Global markets have turned cautious again, with the mild selloff in US equities overnight that carried into Asian trading. A key trigger was pressure on US defense stocks after President Donald Trump’s said he would block dividends and stock buybacks for defense contractors unless they address concerns including executive pay and production inefficiencies

Another market headwind came from crude oil, which dipped as Trump said Venezuela’s interim authorities would transfer up to 50 million barrels of crude to the US, stoking fears of increased supply. Geopolitical tensions have also flared, with reports that the US seized two Venezuela-linked oil tankers, including one under Russia’s flag, as part of an aggressive push to control oil flows in the region.

Despite headlines, some investors are holding back judgment on the broader geopolitical impact, instead focusing on upcoming economic data. Traders are increasingly positioning for tomorrow’s US non-farm payrolls, a key release that could clarify the trajectory of the labor market and influence Fed policy expectations.

Yesterday’s ISM Services PMI showed a strong rebound in the sector at year-end, with business activity, new orders and employment all climbing. Most notably, the employment component returned to expansion for the first time since May 2025, easing concerns over labor market softening. A strong non-farm payrolls figure could bolster confidence in the US economy and make further Fed rate cuts less certain.

In currency markets, Yen is currently the strongest major currency on the week, reflecting some haven flows amid the cautious tone. Aussie sits in second place after today’s retreat, with Dollar following as third strongest overall. At the bottom of the FX leaderboard sits the Loonie, trailed by Swiss Franc and Euro. Sterling and Kiwi are positioning in the middle.

In Asia, Nikkei fell -1.63%. Hong Kong HSI fell -1.20%. China Shanghai SSE fell -0.07%. Singapore Strait Times fell -0.18%. Japan 10-year JGB yield fell -0.042 to 2.079. Overnight, DOW fell -0.94%. S&P 500 fell -0.34%. NASDAQ rose 0.16%. 10-year yield fell -0.041 to 4.138.

Swiss CPI stays subdued at 0.1% as imported prices drag

Swiss inflation remained subdued in December, with headline CPI unchanged at 0.1% yoy, in line with expectations. Core inflation edged slightly higher, ticking up from 0.4% to 0.5%, pointing to mild underlying price pressures even as overall inflation stayed close to zero.

The divergence between domestic and imported prices remained a defining feature. Prices of domestic products rose from 0.4% to 0.5% yoy, while imported goods prices fell further into negative territory, slipping from -1.3% to -1.6% yoy.

On a monthly basis, headline and core CPI were flat mom, with domestic prices up 0.2% mom and imported prices down sharply by -0.8% mom. According to the State Secretariat for Economic Affairs, offsetting price movements kept the index stable. Lower prices for international package holidays, medicines and certain vegetables were balanced by higher costs for hotels, supplementary accommodation and private transport hire.

BoJ regional report sees small firms face constraints on wage hikes

Japan’s economy continues to recover gradually across the country, according to the latest Regional Economic Report from the BoJ. The central bank maintained its assessment for all nine regions, noting that activity is either picking up or recovering at a modest pace.

The report highlighted continued wage pressure, with many firms indicating the need to raise wages in fiscal 2026 at roughly the same pace as in 2025. Strong corporate profits and a tight labour market were cited as key drivers. That said, the BoJ flagged emerging divergence beneath the surface. Some regions warned that smaller firms may struggle to match last year’s wage hikes.

Some export-oriented areas reported softness linked to “the impact of U.S. tariffs and intensifying competition from Asian companies”. Others, however, pointed to “increasing global demand mainly for artificial intelligence-related goods.”

Japan real wages fall -2.8% in November, sharpest in nearly a year

Japan’s real wages fell sharply in November, dropping -2.8% yoy, marking the 11th consecutive month of decline and the steepest fall since last January. Inflation-adjusted earnings were hit as a 3.3% rise in consumer prices more than offset a modest increase in nominal pay.

Nominal wages rose just 0.5% yoy, far below expectations of 2.3% and a sharp slowdown from October’s 2.5% pace. While nominal pay has now risen for 47 straight months, the latest reading marks the weakest growth since December 2021.

The softness was driven largely by a -17.0% drop in special earnings, mainly volatile one-off bonuses outside the usual summer and winter payment periods. More concerning for the underlying trend, regular pay growth eased from 2.4% yoy to 2.0%. Overtime pay slowed from 2.1% to 1.2%, pointing to waning momentum in private-sector income growth and continued pressure on household purchasing power.

RBA’s Hauser shrugs off CPI miss, says rate cuts still unlikely

The RBA remains biased against further near-term rate cuts, despite the softer-than-expected inflation data, according to comments from Deputy Governor Andrew Hauser. Speaking in an interview with Australian Broadcasting Corporation, Hauser said the likelihood of additional easing in the near term remains “probably very low”.

Hauser stressed that the November CPI downside surprise has not altered the central bank’s thinking. He described the data as “helpful” but said it was “largely as we expected,” adding that there was “not a lot of news” in the release from a policy perspective. Inflation remains above the RBA’s 2–3% target range, reinforcing the case for caution.

He also noted that part of the moderation in inflation reflected temporary factors such as Black Friday discounting, while cost pressures in housing-related components actually picked up. As a result, policymakers are placing greater emphasis on the upcoming quarterly inflation report due later this month.

Hauser said the RBA will assess that quarterly data in the context of the broader economy rather than reacting mechanically to a single number. While an extreme outcome would prompt deeper scrutiny, he made clear there is no simple rule linking specific inflation prints to policy move.

“We don’t have a rule that says if it’s 0.9 we hold, and if it’s 1 we raise and if it’s 0.7 we cut — we take a view of the whole economy,” Hauser emphasized.

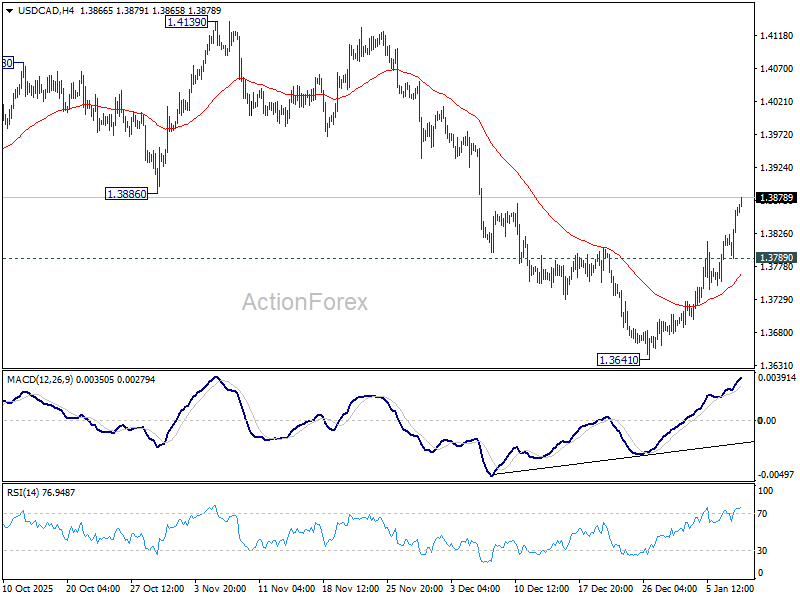

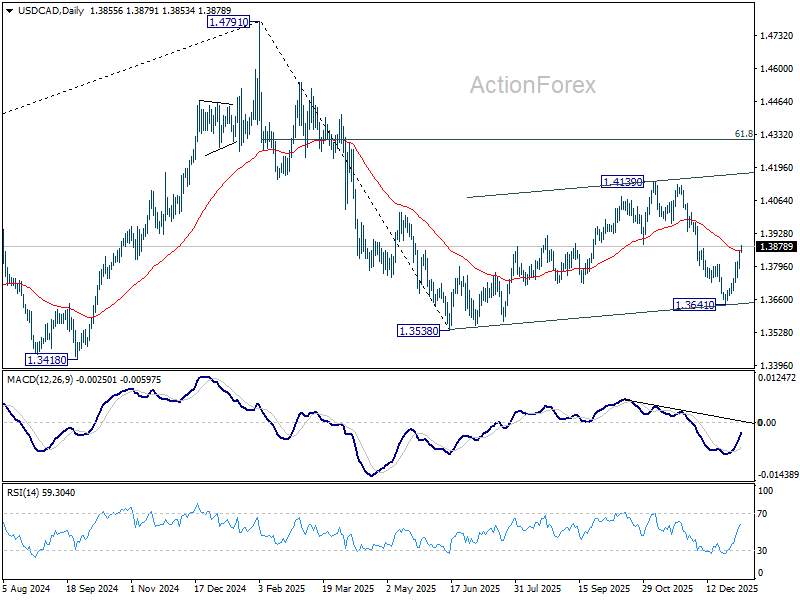

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3813; (P) 1.3838; (R1) 1.3886; More…

USD/CAD’s rally from 1.3641 continues today and intraday bias stays on the upside. Current strong momentum suggests that corrective pattern from 1.3538 is still extending, in its third leg. Sustained trading above 55 D EMA (now at 1.3859) will pave the way to 1.4139 resistance next. On the downside, below 1.3789 minor support will turn intraday bias neutral first.

In the bigger picture, 1.4791 is likely developing into a deeper, larger scale correction. In the less bearish case, it’s just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

{kind=link}