strong months, with manufacturing orders slipping back into contraction as U.S. tariffs began to weigh. Export orders also faltered, while overall business confidence dropped to its lowest in a year, hinting at a softer growth outlook into Q4.

The survey did show resilience in employment, with job creation little changed from August. However, selling price inflation remained “at a level that was above the long-run average”, and a steep rise in manufacturing cost inflation underscored margin pressures for goods producers.

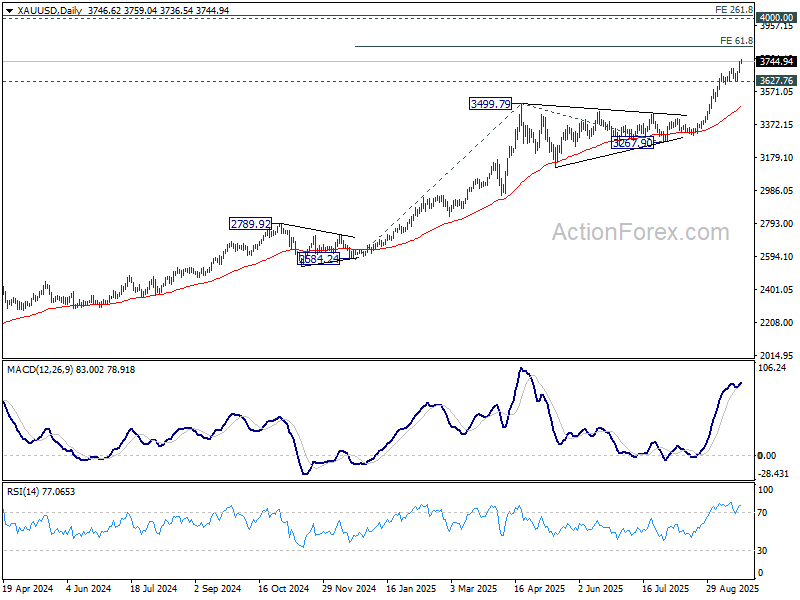

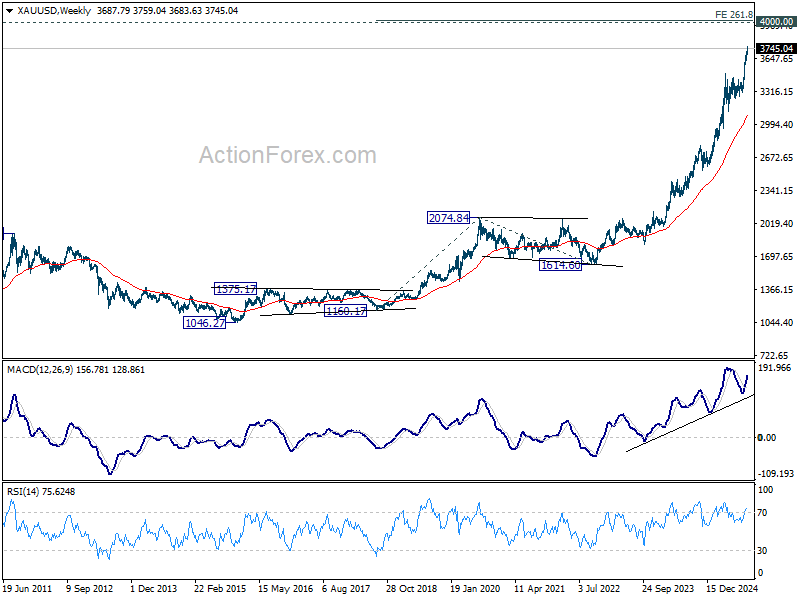

Gold’s record surge sets sights on 4000; Silver pushes toward 50

Gold and Silver extended their relentless rallies this week, with the former printing fresh record highs and the latter touching its strongest levels since 2011. The moves came despite a rebound in Dollar, highlighting the resilience of demand for safe-haven and strategic asset allocations. Gold is eyeing 4000 level, while Silver is pushing toward 50 mark, both psychologically and technically significant.

Extended inflows from central banks, sovereign wealth funds, and institutional investors remain at the core of the rally. The World Gold Council’s 2025 Central Bank Gold Reserves Survey, released in June, showed that 95% of central bankers expect global reserves to rise this year, with none forecasting a decline. Heightened geopolitical risk is the primary driver, while diversification away from Dollar continues to add impetus.

Silver’s fundamentals have reinforced its performance too. Tight supply conditions have helped maintain upward momentum, while structural demand from solar energy, electric vehicles, and electronics has added another source of resilience. Together, these factors explain why Silver has outpaced Gold in recent weeks.

Technically, there are various interpretations on the price actions since last record high at 3499.79. But in most cases, current up-leg should have started from 3267.90. For now, near term outlook will stay bullish as long as 3627.76 support holds. Next target is 61.8% projection of 2584.24 to 3499.79 from 3267.90 at 3833.70.

The longer-term picture for Gold is more compelling. The uptrend from 1046.27 (2015 low) is still in acceleration phase. Current rise from 1614.60 is seen as the fifth leg of the rally, targeting 261.8% projection of 1160.17 to 2074.84 from 1614.60 at 4009.20.

As for Silver, 61.8% projection of 28.28 to 39.49 from 36.93 at 43.85 target is already met and momentum stays strong as seen in D MACD. Outlook will remain bullish as long as 41.09 support holds even in case of retreat. Sustained trading above 43.85 will pave the way to 100% projection at 48.14.

More importantly, as the fifth wave of the rise from 17.54 (2022 low), Silver is on track to 161.8% projection of 21.92 to 34.84 from 28.28 at 49.18 too.

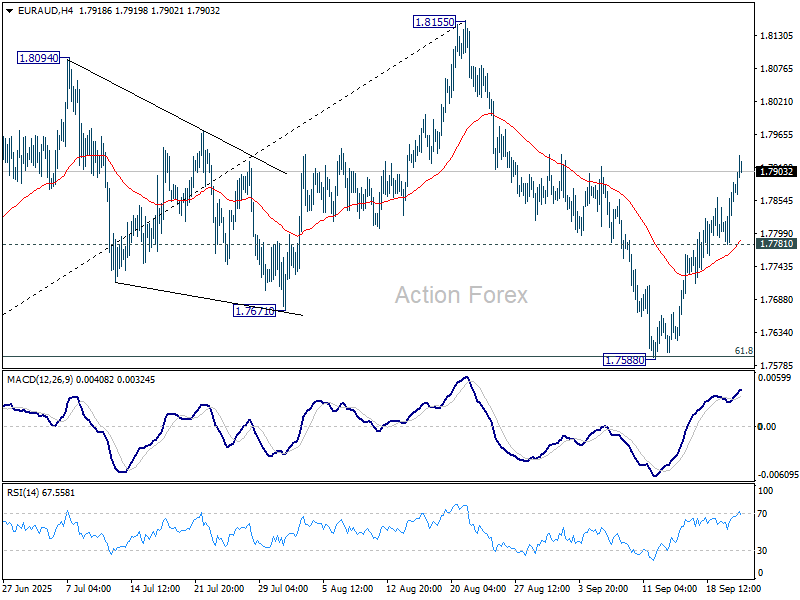

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7812; (P) 1.7850; (R1) 1.7916; More…

EUR/AUD’s rally from 1.7588 continues today and intraday bias stays on the upside. Further rally should be seen to retest 1.8155 resistance next. Firm break there will resume the whole rise from 1.7245. On the downside, below 1.7781 minor support will turn intraday bias neutral first.

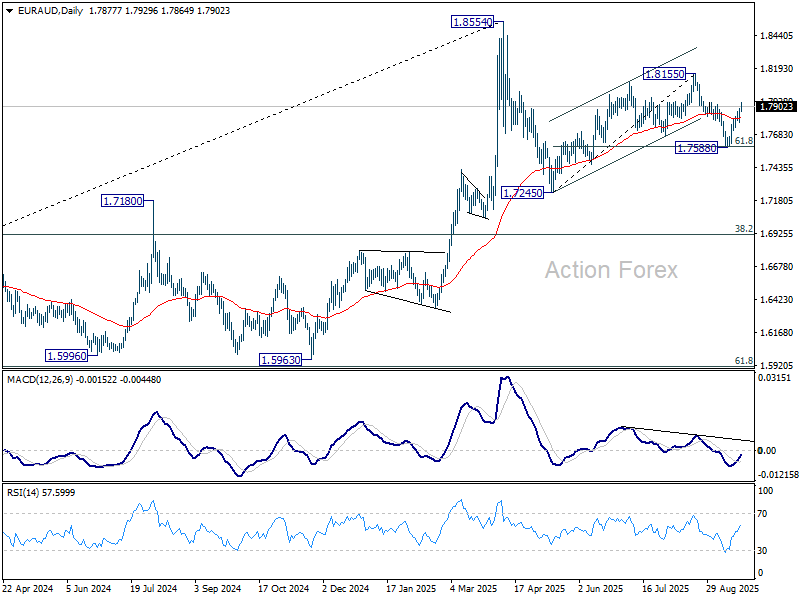

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

{kind=link}