Dollar weakened broadly in early US trade after a sharp miss in the ADP employment report. The data amplified concerns that US job growth is faltering, and rate markets reacted swiftly. A quarter-point Fed cut this month is now fully priced in, while the odds of another cut in December have jumped to nearly 90%.

However, the picture remains incomplete. The more comprehensive nonfarm payrolls report, which could confirm or challenge the ADP signal, may not be released if the US government shutdown persists. The closure — the first since 2018–19 — is going to disrupt data flows. Unless lawmakers strike a funding deal in the coming days, both Friday’s payrolls and Thursday’s weekly jobless claims could be delayed. Such an outcome would leave both the market and Fed officials flying blind, unable to validate the extent of labor market weakness.

In contrast, Yen extended its rally, with speculation intensifying that the BoJ could raise rates at its October 30 meeting. Today’s Tankan survey showed resilience in manufacturing despite tariff headwinds, adding weight to the hawkish case. Traders now assign a 40% chance of a quarter-point hike later this month. Attention will turn to speeches by Deputy Governor Shinichi Uchida on Thursday and Governor Kazuo Ueda on Friday. Their tone could be pivotal in confirming whether October is a genuine option, or if markets should expect a move later in the year.

Sterling has also gained ground, buoyed by reports that senior Labour figures are no longer ruling out increases in income tax, VAT, or employee national insurance — traditionally viewed as politically untouchable. Any adjustment here could provide the fiscal headroom needed to stabilize finances. Though, confirmation will have to wait until the November 26 budget.

Overall, Yen leads today’s FX performance, with Kiwi and Pound following. At the bottom,Loonie trails, alongside Swiss Franc and Dollar. Euro and Aussie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.68%, at new record. DAX is up 0.33%. CAC is up 0.37%. UK 10-year yield is down -0.009 at 4.692. Germany 10-year yield is down -0.005 at 2.711. Earlier in Asia, Nikkei fell -0.85%. Hong Kong and China were on holiday. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.002 t o 1.653.

US ADP payrolls drop -32k, small firms bear the brunt

US ADP private payrolls fell by -32k in September, far below expectations for a 50k increase and marking the steepest drop in two and a half years. August’s figures were also revised down to a loss of -3k from an initially reported gain of 54k.

The breakdown showed broad-based weakness. Service providers cut -28k jobs, while goods producers shed -3k. Small businesses were hit hardest, losing -40k positions, whereas large firms with 500 or more employees managed to add 33k.

ADP’s chief economist Nela Richardson said the data “further validates what we’ve been seeing in the labor market, that US employers have been cautious with hiring.”

Despite the slowdown, wage growth held steady. Average pay rose 4.5% yoy in September, little changed from August. However, the pace for job changers eased to 6.6% yoy, down half a percentage point, suggesting wage momentum is beginning to cool alongside weaker employment growth.

BoE’s Mann warns inflation persistence playing out

BoE policymaker Catherine Mann said today that keeping rates on hold is “appropriate for the current period,” and warned that the risk of sticky inflation remains elevated. Speaking to Bloomberg TV, she flagged “drift in inflation expectations” as a key concern, noting that it reinforces the persistence of price pressures.

Mann argued that the scenario outlined earlier this year — one where inflation risk lingers longer than expected — is now “playing out.” She added that the UK’s supply side continues to pose challenges for both the economy and policymakers, making it harder to fully restore price stability.

On trade, Mann said she does not yet see diversion effects feeding through as the “tariff landscape continues to be shifting.” “The domestic component is the more important issue that I need to face,” she said.

UK PMI manufacturing at 46.2, sector struggles with more worrying news

The UK manufacturing sector slipped further into contraction in September, with the PMI finalized at 46.2, down from 47.0 in August and marking a five-month low. Rob Dobson, Director at S&P Global Market Intelligence, called the results “further worrying news” for industry, pointing to weak demand, fading export orders, and a high-cost environment amplified by rising taxes and labor costs.

The report noted that the tough backdrop is eroding business confidence. Firms have now shed jobs for 11 consecutive months, with many cutting back on purchasing and non-essential spending. Sentiment about the year ahead remains subdued.

There were some glimmers of hope. Firms highlighted that lean inventories and potential easing in global trade tensions could lift output in the months ahead. Input costs are also rising at a slower pace, which may give the BoE scope to cut rates later this year.

Eurozone inflation ticks higher to 2.2%, core steady 2.3%

Eurozone headline inflation edged up in September, with CPI rising to 2.2% yoy from 2.0% yoy in August, in line with expectations. Core CPI, which excludes energy, food, alcohol and tobacco, held steady at 2.3% yoy, suggesting underlying price pressures remain sticky even as the energy drag eases.

By component, services posted the highest annual inflation at 3.2%, slightly higher than August’s 3.1%. Food, alcohol and tobacco slowed to 3.0% from 3.2%. Non-energy industrial goods were unchanged at 0.8%. Energy prices continued to decline, though the contraction moderated to -0.4% from -2.0%.

Eurozone PMI manufacturing at 49.8, stagnation can be viewed positively

Eurozone manufacturing activity edged back into contraction in September, with the PMI finalized at 49.8, down from August’s 50.7. Output slowed as well, with the production index falling from 52.5 to 50.9, pointing to weaker factory momentum across the bloc.

Country data painted a mixed picture. The Netherlands stood out with a 38-month high of 53.7, while Ireland and Greece also held above 50. Spain remained in expansion at 51.5 but slowed to a three-month low. Germany, France, and Italy — the region’s largest economies — all stayed below 50, signaling their industrial recessions are easing but not yet over.

Cyrus de la Rubia of Hamburg Commercial Bank said the “stagnation observed in the manufacturing sector can also be viewed positively,” given headwinds from US tariffs, political uncertainty in France and Spain, and high energy costs. He noted the sector is “holding up surprisingly well,” though confidence remains lower than the decade average.

Japan’s Tankan shows resilience, supports BoJ tightening outlook

Japan’s Q3 Tankan survey showed large manufacturers growing more confident, with the index rising from 13 to 14, in line with expectations and the highest since Q4 2024. While the manufacturing outlook held steady at 12, suggesting some softening ahead, sentiment remains resilient despite trade headwinds.

Non-manufacturing confidence also stayed firm, with the index unchanged at 34, beating forecasts, and the outlook improving to 28 from 27.

Large firms signaled robust investment plans, projecting a 12.5% increase in capital expenditure for the fiscal year to March 2026, up from June’s forecast of 11.5%.

The results suggest Japan’s economy is weathering tariff pressures and steady domestic demand continues to support activity. For the Bank of Japan, the data bolster expectations that further tightening is coming — the debate is less about if and more about when policymakers will move.

Japan PMI manufacturing finalized at 48.5, weak demand from China and US

Japan’s manufacturing sector contracted further in September, with the PMI finalized at 48.5, down from August’s 49.7. S&P Global’s Annabel Fiddes said the sector ended Q3 “on a weaker note,” as output and new orders declined at a faster pace, driven by softer demand across key markets such as China and the drag from US tariffs.

Weaker demand weighed on business confidence, leading firms to scale back activity. Employment expanded at the slowest pace since February, while purchasing activity dropped at the second-steepest rate since early 2024. The cautious stance underscores concern that the sector may “struggle to see much growth in the near term.”

Price dynamics offered some relief, with cost pressures “less pronounced” than earlier in the year. Still, selling prices rose at a “historically strong pace” as firms sought to protect margins.

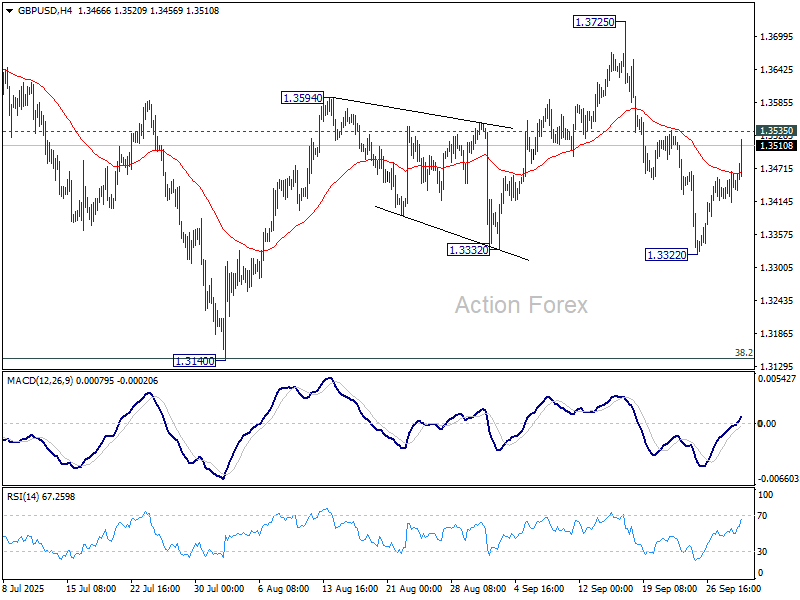

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3418; (P) 1.3442; (R1) 1.3471; More…

Focus is back on 1.3535 resistance in GBP/USD with today’s extended rebound. Firm break there will target 1.3725/87 key resistance zone. On the downside, though, break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

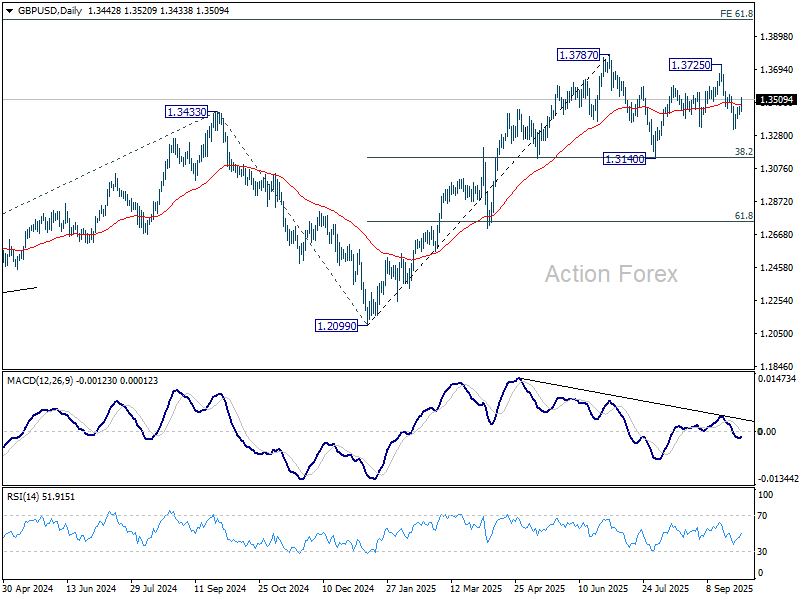

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

{kind=link}