Risk sentiment softened as markets reopened after the holiday break, with investors adopting a more defensive posture. Asian equities drifted lower, and European markets struggled to gain traction at the open, reflecting subdued conviction.

One immediate dampener came from the Summary of Opinions released by the BoJ. The document reinforced that hawkish voices within the board remain firmly intact following the December rate hike. While no near-term tightening is in play, the broader message was unmistakable: the policy path still points upward. Several policymakers signaled that normalization is unfinished even after lifting the policy rate to a multi-decade high earlier this month.

A notable nuance was the absence of explicit pushback from the two Japanese government representatives present at the BoJ meeting. That silence is read as a lack of political interference from Prime Minister Sanae Takaichi, and a tacit endorsement of measured tightening if economic conditions allow.

Geopolitical risks also weighed on sentiment, with renewed focus on East Asia. China conducted extensive live-fire drills around Taiwan, involving multiple branches of its military, as Taiwan responded with troop deployments and high-profile defense demonstrations.

The drills came just days after the US announced a record USD 11.1B arms sales package to Taiwan, drawing strong protests from Beijing and warnings of “forceful measures” in response. Such exercises increasingly blur the line between routine training and preparations that could mask early stages of an attack.

In FX markets, defensive currencies outperformed. Yen led gains for the day so far, followed by Swiss Franc and Euro. At the other end, Kiwi lagged, followed by Aussie and Loonie, as risk-sensitive currencies struggled to regain footing. Dollar and Sterling traded in the middle of the pack.

In Asia, Nikkei fell -0.44%. Hong Kong HSI fell -0.71%. China Shanghai SSE rose 0.04%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield rose 0.02 to 2.061.

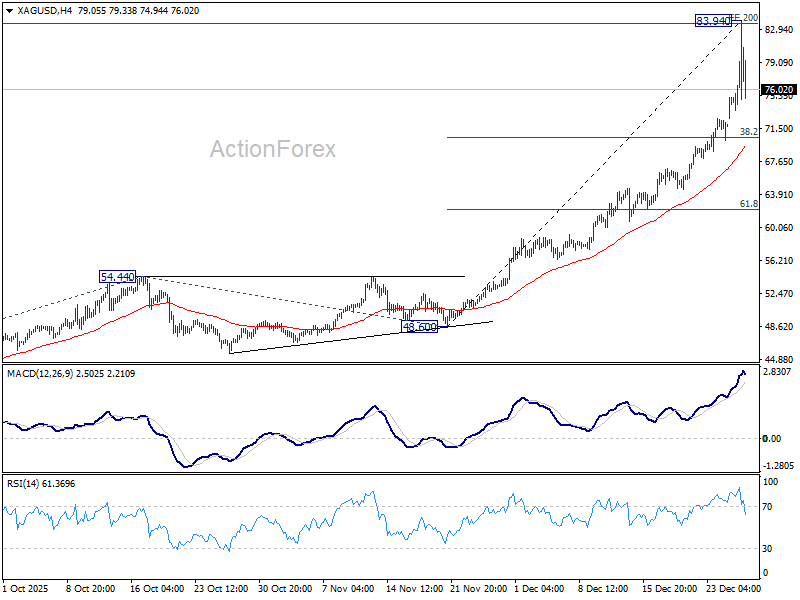

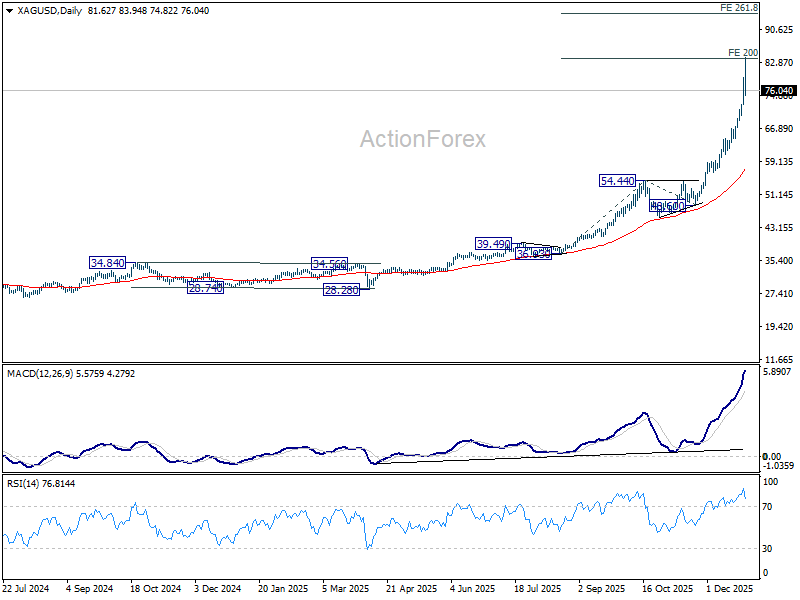

Silver pauses after strong rally, 70–84 consolidation band set

Precious metals opened the week with a sharp bout of volatility, led by a thin-market surge in Silver that briefly carried prices to fresh record highs just below 84. The rally, however, quickly lost momentum, and the retreat in both Silver and Gold suggests consolidation is now the more likely path, rather than immediate continuation. After an extended run, profit-taking has begun to surface, particularly as markets reassess near-term risk drivers.

Part of the pullback has been attributed to tentative optimism around peace discussions in Ukraine. While headlines have eased some immediate safe-haven demand, broader geopolitical risks remain firmly in play. East Asia is now a focal point after China conducted live-fire drills around Taiwan under its “Justice Mission 2025” exercises, deploying troops, warships, fighter jets, and artillery. Macro support also remains intact. Expectations for extended policy easing by the Federal Reserve in 2026, alongside persistent Dollar weakness, should limit the downside for both Gold and Silver once consolidation matures.

Technically, Silver’s upside acceleration was stronger than expected, as exaggerated by thin market. 200% projection of 36.93 to 54.44 from 48.60 at 83.52 was already met.

Considering the strength of the latest upleg and the depth of the subsequent pullback, a short term top was likely formed and some time is needed to digest to move. Hence, more sideway trading is expected in the coming days.

For now, initial support should be found at 38.2% retracement of 48.60.to 83.94 at 70.44, which is slightly above 55 4H EMA (now at 69.49) to contain downside. Range trading is expected between 70 and 84 for consolidations.

The prospect of extending the powerful up trend to 261.8% projection at 94.34 remains alive. However, firm break of 70 will indicate that it’s already in a medium term correction, instead of a near term one.

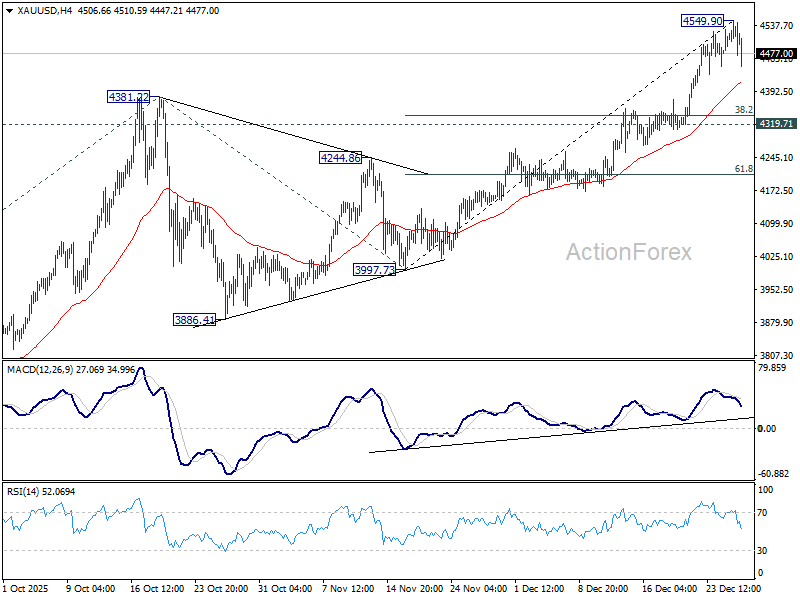

Gold has clearly underperformed Silver on the strength of latest rise. For now, some consolidations would be seen below 4549.90 high.

Firm break of 55 4H EMA (now at 4410.98) would bring deeper pullback towards 4319.71 support. But strong support is expected there to bring rebound, and set the base for extending the up trend at a later stage.

However, further break of 4319.71 will suggest that Gold is in a deeper correction towards 55 D EMA (now at 4159.42). It this happen, it would also be taken as a signal of similar deeper correction in Silver too.

BoJ opinions suggests series of hikes as neutral rate remains distant

The latest Summary of Opinions from the BoJ’s December 18–19 meeting reinforced a clear tightening bias, with many policymakers arguing that the December rate hike should not mark the end of the cycle.

One opinion noted there was “still considerable distance” to neutral levels, explicitly calling for rate hikes at “intervals of a few months”. Another linked Yen weakness and rising long-term yields partly to the policy rate being too low relative to inflation, suggesting delayed normalization risks exacerbating financial distortions.

Inflation concerns featured prominently throughout the discussion. Several members described recent price pressures as “sticky”. One opinion highlighted spring wage negotiations as a key test, arguing that a third consecutive year of target-consistent wage growth would confirm underlying inflation has reached 2%.

Still, not all voices favored an aggressive path. Some policymakers urged caution, citing uncertainty around the neutral rate and shifting global rate environments. They argued flexibility should take precedence over targeting a specific policy level.

At the meeting, the BoJ raised its policy rate to a 30-year high of 0.75%.

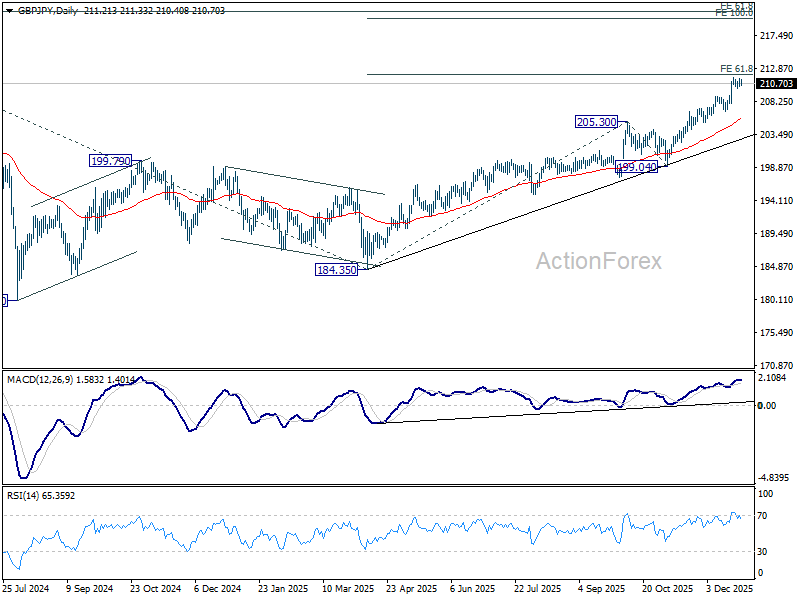

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.68; (P) 211.10; (R1) 211.79; More…

GBP/JPY dips mildly as consolidations continue below 211.57. Intraday bias stays neutral for the moment. Deeper retreat could be seen but downside should be contained above 206.74 support to bring another rally. On the upside, break of 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98 will extend current up trend to 100% projection at 219.99 next.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 199.04 support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

{kind=link}