Sterling weakened further today after UK inflation data surprised further to the downside, reinforcing expectations that price pressures are easing faster than previously thought. The softer CPI print extended losses in Sterling following a weak run of domestic data this week.

After inflation peaked at a lower-than-expected 3.8% earlier in the year, disinflation trend now appears to be accelerating. November’s data suggests that inflation is converging toward target more quickly. Alongside weaker UK labor market figures released yesterday, this week’s data all but seals the case for a BoE rate cut tomorrow. Market focus has already shifted beyond the decision itself toward how long the easing cycle could extend into next year.

On current information, policy easing is set to continue next year. The debate is not really about whether the BoE will cut again, but when. February and March are both plausible. Though February stands out given the availability of fresh economic projections, a factor that gains weight in light of this week’s data.

Elsewhere, Dollar staged a notable rebound as the sharp post-NFP selloff faded. After an initial surge, market-implied odds of a March Fed rate cut have slipped back to around 51%, reflecting a partial reassessment rather than a full reversal.

One interpretation is that while October’s sharp contraction in payrolls was clearly alarming, investors are holding out hope for a more sustainable rebound in hiring. Temporary drags from the government shutdown have cleared, while the one-year US–China tariff truce has reduced uncertainty around trade and pricing.

Looking ahead, the December, January, and February US employment reports, alongside inflation data, will be critical in shaping expectations for the March FOMC meeting. With such a heavy data pipeline, it is premature to place strong bets on further Fed easing. At least, that’s likely what the majority of traders think.

For now, the currency markets lack a strong directional bias. Yen leads for the week, followed by Dollar and Loonie, while Kiwi and Aussie lag. Sterling and Euro are stuck in the middle.

In Asia, Nikkei rose 0.26%. Hong Kong HSI is up 0.76%. China Shanghai SSE rose 1.19%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield rose 0.017 to 1.973. Overnight, DOW fell -0.62%. S&P 500 fell -0.24%. NASDAQ rose 0.23%. 10-year yield fell -0.033 to 4.149.

UK CPI undershoots at 3.2% as disinflation broadens in November

UK inflation eased more than expected in November, reinforcing signs that price pressures are moderating. Headline CPI slowed from 3.6% yoy to 3.2%, undershooting expectations of 3.5% and marking a second consecutive monthly decline. On a month-on-month basis, CPI fell -0.2% mom, adding to the disinflationary signal.

Underlying inflation also cooled. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.4% yoy to 3.2%, below forecasts of 3.4%, suggesting easing price pressures beyond volatile components.

The moderation was driven mainly by goods, where inflation eased from 2.6% yoy to 2.1% Services inflation edged slightly lower from 4.5% to 4.4%.

Japan posts first trade surplus in five months, US-bound shipments rebound

Japan’s trade data for November delivered a positive surprise, with exports rising 6.1% yoy to JPY 9.72 trillion, beating expectations of 4.8% yoy, and marking the third consecutive month of growth. The strength helped Japan record a JPY 322.2 billion trade surplus, the first in five months.

Exports to the US were a key driver, climbing 8.8% yoy. Auto shipments to the US rose 1.5%, marking the first increase since March and suggesting the drag from higher US tariffs is beginning to ease.

By contrast, exports to mainland China fell -2.4% yoy, weighed down by a sharp -5.9% decline in foodstuff shipments. That weakness came against a backdrop of renewed political tension, after Prime Minister Sanae Takaichi warned that a Chinese attempt to seize Taiwan could prompt Japanese military intervention, followed by Beijing restricting imports of Japanese seafood. Offsetting some of that drag, exports to Hong Kong surged 11.4%.

On the import side, growth was more subdued. Imports rose just 1.3% yoy to JPY 9.39 trillion, undershooting expectations of 2.5%.

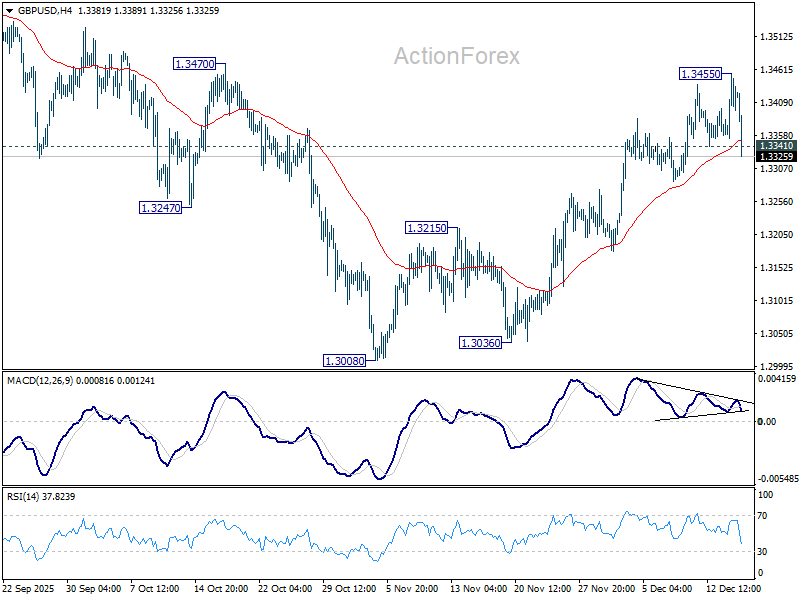

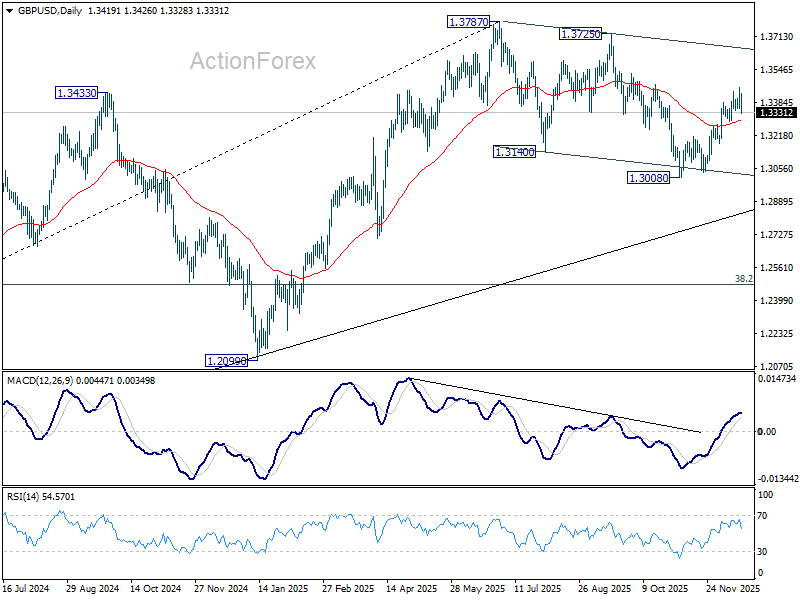

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3411; (R1) 1.3467; More…

Intraday bias in GBP/USD is turned neutral again with current retreat. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3293) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

{kind=link}