Canadian manufacturing and wholesale reports for November should reinforce that heavily trade exposed sectors are still being negatively impacted by U.S. tariffs, even as we continue to expect increases in household spending to keep overall gross domestic product growth positive.

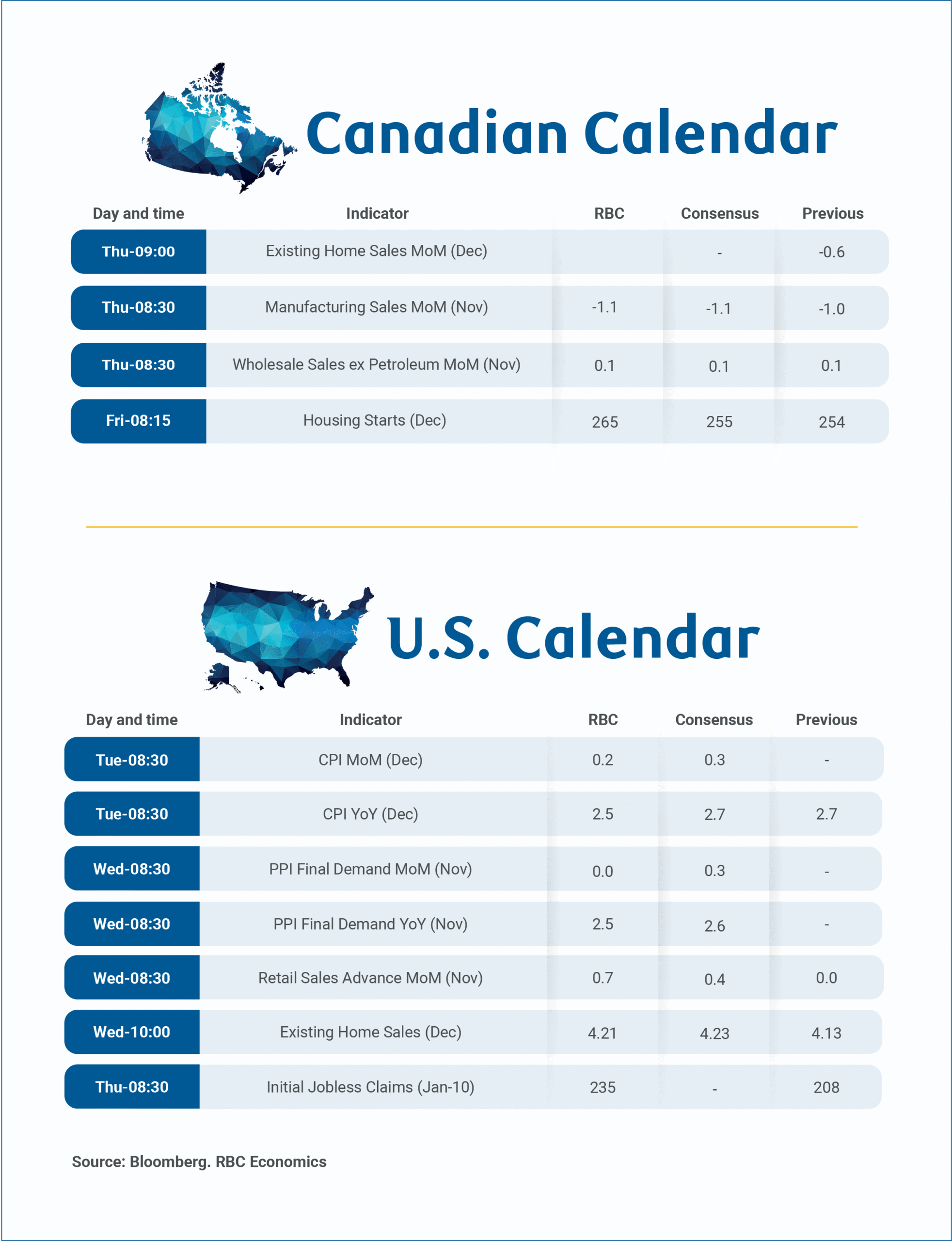

Statistics Canada’s preliminary estimates showed a 1.1% decline in manufacturing sales in November, and a 0.1% increase in wholesales. The reported drop in manufacturing sales was despite a 1% rise in output prices, implying a larger decline in sale volumes.

Much of the weakness appears to have been concentrated in the auto sector— the number of vehicles produced was down 22% from a year ago in November in separately reported data, coinciding with the imposition of new U.S. tariffs on medium and heavy-duty trucks on Nov 1. StatsCan also flagged food manufacturing as a soft spot.

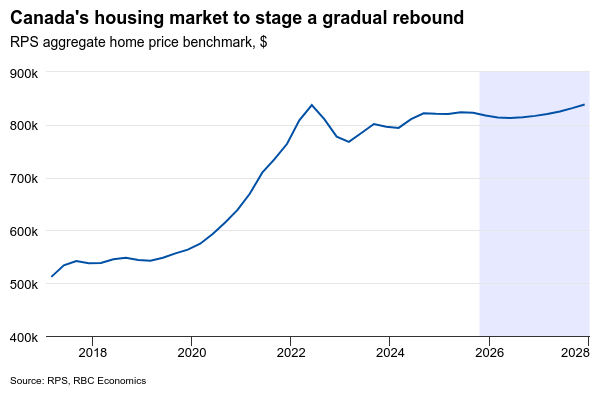

December home resale data on Thursday is expected to show a lackluster finish to 2025 as activity and prices moderated particularly in key markets like southern Ontario and B.C., where inventory is keeping buyers in a stronger negotiating position. Still, we continue to expect improvement in the Canadian economy, and the lagged impact of lower interest rates will support a gradual pick up in housing markets in 2026.

We look for housing starts on Friday to tick higher following a jump in permit issuance into October, and expect overall GDP growth to remain modestly positive in Q4 with continued growth in consumer spending. The advance estimate of retail sales showed a 1.2% increase in November.

In the U.S., we look for consumer price growth to slow on Tuesday and retail spending to remain firm on Wednesday.

2026 kicked off with a significant increase in geopolitical uncertainty, and headlines/fallout from U.S. military action in Venezuela will continue to be closely watched. The view that any significant shift in Venezuelan oil production would take many many years and would be unlikely in volume terms to meaningfully impact Canadian heavy oil production or sales to the United States. We have made no adjustments at this point to our Canadian or U.S. economic outlooks as a result.

Week ahead data watch:

December U.S. inflation data is expected to show soft core consumer price index (ex-food and energy) growth at 0.2% month-over-month, driven by persistent weakness in shelter costs, particularly rent and owners’ equivalent rent. A sharp slowing in growth in the rent components between September and November was in part due to methodology issues resulting from the government shutdown that prevented collection/release of October CPI data, but we expect underlying rent price growth has also been slowing. Food prices likely ticked higher after surprising on the downside in November but gasoline prices declined, leaving headline CPI up a similar 0.2% month-over-month and 2.5% year-over-year.

We expect U.S. retail spending remained firm in November, driven in part by a rise in prices at gasoline stations, but also higher auto sales (unit vehicles sales rose 1.7% in November). Further growth in control (ex-auto, gas, and building material) store sales also build on the 0.9% jump in October.

{kind=link}