With the economic calendar nearly empty, markets are fixated on the escalating political risk surrounding Fed Chair Jerome Powell, who is now under federal criminal investigation linked to the renovation of the Fed’s headquarters and his congressional testimony on the matter. The move has taken markets by surprise, particularly given that Powell’s term as Fed Chair is due to conclude in May. A new chair is expected to be appointed soon, with President Donald Trump widely anticipated to announce his pick later this month.

One theory in markets is that the investigation is tied to the broader political calendar, with US midterm elections in November. The administration is seen as keen to push interest rates lower as quickly as possible, and pressure on the Fed has intensified as policymakers resist aggressive easing.

Powell’s response has been unusually direct. In a blunt statement, he warned that “the threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences” of the President.

A key question now is whether this episode prompts investors to diversify away from US assets, particularly at the long end of the Treasury curve. While reactions have so far been measured, the potential for a deeper reassessment of US institutional credibility is resurfacing. That risk is starting to show in rates markets. US 10-year Treasury yields have breached the important 4.20% technical resistance zone. A sustained move above that level could open the door to a more meaningful selloff in Treasuries, especially if confidence erosion accelerates.

Under normal circumstances, rising long-end yields would be supportive for Dollar. This time, however, the currency has failed to benefit, as concerns around policy credibility and institutional independence offset the usual rate-supportive dynamics.

Gold has been the clear beneficiary of this environment, surging to fresh record highs as investors seek insulation from political and institutional uncertainty. Attention is also turning to whether Euro could attract renewed inflows as the only viable liquid alternative to Dollar should confidence in US assets deteriorate further.

In FX markets so far, Dollar sits at the bottom of the performance table, followed by Yen and Loonie. Yen remains pressured as markets bet Japan could call a snap election to capitalize on Prime Minister Sanae Takaichi’s strong popularity and pursue fiscal expansion, and thus lifts domestic risk appetite. Kiwi leads gains, followed by Swiss Franc and Sterling, with Euro and Aussie trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.50%. CAC is up 0.02%. UK 10-year yield is up 0.02 at 4.398. Germany 10-year yield is down -0.017 at 2.851. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 1.44%. China Shanghai SSE rose 1.09%. Singapore Strait Times rose 0.47%.

Eurozone Sentix jumps to six-month high, recovery optimism builds

Eurozone investor confidence improved at the start of the year, with Sentix Investor Confidence Index rising from -6.2 to -1.8 in January, well above expectations of -5.1 and the strongest reading since July. The rebound was broad-based, with the Current Situation Index climbing from -16.5 to -13.0 and the Expectations Index jumping from 4.8 to 10.0, both also six-month highs.

Sentix noted that the improvement reflects a narrowing gap between professional and private investors. While institutional investors had already turned more optimistic in recent months, private investors had remained sceptical. That dynamic is now shifting, with private investors beginning to join the recovery narrative, even though differences in outlook between the two groups remain historically large.

Inflation concerns are also easing at the margin. Sentix’s Inflation Barometer shows expectations for slightly softer price pressures, helping to reduce stress on bond markets. However, Sentix cautioned against assuming renewed central bank support, warning that as the recovery takes hold, ECB policymakers are “unlikely to feel much incentive to act”.

EUR/USD Mid-Day Outlook

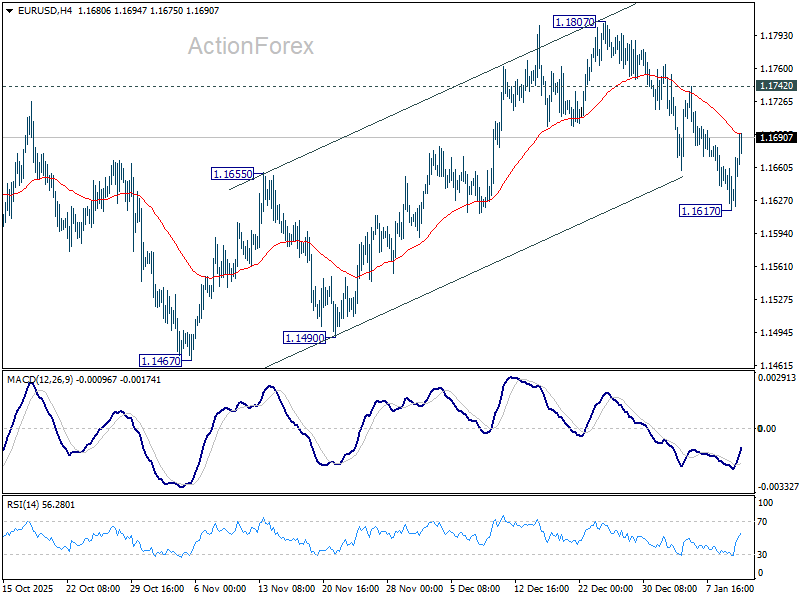

Daily Pivots: (S1) 1.1615; (P) 1.1639; (R1) 1.1661; More….

Intraday bias in EUR/USD stays neutral at this point. On the upside break of 1.1742 resistance will argue that pullback from 1.1807 has completed. Rise from 1.1467 should then be ready to resume. Further break of 1.1807 will pave the way to retest 1.1817 high. Nevertheless, on the downside, below 1.1617 will target 1.1467 support. Overall, price actions from 1.1917 are seen as a corrective pattern that might extend further.

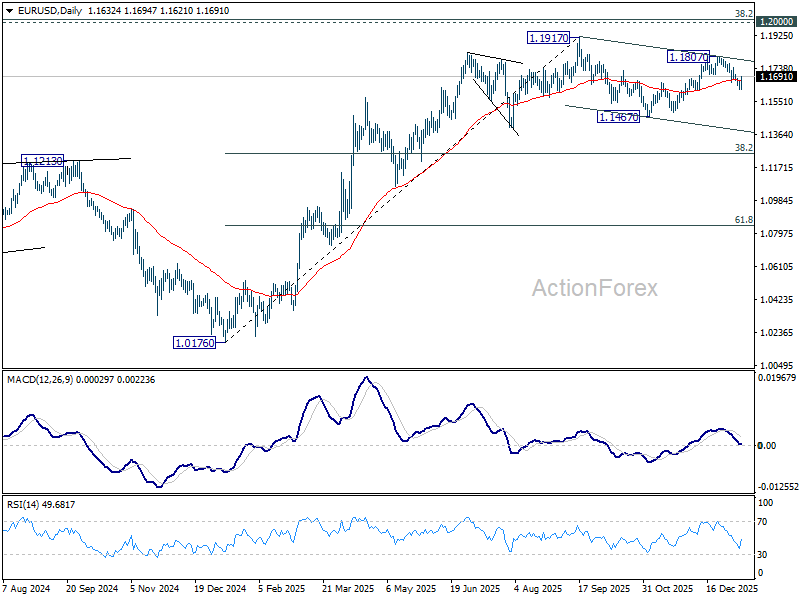

In the bigger picture, as long as 55 W EMA (now at 1.1416) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}