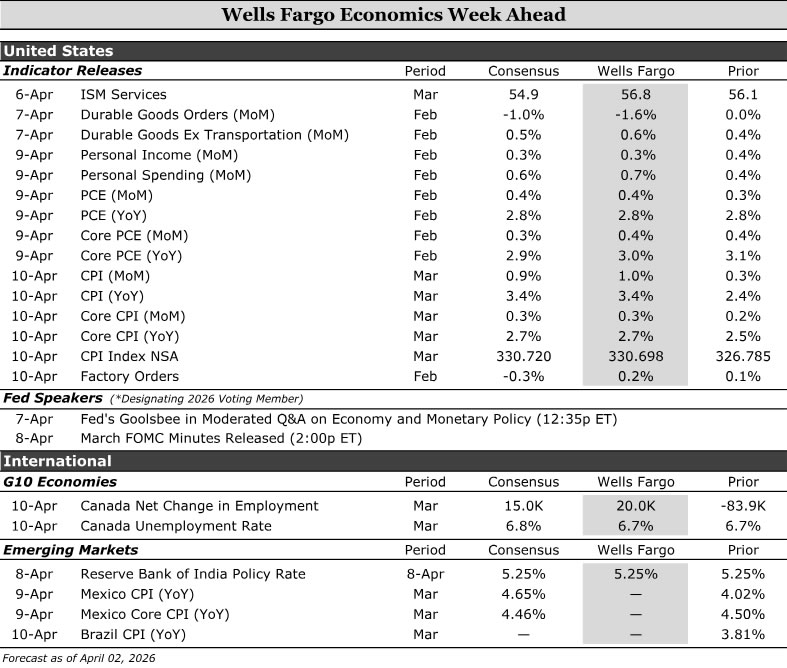

United States:

- Personal Income & Spending (Thursday), Consumer Price Index (CPI) (Friday)

G10 Economies:

- Canada Labor Force Survey (Friday)

Emerging Markets:

- Reserve Bank of India (Wednesday), Mexico CPI (Thursday), Brazil CPI (Friday)

U.S. Week Ahead

Personal Income & Spending • Thursday

U.S. economic data remain somewhat stale due to the lingering effects of last year’s prolonged federal government shutdown. The upcoming Personal Income & Spending report is a case in point, with next week’s release covering February activity—already about a month old. That lag feels more consequential amid ongoing tensions with Iran. High‑frequency credit‑card data through March suggest consumers remain resilient for now, but the risk of a slowdown grows the longer uncertainty persists, particularly if gasoline prices continue to climb sharply.

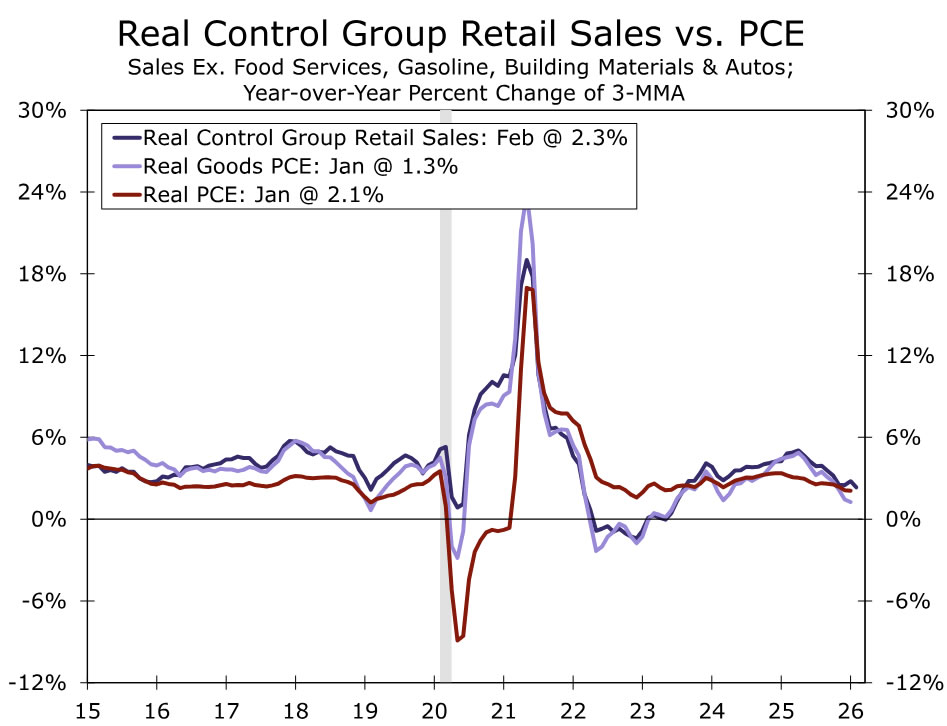

Looking at February, we expect personal spending to rise 0.7%. Solid retail sales—up 0.6% on the month, with the control group advancing 0.5%—point to healthy goods demand (chart), while firmer restaurant spending indicates continued momentum in services. That said, much of the nominal strength reflects higher prices. We expect the PCE deflator increased 0.4%, implying real spending rose a still‑solid but more modest 0.3%. We forecast personal income to increase 0.3%, reflecting some normalization after January’s boost from the Social Security cost‑of‑living adjustment.

Consumer Price Index (CPI) • Friday

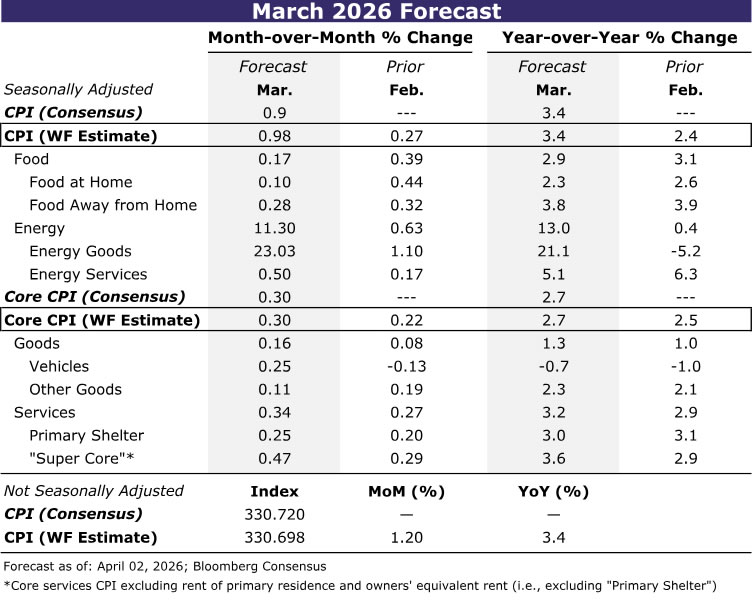

The March CPI report will put an abrupt end to the gradual disinflationary trend in place over the past two years. We estimate consumer prices rose 1.0% in March, leading to a year-over-year increase of 3.4% (table). Unsurprisingly, energy goods—largely gasoline—will account for the lion’s share (~70 bps) of March’s monthly increase as higher oil prices have quickly fed through to prices at the pump. Airline fares are expected to be another source of strength in March and drive public transportation prices up 7%, although we expect the recent surge in jet fuel to lead to an even larger rise in airfares in April.

We do not expect to see the effects of the Middle East conflict immediately feeding into other categories of inflation, however. Despite higher prices for LNG exports, domestic natural gas prices have been little changed, which should limit near-term energy services inflation. Meantime, food at home is likely to moderate in March thanks to giveback in the volatile fruits & vegetable component.

Within the core, we look for a modest strengthening in goods primarily due to a rebound in used auto prices. Core services is likely to match the 0.3% gain registered in February, as the expected jump in airline fares is largely offset by mean-reversion in medical care services and further softness in motor vehicle insurance. We anticipate primary shelter rose 0.25%, roughly in-line with its three-month average.

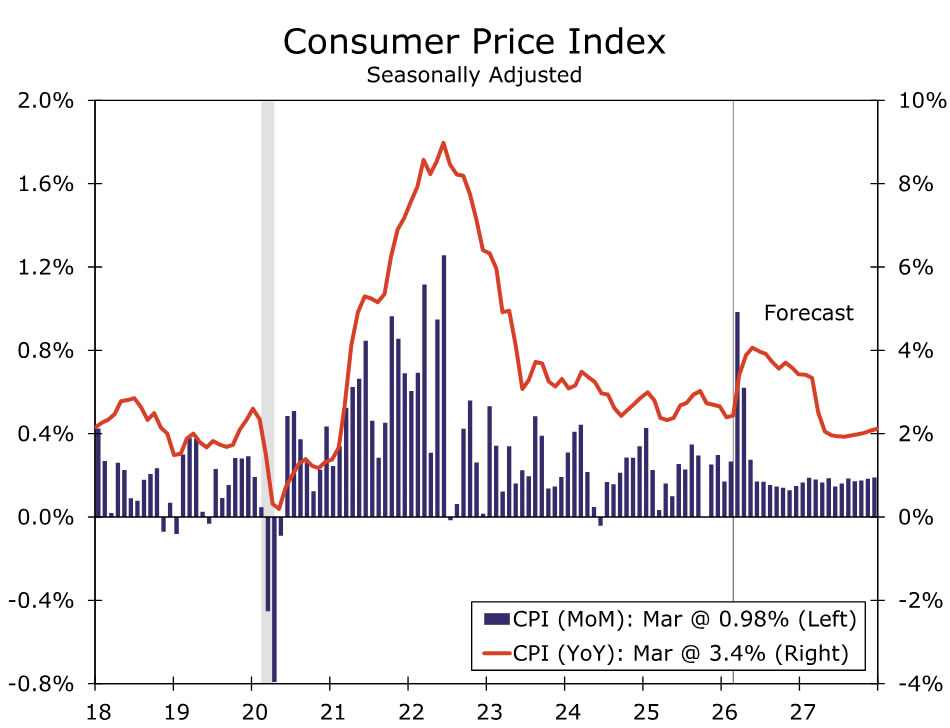

The recent oil shock is likely to dominate the view of inflation in March, but we expect the details to suggest that the modest downward trend in core CPI was already struggling to be maintained. A sustained increase in oil will further complicate progress in reducing inflation as higher production and transportation costs slowly seep into some core categories. Yet, the reduction in household purchasing power caused by higher gasoline prices is likely to limit the ability for some companies to pass on higher costs. We expect the year-over-year rate of core CPI to be stuck in the range of 2.7%–3.1% through the remainder of this year as a result (chart).

G10 Week Ahead

Canada Labor Force Survey • Friday

We look for Canada’s March Labor Force Survey (LFS) to rebound from the soft January/February prints with +20K jobs, with the unemployment rate steady at 6.7%. Risks are asymmetric: upside to the jobs number and downside to the unemployment rate. The near-term story is a labor market that’s stable, not collapsing—with the main fragility still concentrated in manufacturing and trade-exposed goods, while services, health care, energy and the public sector continue to look relatively resilient. That sector mix should be increasingly shaped by U.S. tariff exposure, the recent surge in energy prices and the impending USMCA review. Structurally, the backdrop has shifted: a shrinking population (net outflow of temporary residents) and an aging workforce are lowering labor force growth—and with it the monthly job threshold needed to keep unemployment stable. The implication is that the unemployment rate can drift lower even with only modest job creation over the coming months. A steadier labor market, in turn, likely tilts the Bank of Canada’s (BoC) focus back toward inflation. We continue to see the BoC stuck on hold as it assesses the energy-price shock and the risk of inflation persistence/feedback. April still looks far too early for a move, but the Monetary Policy Report should offer a clearer read on the BoC’s reaction function. We still pencil in a Q3 (July) hike, with the risk of a later hike this year depending on the intensity and persistence of energy and commodity price pressures.

EM Week Ahead

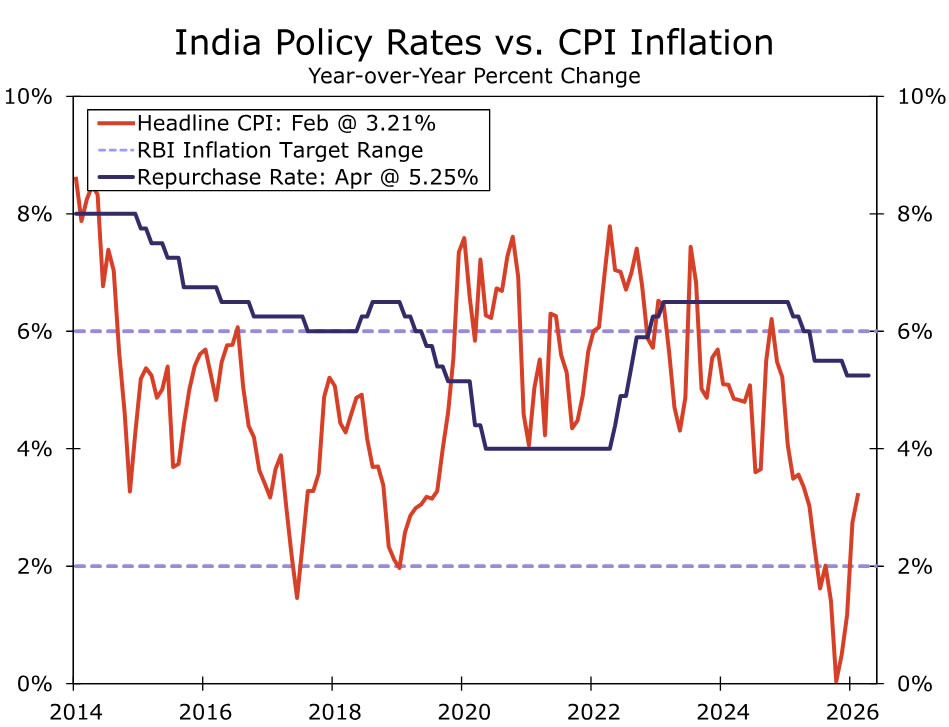

Reserve Bank of India • Wednesday

Reserve Bank of India (RBI) policymakers will assess monetary policy settings next week for the first time since the oil price shock, and we expect interest rates to be left on hold. Prior to events in the Middle East, RBI policymakers were inching closer to ending the easing cycle, but perhaps maintained a slight bias for additional rate cuts. With oil prices likely to push headline inflation sharply higher in the coming months and keep the rupee under pressure, we have our doubts the bias remains for additional rate cuts. In fact, through our forecast horizon, we believe rates in India will be kept unchanged as inflation pressures build and INR remains on the back foot.

But the RBI, like many other central banks, is caught in between an inflation and a growth shock. The age-old question will loom for the RBI: support growth or contain inflation? Inflation is likely to be the priority for policymakers, but the economy is set to soften given India’s status as a major oil importer. Softening growth could keep the bias for policymakers tilted toward rate cuts. But, in our view, with the economy still likely to grow 6.5%–7% this calendar year, perhaps the need to lower policy rates is not that pressing. Either way, we will get more insight into the RBI thought process and how they consider this trade-off next week.

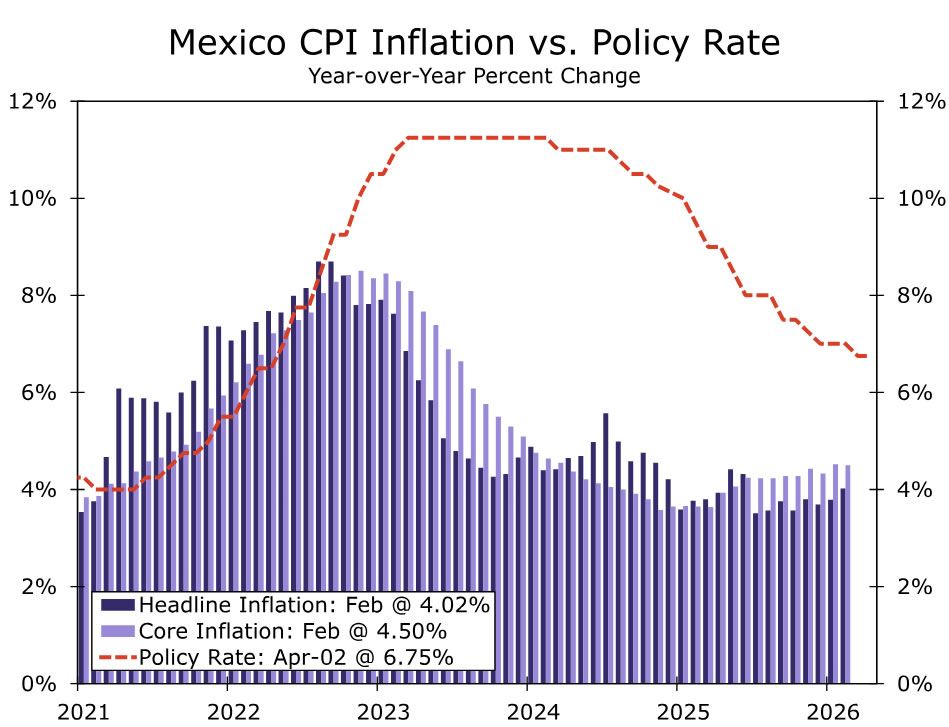

Mexico CPI • Thursday

For Mexico watchers, the path of inflation has been top of mind. Not only to get a sense of the future direction of Banxico monetary policy but also to gauge whether financial markets will deem prior Banxico easing as a policy error. March inflation should show headline CPI popping higher to reflect the spike in energy prices. At the same time, core inflation, the measure that strips out elevated energy costs, is likely to remain flat. Policymakers have been more focused on sluggish growth prospects to rationalize lowering interest rates, but another key component to justify easing monetary policy has been policymakers’ view that core inflationary pressures are muted.

A flat March core inflation print combined with a softening growth outlook, in our view, should continue to give policymakers rationale to cut policy rates at least one more time. Just recently, we adjusted our Banxico outlook to reflect our view for a terminal rate of 6.50% by mid-year. For now, that forecast remains in place, but we also flagged the possibility that Banxico has lowered rates too much. Risks on the horizon such as trade and political uncertainty, could prompt capital flight as carry associated with the peso has been eroded over time. Even a further shift in risk sentiment from the oil price shock can drive a repricing of local financial markets that ultimately prompts as aggressive tightening cycle that keeps growth weighed down for an extended period of time.

Brazil CPI • Friday

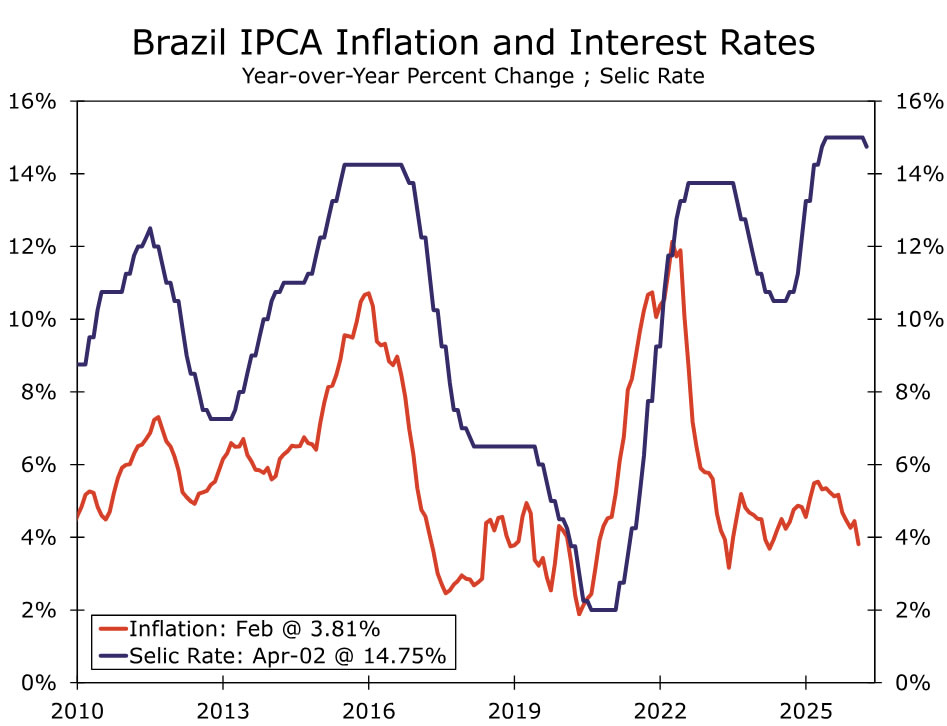

While Brazil is one of the economies a bit more shielded from higher energy prices, the inflationary impulse of a spike in energy costs will still materialize. To that point, we expect year-over-year headline inflation to rise close to, possibly back above, 4% when March data are released next week. The balance of risk is shifted toward a firmer rise in inflation, and with inflation expectations already reacting to the rise in energy prices, policymakers are also in reaction mode. To that point, fiscal authorities have already deployed policy to offset the rise in energy prices for households. And monetary policymakers are communicating more caution when considering further reductions in interest rates.

The rise in March inflation should keep fiscal and monetary policymakers busy, but also on guard going forward. For fiscal policy, President Lula is likely to deploy subsidies and other forms of financial support ahead of his re-election campaign. Brazilian Central Bankers are also likely to keep the gradual pace of rate reductions in place, possibly even keep rates steady, to defend against unanchored inflation expectations from materializing. Combined with geopolitical tensions that do not seem to be receding all that quickly, this policy mix could be in place for an extended period of time.

{kind=link}