- US NFP and CPI data awaited after Warsh’s nomination as Fed chief.

- Yen traders lock gaze on Sunday’s snap election.

- UK and Eurozone Q4 GDP data also on the agenda.

- China CPI and PPI could reveal more weakness in domestic demand.

Dollar recovers on Warsh nomination, upbeat ISM mfg PMI

The US dollar has entered a recovery mode and managed to outperform all its major peers this week, mainly driven by the nomination of former Fed Governor Kevin Warsh as the new Fed Chair. During his term, between 2006 and 2011, Warsh was concerned about inflation and was against balance sheet expansion, and that’s why investors were surprised by Trump’s choice.

Having said that though, Trump is obsessed with aggressive rate cuts and Warsh may have shown signs of a different approach this time. In any case, with the ISM manufacturing PMI surprising to the upside, the prices subindex of the services report rising as well, but the ADP private employment report revealing less-than-expected jobs growth for January, investors remained convinced that the Fed may need to proceed with two quarter-point rate cuts this year.

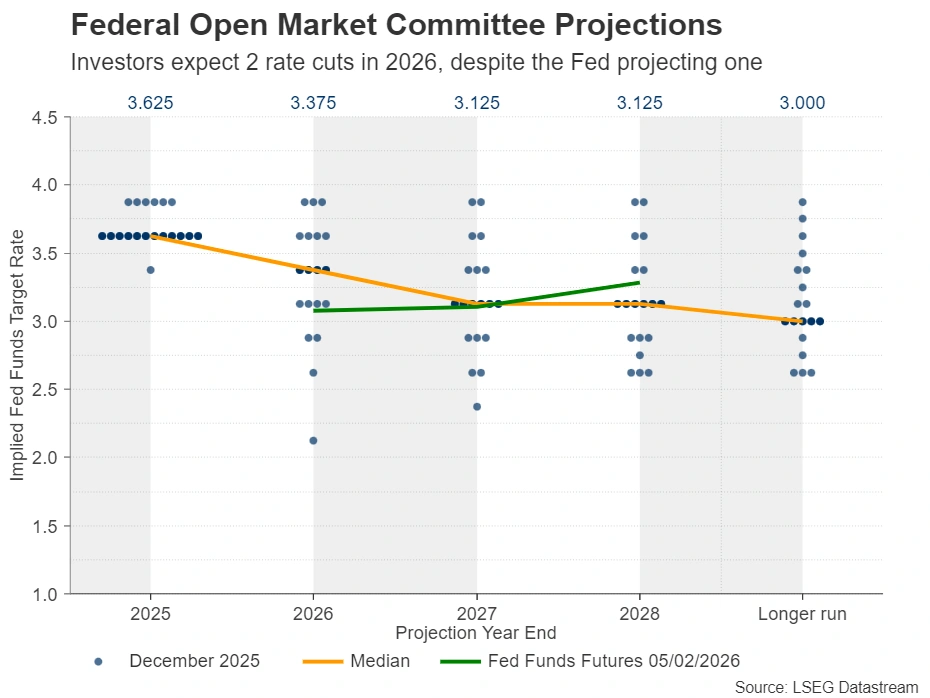

NFP and CPI on tap amid bets of two Fed cuts in 2026

With that in mind, next week, the spotlight is likely to turn to the rescheduled NFP report on Wednesday, and Friday’s CPI data, both for January. Nonfarm payrolls are expected to have accelerated to 68k from 50k, while the unemployment rate is forecast to have held steady at 4.4%. However, taking into account that private payrolls are expected to have increased to 70k from 37k, but the ADP report revealed only a mere 22k job gains in the private sector, the risks surrounding the NFP print may be tilted to the downside. The slide in the employment subcomponent of the ISM services PMI is adding extra credence to that view.

A report contrasting Fed Chair Powell’s view that the downside risks to the labor market are diminishing could prompt investors to add to their rate cut bets and thereby bring the US dollar under some selling pressure.

However, whether the slide will be sustained or not will likely depend on Friday’s CPI data. The headline rate held steady at 2.7% in December, decently above the Fed’s objective of 2%, and with the prices subindices of both the ISM manufacturing and services PMIs suggesting accelerating inflation, the risks of the CPIs may be tilted to the upside. Thus, should the CPI data reveal further stickiness in consumer prices, the US dollar is very likely to reverse and recover at least a portion of any NFP-related losses.

The US retail sales will be released on Tuesday, ahead of both the NFP and CPI reports.

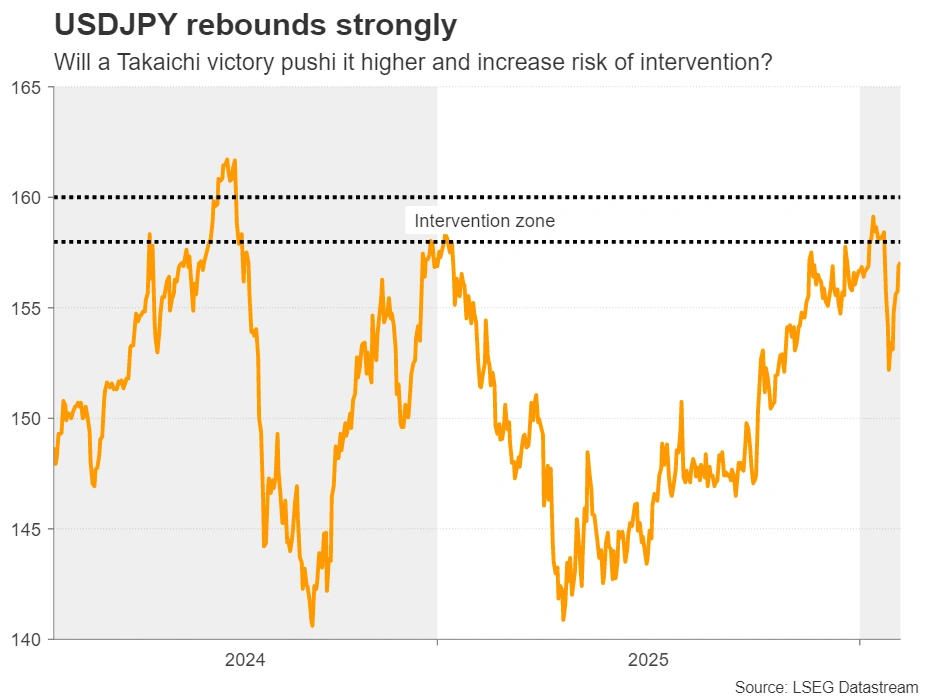

Will a Takaichi win take Dollar/Yen back to the 160.00 area?

The dollar gained the most ground against the yen, which came under pressure after Japan’s PM Takaichi talked about the benefits of a weaker yen. The Japanese currency has staged a stellar recovery following concerns about a coordinated US-Japan intervention, with dollar/yen falling from around 159.00 to 152.00, before rebounding on Takaichi’s remarks back above the 157.00 zone.

Now yen traders will likely lock their gaze on Japan’s snap election on Sunday. Takaichi called for elections in an attempt to strengthen her hand in parliament and thereby be able to proceed more easily with her fiscal plans.

During the first month of the year, polls showed a drop in popularity of the new prime minister with only one of them pointing to a more-than-70% support compared to three in December. However, the remaining showed a still strong 60%.

Thus, should the current coalition confirm expectations of a landslide, the yen could give back more of its intervention-related gains, on speculation of large spending and bigger pressure on the BoJ to proceed more slowly with future interest rate hikes. That said, should dollar/yen approach the 160.00 zone again, intervention warnings or new rate checks could be possible, limiting further advances.

On the contrary, if Takaichi’s coalition does not secure a majority, the yen could strengthen as she pledged to step down. Political uncertainty could weigh on Japan’s stock market, and the yen could eventually attract safe-haven flows, supported by expectations of a less expansionary fiscal policy and a more hawkish BoJ stance down the road, even if there is an initial delay until a new governing coalition is formed.

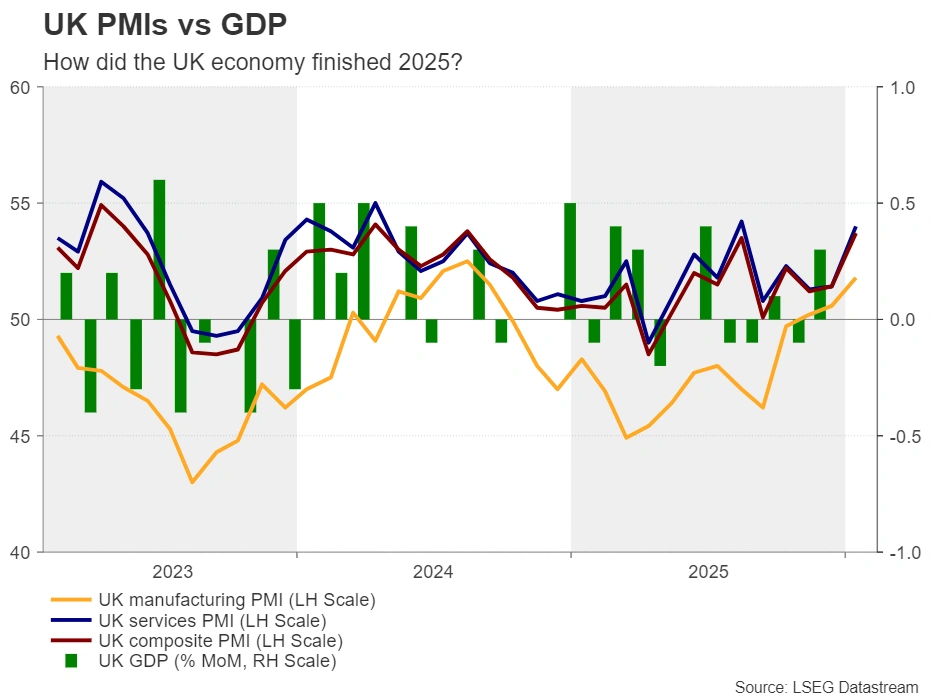

As BoE rate cut chances grow, GDP data enter the spotlight

From the UK, the first estimate of Q4 GDP will be released, alongside the monthly GDP print for December and the industrial and manufacturing production rates for the same month.

On Thursday, the Bank of England kept interest rates untouched at 3.75%, but the voting pattern revealed that the decision was a close call. Four members voted for a rate cut and five for no action, which means that only one official is needed to change his/her mind at one of the upcoming meetings for a rate cut to be delivered.

Officials remained willing to further reduce interest rates, with Governor Bailey noting that disinflation is on track and ahead of schedule, which allows scope for some further easing if the outlook evolves in line with the Bank’s projections.

This prompted investors to add to their rate cut bets, assigning a nearly 50% chance of a rate cut at the upcoming decision on March 19. By the end of the year, they expect two rate cuts, similar to the Fed.

Thus, with the economy slowing down and the third quarter of 2025 undergoing sluggish growth, another round of soft data for Q4 could increase the chances of a March rate cut, pushing the British pound lower. However, it is worth mentioning that the improvement in the PMI data during the last three months of the year compared to Q3, is tilting the risks to the upside. The further PMI increases in January point to a healthier start of the new year.

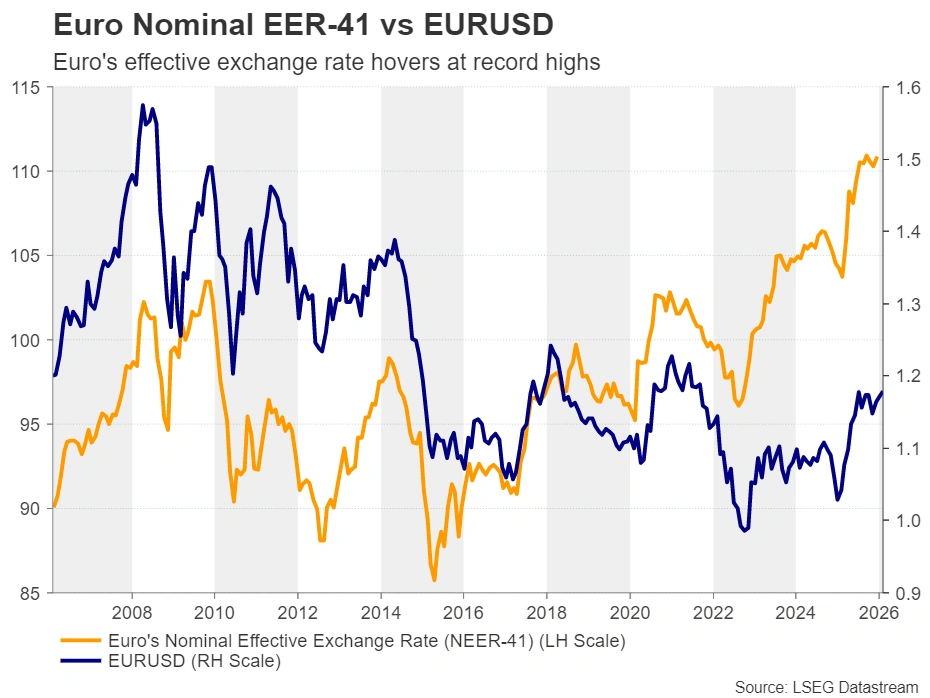

EZ GDP on tap amid comments about strong Euro

Euro traders will also have to digest preliminary GDP data for Q4, due to be released on Friday. The ECB also kept interest rates unchanged on Thursday, providing little new information in the accompanying statement. President Lagarde expressed once again the view that the Eurozone economy is doing well but added that a stronger euro could bring inflation down beyond current expectations. On Friday, ECB policymaker Kazaks said that a material strengthening of the currency could trigger a monetary policy response.

Thus, a GDP data set pointing to some weakness during the last quarter of 2025 could enhance concerns that the strong currency may have hurt the economy even more at the turn of the year, and although market participants are not assigning any meaningful chance of a rate cut down the road, they may start considering it.

China CPI and PPI data also on the agenda

Elsewhere, China’s CPI and PPI data for January are due to be released during Wednesday’s Asian session. The world’s second largest economy grew 5.0% in 2025, driven by the nation’s effort to achieve record exports to the rest of the world, which led to a record trade surplus.

However, weakness in the domestic parts of the economy persisted, with retail sales growing only 3.7% and property investment dropping by 17.2%. Although the CPI entered into positive territory in October and accelerated in November and December, the headline PPI rate has been in negative territory since November 2022. Perhaps manufacturers are keeping prices low to stay competitive amidst US President Trump’s tariffs. That said, further deflationary prints could raise concerns about the profitability of such firms and thereby their contribution to the broader economy.

In such a case, the aussie could pull back a bit, but with the RBA turning more hawkish than other major central banks, and actually raising interest rates this week, any retreat in aussie/dollar may be limited and short-lived, especially if the greenback comes under pressure due to potentially weak nonfarm payrolls.

{kind=link}