Dollar climbed sharply in early US session as markets continued to pare back bets on a Fed rate cut in Q1 2026, a move driven by stronger-than-expected labor market data. Initial jobless claims fell back below the psychological 200k mark, countering dovish concerns about extended labor-market deterioration.

Odds of a March rate cut have collapsed further to below 22%. Also, markets now see roughly a two-in-three chance that a rate cut will occur by the end of the first half — down sharply from near 80% just a week ago. The first easing move might come only after a leadership transition at the Fed.

Across FX markets today so far, Dollar is the best performer, followed by Aussie and Loonie. Sterling is struggling the most amid benign UK data that hasn’t materially lifted the Pound, with Euro and Swiss Franc also lagging. Yen and Kiwi sit in the middle of the performance table.

Elsewhere in commodities, oil prices tumbled from multi-month highs after US President Donald Trump’s remarks eased fears of imminent US military action against Iran, a catalyst that had recently underpinned energy markets. Adding to the supply picture, Venezuelan crude shipments have resumed. That supply increase is seen contributing to the sentiment that near-term oversupply risks would outweigh geopolitical pressures, keeping a lid on prices.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.02%. CAC is down -0.18%. UK 10-year yield is up 0.036 at 4.38. Germany 10-year is up 0.011 at 2.829. Earlier in Asia, Nikkei fell -0.42%. Hong Kong HSI fell -0.28%. China Shanghai SSE fell -0.33%. Singapore Strait Times rose 0.43%. Japan 10-year JGB yield fell -0.017 to 2.169.

US initial jobless claims fall to 198k, signal little labor market stress

US labor market conditions showed renewed firmness, with initial jobless claims falling more than expected in the latest week. Claims dropped by -9k to 198k in the week ending January 10, below expectations of 208k and marking one of the lowest readings of the past year.

The four-week moving average of initial claims declined by -6.5k to 205k, the lowest level since January 20, 2024. The smoothing measure confirms that layoffs remain limited, with little evidence of sustained deterioration in hiring conditions.

Continuing claims also edged lower, falling 19k to 1.884 million in the week ending January 3. The four-week average was broadly unchanged at 1.889 million.

Eurozone exports fall -3.4% yoy in Nov, EU down -4.4%, external demand drags

Eurozone trade data for November pointed to weakening external demand, even as the bloc maintained a modest surplus. Goods exports fell -3.4% yoy to EUR 240.2B, while imports declined -1.3% to EUR 230.3B, leaving a trade surplus of EUR 9.9B. The resilience came from within the bloc. Intra-Eurozone trade rose 0.8% yoy to EUR 220.9B, partially offsetting softness in extra-Eurozone flows.

At the broader EU level, goods exports dropped -4.4% yoy to EUR 213.8B and imports fell -2.9% to EUR 205.7B, resulting in a EUR 8.1B trade surplus.

By trading partner, exports to the US fell sharply by -20.3% year-on-year, while shipments to the UK declined -6.0%. Trade with China was broadly stable, with exports down just -1.2% despite stronger imports, keeping the bilateral deficit large. Switzerland stood out as a relative bright spot, with EU exports rising 6.7%.

Eurozone industrial output rises 0.7% mom in November, led by capital goods

Eurozone industrial production rose 0.7% mom in November, outperforming expectations for a 0.5% gain. The gains, however, were uneven across categories.

Capital goods output jumped 2.8%, providing the main lift, while intermediate goods rose a modest 0.3%. By contrast, energy production fell sharply by -2.2%, while durable and non-durable consumer goods declined -1.3% and -0.6% respectively, pointing to still-soft consumer demand.

Across the wider EU, industrial production increased just 0.2% on the month. Estonia (6.0%), Lithuania (5.8%), and Czechia (2.8%) recorded the strongest gains, while Luxembourg (-7.3%), Denmark (-5.1%), and Portugal (-3.0%) posted the steepest declines.

UK GDP beats with 0.3% mom growth in November, services lead

UK economic output surprised to the upside in November, offering a modest boost to the growth outlook late in the year. GDP rose 0.3% mom, beating expectations for flat growth, with strength concentrated in services and production.

Services output increased 0.3% mom, while production jumped 1.1% mom, offsetting a sharp -1.3% mom decline in construction activity. The data points to improving momentum in consumer- and business-facing sectors, even as construction continues to struggle.

Over the three months to November, GDP edged up 0.1%. Services grew 0.2%, while production slipped -0.1% due largely to weaker motor vehicle manufacturing, and construction fell -1.1%. On a year-on-year basis, GDP expanded 1.3%, led by services growth of 1.4%. Production rose 0.4% and construction rose 0.7%.

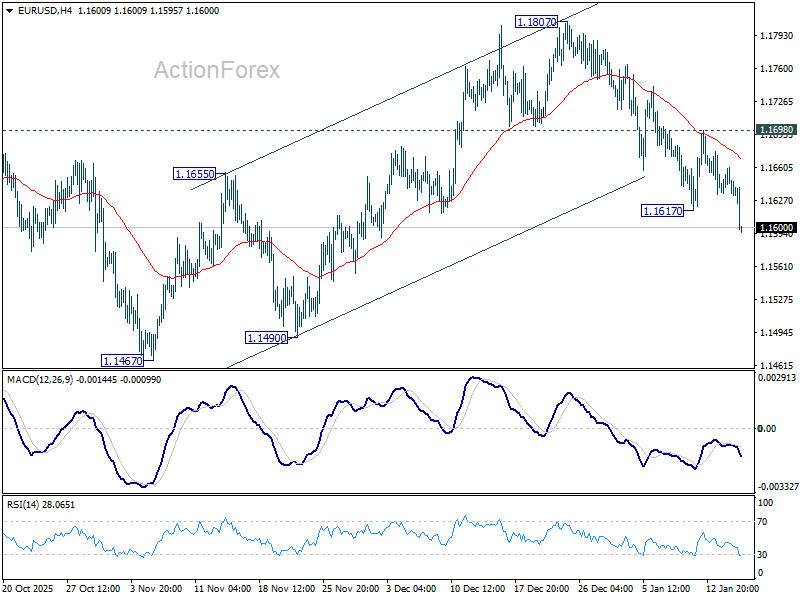

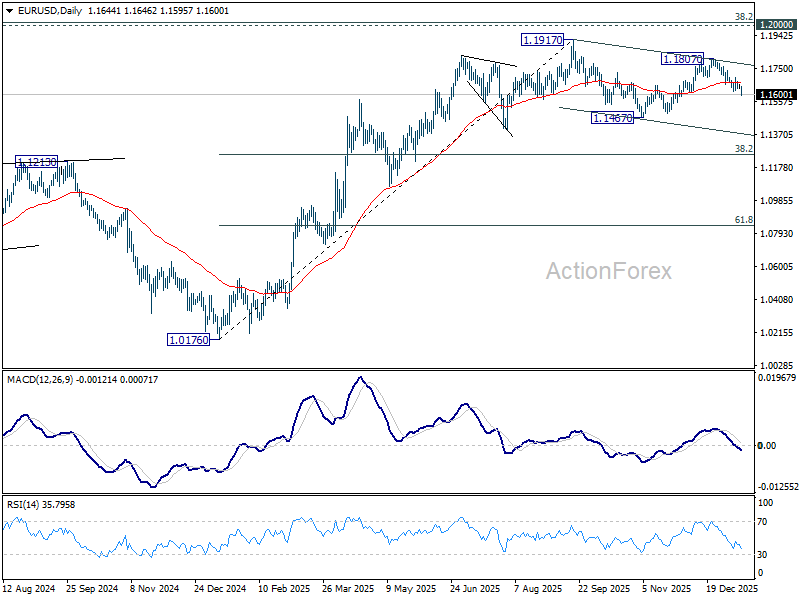

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1633; (P) 1.1648; (R1) 1.1659; More….

EUR/USD’s fall from 1.1807 resumed by breaking through 1.1617 temporary low and intraday bias is back on the downside. Current development revived the case that corrective pattern from 1.1917 is already in its third leg. Deeper fall would be seen to 1.1467 support and below. Risk will now stay on the downside as long as 1.1698 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 1.1416) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}