February’s Labour Force Survey for Canada next Friday, alongside January’s international merchandise trade report on Thursday will be in focus to assess whether the economy started 2026 on a solid footing.

We expect employment to increase by 10,000 in February, while the unemployment rate edges higher to 6.7% from 6.5% in January—reflecting a partial retracement in the labour force participation rate after an unusually large January decline.

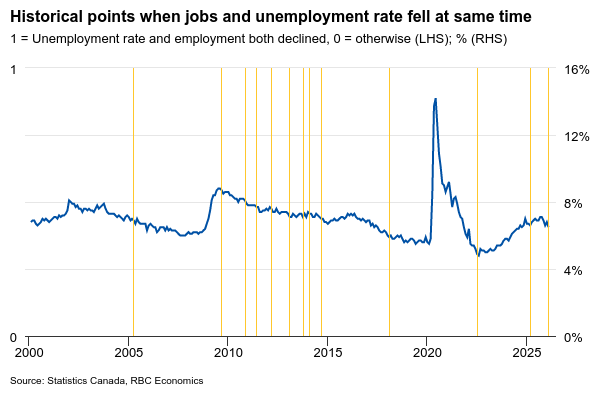

The sharp drop in the unemployment rate in January (from 6.8% in December) came despite a 25,000 drop in jobs. The labour force posted a 119,000 drop—driven by further slowing in population growth, but also the largest drop in the labour force participation rate (-0.4 ppts) since a pandemic lockdown in January 2022.

The combination of falling employment and unemployment rate at the same time sounds unusual, but Labour Force Survey data is notoriously volatile and historically, it’s not so uncommon to see that dynamic in any one given month.

Since 2000, there have been 13 months were employment and the unemployment rate declined at the same time (about once every two years). Importantly, all of those came during periods of stable to improving labour markets, not during slowdowns.

Still, an unprecedented slowing in Canada’s population from caps on temporary resident arrivals means this combination could happen more often with a shrinking labour force lowering the pace of job growth needed to push unemployment lower.

The increase in the unemployment rate we expect in February would only partially reverse the prior decline, and leave a gradual downtrend from a recent peak of 7.1% in September intact.

Wage growth will also be closely watched for signs of continued easing in pay increases. Average hourly wage growth year-over-year has been declining, consistent with most survey results.

Easing trade in January

Canada’s January merchandise trade balance on Thursday is expected to show exports and imports slowed following stronger readings late last year.

Energy prices surged in January, which likely drove much of the movement in the trade balance given Canada’s role as a major energy exporter. At the same time, motor vehicle production appears to have softened early in the year, consistent with signals from Statistics Canada’s advance manufacturing indicators, although a jump in December production could see exports rising with a lag in January.

Data summary:

February U.S. inflation report due next week will provide additional context for North American price trends. We expect headline inflation to come in at 0.3% month-over-month, which will push the year-over-year rate slightly higher to 2.5%. Core inflation growth is expected to remain unchanged from the prior month at 2.5% year-over-year and 0.3% month-over-month.

{kind=link}