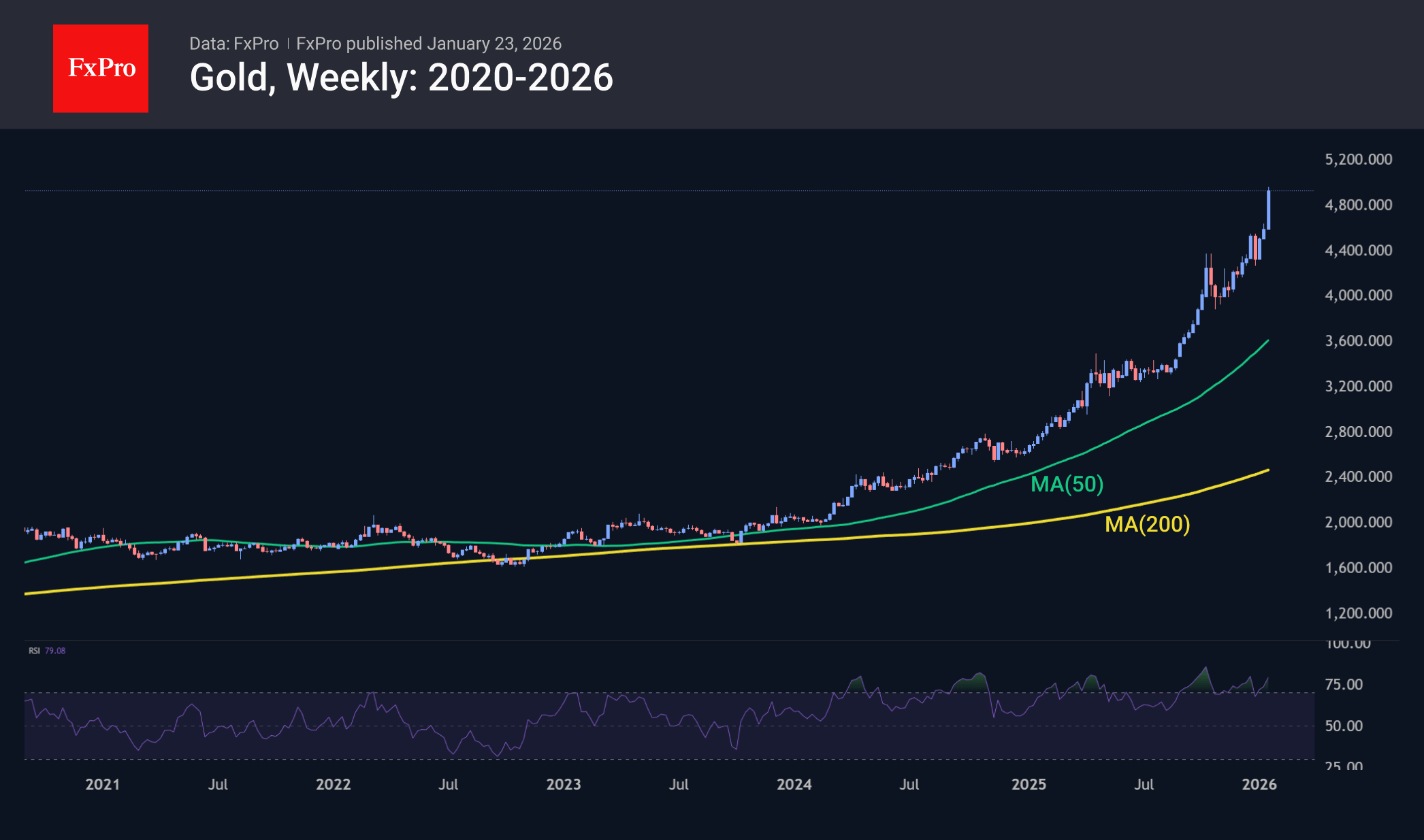

Gaining nearly 7% since Monday, gold is recording its strongest nominal growth in history and one of its most powerful weeks in terms of momentum. Gold is now within striking distance of the psychologically important $5,000 per ounce mark, which was unthinkable just a couple of years ago when the market was resting at $2,000.

The rally is driven by geopolitics, fiscal problems, the associated debasement trade, lower rates and capital outflows from other markets. When the Fed began tightening monetary policy in 2022, money market fund holdings stood at $5.5 trillion. By the end of 2025, they had increased to $7.7 trillion. As interest rates fall, money will flow into other assets. But to where? Stocks are fundamentally overbought, and Bitcoin has fallen out of favour due to declining volatility. Precious metals, on the other hand, are shining.

So, Goldman Sachs’ upward revision of its gold forecast for the end of 2026 from $4,900 to $5,400 seems logical. The bank expects a 50-basis-point cut in the federal funds rate and points to a 500-tonne increase in precious metal-focused ETF holdings since the beginning of 2025.

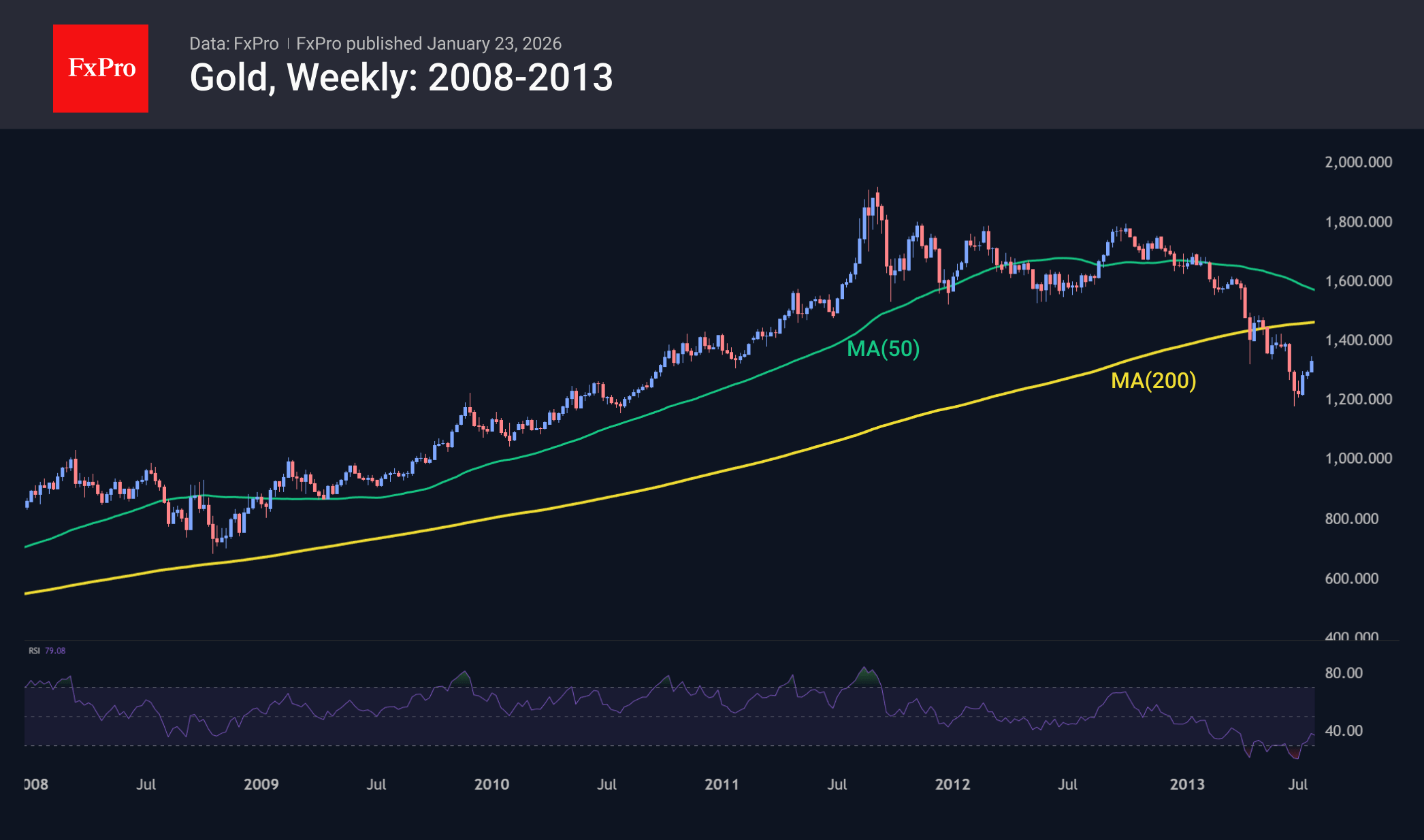

On the other hand, such an explosion of volatility after a prolonged rise is often the last impulse before a global reversal. The problem is understanding exactly when the turning point will occur. The current growth of more than 25% over the past 11 weeks is comparable to what happened at the end of the rally in 2011, and this week’s growth dynamics are similar to what happened during the last week of sharp growth a decade and a half ago. But history also teaches us patience: gold cautiously retested its highs for another three weeks, even though the downward slumps were becoming increasingly fierce. We may see something similar this time around.

{kind=link}