Canadian Highlights

- Canada’s data deluge showed a cooling trend in November core inflation, which reinforces the Bank of Canada’s shift to a hold stance.

- Canada’s population saw its steepest decline on record in the third quarter. Weak go-forward population gains should weigh on economic activity and maintain downward pressure on the unemployment rate.

- Canadian home sales and prices had a weak November, but we think 2026 should bring improved fortunes.

U.S. Highlights

- Employment growth slowed in the first two months of the fourth quarter, owing to the impact of deferred resignations on federal government employment.

- Inflation fell sharply in November, but the degree of the descent and the condensed nature of the data collection period warrants caution in interpreting the data.

- Federal Reserve officials continued to voice a spectrum of opinions on the outlook for monetary policy that on aggregate spoke to a cautious approach moving forward.

Canada – A Chilly End to 2025

While the U.S. had a cornucopia of data to whet the appetite, Canada had its own data buffet heading into the holidays. Most important for the Bank of Canada was the inflation report for November which showed a notable cooling in core inflation. Today’s retail spending report was also frosty, confirming a slowing trend in spending volumes. Alongside this, updates on the freeze in population growth, and a chill in housing construction all point to the Bank of Canada staying on the sidelines heading into 2026.

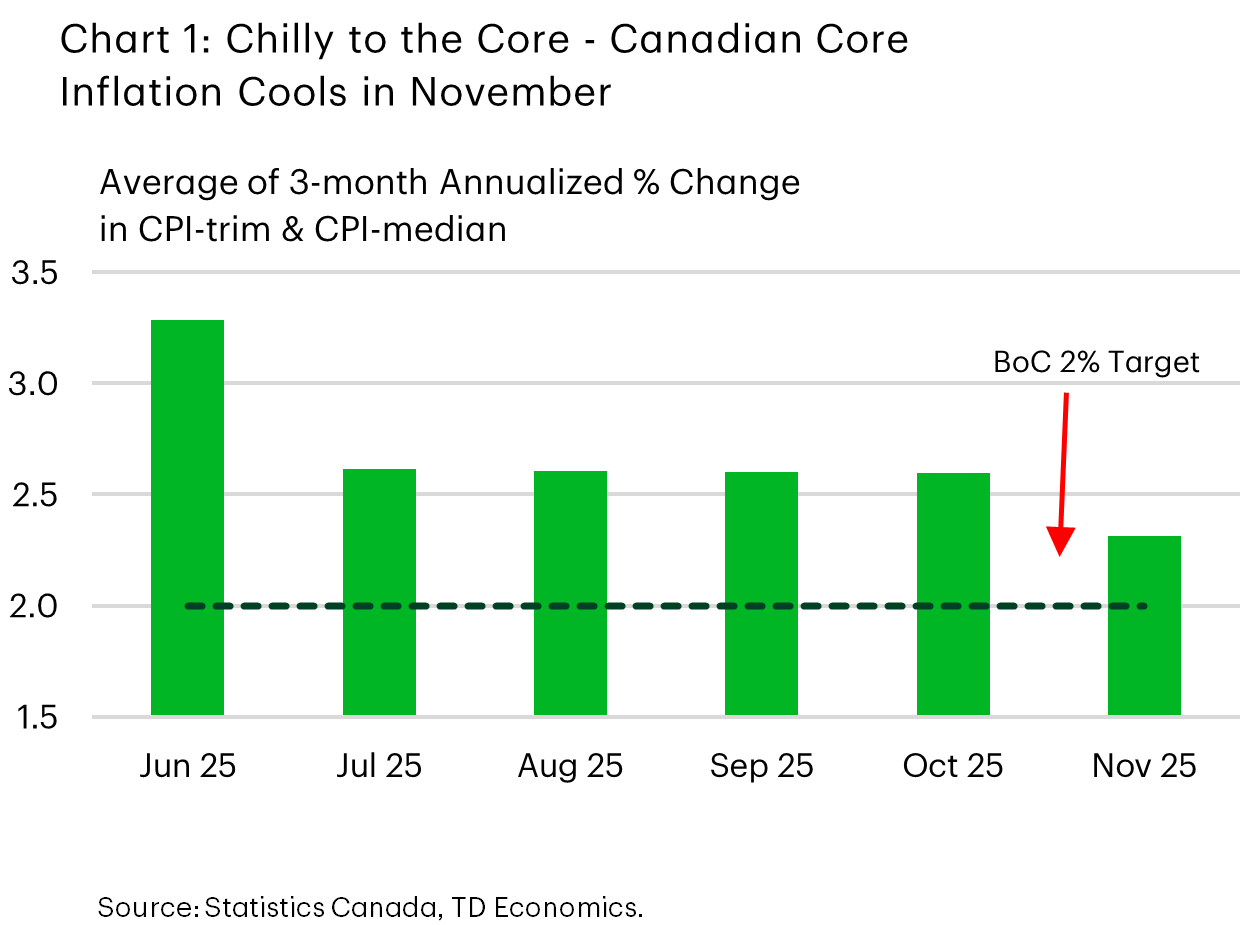

It seems a chilly winter breeze swept through key inflation metrics, as the Bank’s preferred core measures (median and trim) cooled to 2.8% year-on-year (y/y), while the three-month trends were even snowier (Chart 1). Headline inflation, meanwhile, was unchanged with some choppiness on deck for December, as last year’s GST holiday muddies comparisons. However, falling oil prices could offer some offset. Oil slipped again this week, greased by oversupply concerns. However, on-going tensions between the U.S. and oil producer Venezuela limited the extent of the decline.

The inflation report wasn’t all merry, with food prices playing the proverbial grinch. Grocery store prices climbed 4.7% (y/y), harkening back to the bad old days of pandemic inflation. This is something that will catch the eye of policymakers, as higher food prices can impact inflation expectations.

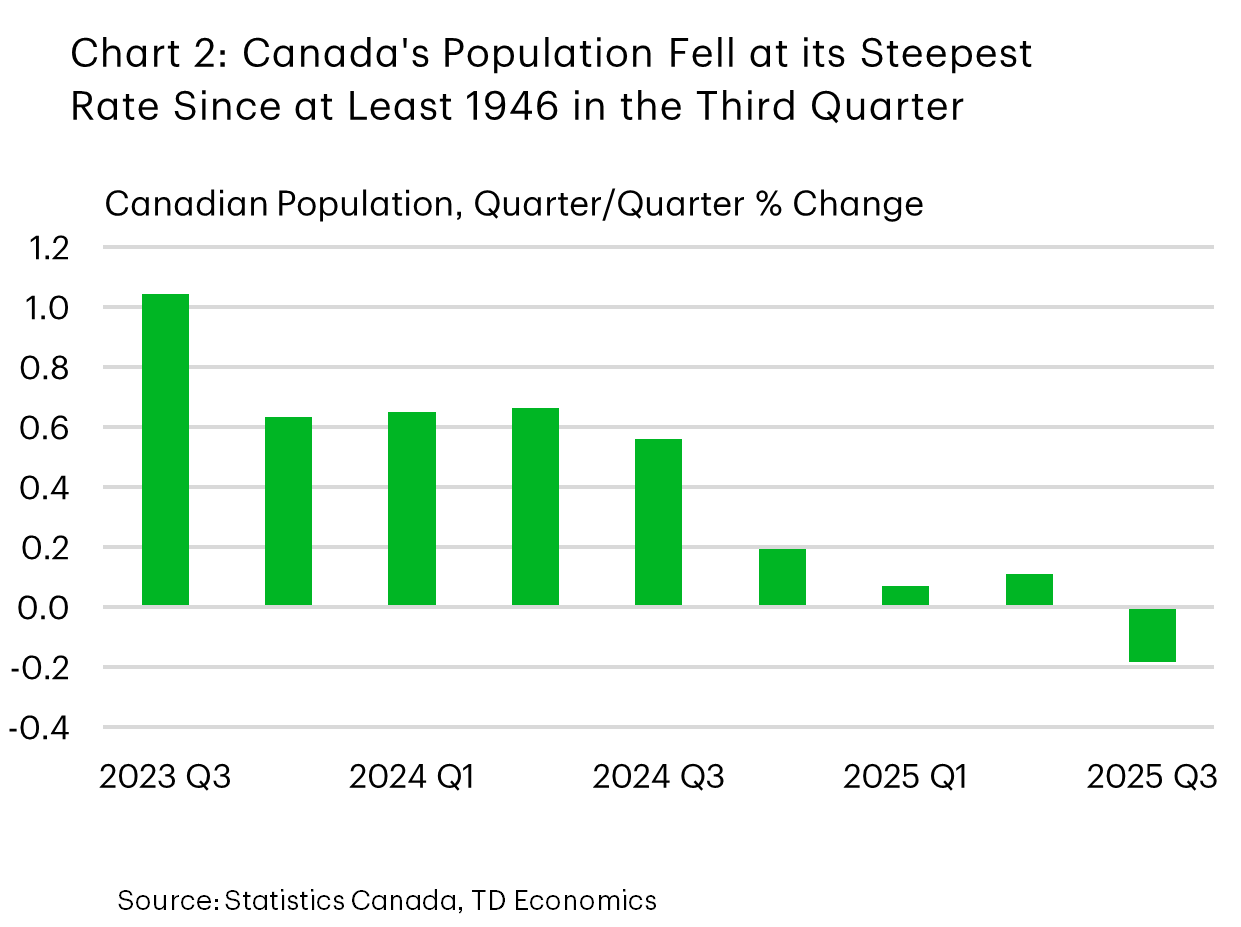

A key piece from the inflation report for the outlook was that rent growth continued to moderate. This is partially a function of the steep slowdown in Canada’s population growth, and this week featured a stark reminder of this trend. Canada’s population growth was downright frosty in the third quarter, slipping 0.2% quarter-on-quarter (Chart 2). This marked the largest decline on record! We anticipate 2026 to be another year of frigid population gains, which should restrain the pace of economic growth. Weak population growth will also weigh on the labour force, which should keep downward pressure on the unemployment rate.

Muted population gains will also drag on housing demand. In this vein, we received November data on Canadian home sales and average home prices this week. Overall, trends were cool, with home sales, average and benchmark prices all slipping a touch. We do, however, expect some improvement in both measures moving forward, benefiting from pent-up demand and amelioration in the Canadian jobs market. In contrast, housing starts popped higher in November but are on a downtrend which should extend into 2026, bogged down by a tepid pace of population gains.

Investors certainly had a lot of data to chew on this week and, all things considered, it was on the cooler end of the spectrum. However, it certainly wasn’t wintry enough to shake the Bank from their current hold stance. Indeed, we think the Bank will keep any changes to its policy rate on ice for the foreseeable future.

U.S. – Data with A Grain of Salt

This was arguably the biggest week for U.S. economic data in several months, as highly anticipated employment and inflation data delayed by the government shutdown was finally released. Financial markets largely took the data in stride, with U.S. Treasury yields falling slightly on the week, while equity markets were roughly unchanged as of the time of writing.

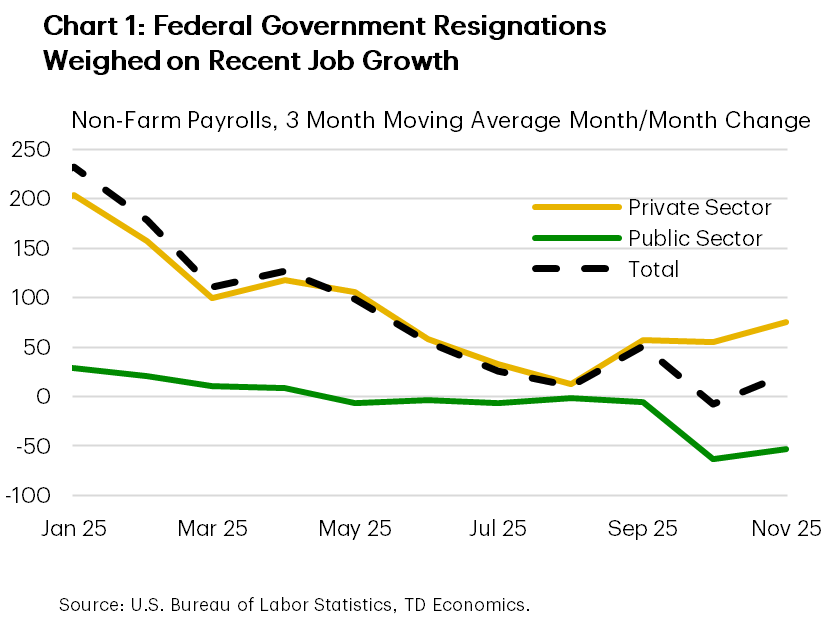

On the data front, the employment report showed that the economy continued to add jobs in the fourth quarter. However, headline job growth was weighed down by a large decrease in federal government jobs in October (Chart 1) – a byproduct of the deferred resignation offers sent out earlier in the year. Despite the near-term distortions, job growth has decelerated through the second half of the year, which has led to an uptick in the unemployment rate and motivated the 75 basis-point reduction in interest rates implemented by the Federal Reserve since September.

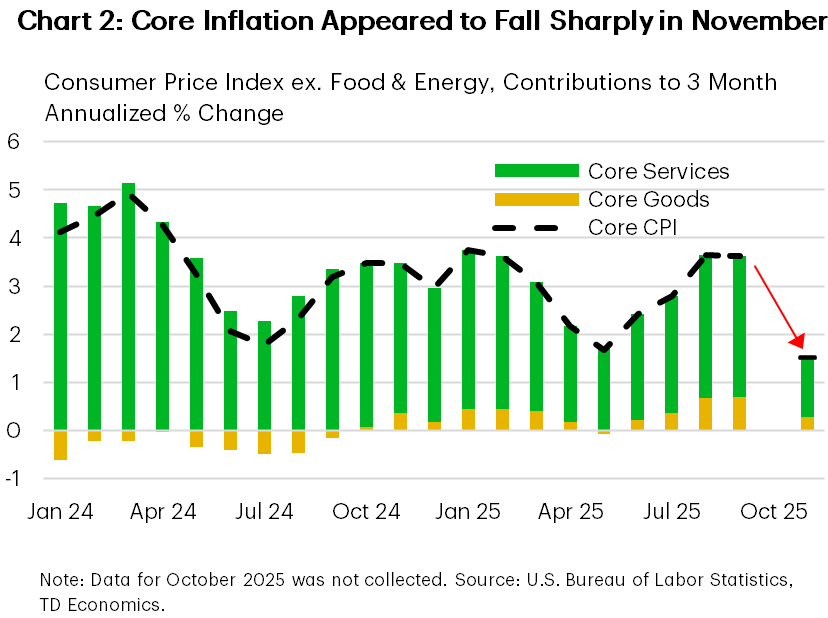

The pace of monetary policy easing has been deliberately gradual though, as inflation risks have been rising at the same time. However, November CPI data showed that there may have been a break in this trend in recent months, with the annual percentage change in core inflation falling to 2.6% – the lowest level since March 2021. Given the shorter collection period for this data owing to the government shutdown and the sharp drops recorded in several index categories (Chart 2), this data should be taken with a grain of salt. Market pricing for the Federal Reserve’s January meeting was largely unchanged, with only a 25% chance for a fourth consecutive cut.

The handful of Federal Reserve officials we heard from this week offered notably different assessments on the policy rate outlook. Miran made the case for aggressive rate cuts, positing that inflation metrics were anomalously high, while Waller also took a dovish tone but noted a gradual pace of rate cuts would be warranted going forward. On the other end of the spectrum was Bostic, who voiced greater concern for inflation risks and stated he did not currently see the need for rate cuts in 2026. Other speakers, including Vice Chair Williams, echoed Powell’s comments from his press conference last month that monetary policy was in a good place heading into 2026. Despite growing dissent among FOMC members, the balance of opinion is one of relative caution heading into the new year. Market pricing has followed suit, with another rate cut not expected until the Fed’s meeting in late April next year at the earliest.

Looking ahead to next week, there will be few items on the economic agenda during the holiday shortened week, but the preliminary estimate for third quarter GDP on Tuesday will be a highlight. A strong reading for annualized growth of roughly 3% is expected, which will likely be followed by a deceleration in the fourth quarter owing to the government shutdown. Nevertheless, we expect the economy to grow by 2.2% in 2026, aided by fiscal and monetary policy support.

{kind=link}