Market reaction to the Fed’s widely expected rate hold was muted overnight, with equities struggling to find direction. S&P 500 briefly pushed above the 7,000 mark, but the move lacked follow-through. By the close, all three major US indexes finished near flat.

Away from equities, two developments stood out. US Treasury yields moved higher, with the 10-year yield closing back above 4.25%, hinting at renewed pressure on the long end rather than any rush into safety. At the same time, the rally in precious metals extended. Gold surged to another record above 5,500, while Silver pressed through the 120 level.

Taken together, the moves suggest markets have quickly returned to a familiar rhythm following what was largely a non-eventful FOMC decision.

The most notable takeaway from Jerome Powell’s press conference was not economic guidance, but his repeated emphasis on keeping the Fed insulated from political influence amid rising pressure from the Trump administration to cut rates.

“Stay out of elected politics, don’t get pulled into elected politics,” Powell said, stressing that independence remains central to the Fed’s credibility. He was careful, however, to distinguish independence from disengagement.

Powell emphasized that accountability runs through Congress, describing engagement with lawmakers as an “affirmative regular obligation.” He argued that democratic legitimacy is earned through oversight and transparency, not through alignment with political agendas.

When pressed repeatedly on a Justice Department probe into cost overruns for the Fed’s headquarters renovation and on whether he plans to stay after his term ends, Powell declined to engage. “There’s a time and place for these questions,” he said, repeatedly signaling boundaries.

In FX markets, Dollar remains the worst performer of the week, with selling pressure returning after the Fed. Euro follows as the second weakest, with Loonie next. Aussie leads, supported by firm inflation data and tightening expectations, followed by Kiwi and Swiss Franc. Yen and Sterling now sit in the middle of the performance table.

NZ ANZ business confidence eases to 64.1, pricing signals turn hotter

New Zealand’s ANZ Business Confidence eased in January, slipping from a 30-year high of 73.6 to 64.1. While the decline looks notable, confidence remains at a very strong level historically. The own activity outlook also moderated, falling from 60.9 to 51.6, pointing to some loss of momentum after December’s surge. According to ANZ, the coming months will be key in determining whether growing talk of rate hikes begins to weigh on activity.

The more important signal came from inflation indicators, which moved decisively higher. The net share of firms expecting to raise prices in the next three months rose 5 points to 57%, the highest reading since March 2023. Firms also expect to raise prices by 2.1%, up from 1.8%, marking the fastest pace in two years. Wage pressures are beginning to lift modestly, while inflation expectations reached their %, highest level in 15 months.

ANZ described the results as a mix of “good news and bad news,” warning that the inflation signals are not consistent with forecasts from either the bank or the RBNZ. Explanations include faster margin recovery or less spare capacity than assumed. ANZ still forecasts the first OCR hike in December, but cautioned that if pricing intentions show up in hard data, tightening could come earlier.

New Zealand exports and imports jump 15% yoy in December

New Zealand recorded a modest but better-than-expected trade surplus of NZD 52m in December, exceeding forecasts for a NZD 40m surplus. According to Stats NZ, goods exports jumped 15% year-on-year to NZD 7.7B, while goods imports rose by a similar 15% to NZD 7.6B, reflecting strong two-way trade flows at year-end.

Export growth was broad-based across key trading partners. Shipments to Australia rose NZD 204m (26% yoy), while exports to the EU increased NZD 120m (31%). Exports to China, New Zealand’s largest market, grew a more modest 4.6%, while gains were also recorded to the US (4.8%) and Japan (15%).

On the import side, increases were led by China, with imports up NZD 381m (27% yoy), followed by the EU (26%) and Australia (27%). In contrast, imports from the US fell -16% yoy, offering some offset to the overall rise.

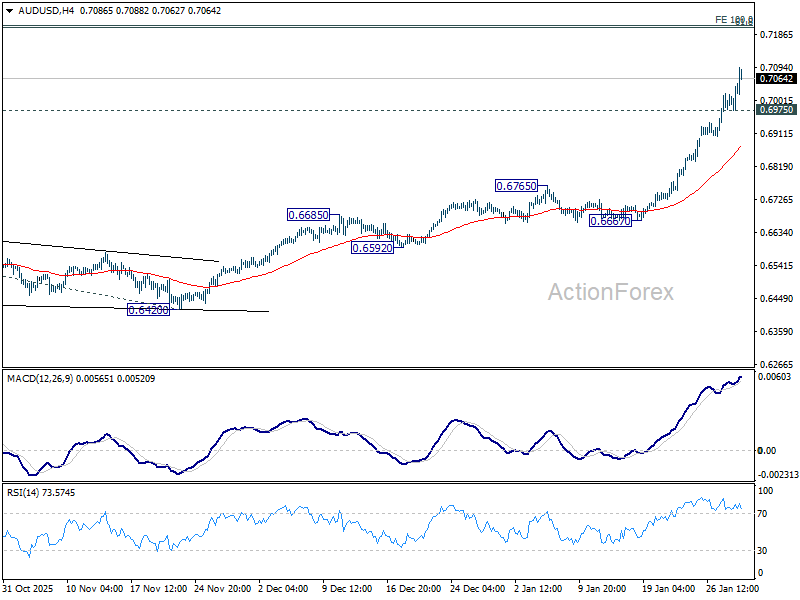

AUD/USD Daily Report

Daily Pivots: (S1) 0.6998; (P) 0.7021; (R1) 0.7064; More...

AUD/USD’s rally continues today and intraday bias stays on the upside. Current up trend should target 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. On the downside, below 0.6975 minor support will turn intraday bias neutral and bring consolidations. Downside of retreat should be contained above 0.6765 resistance turned support to bring another rally.

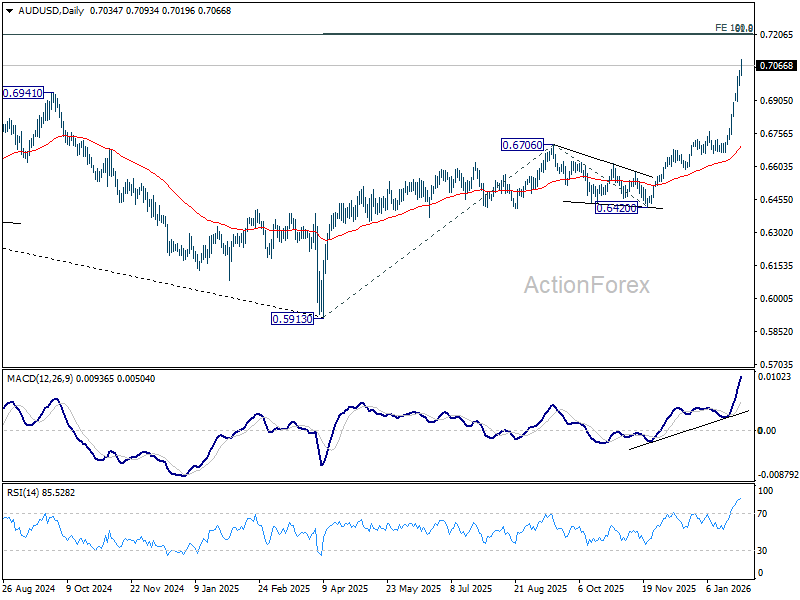

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

{kind=link}