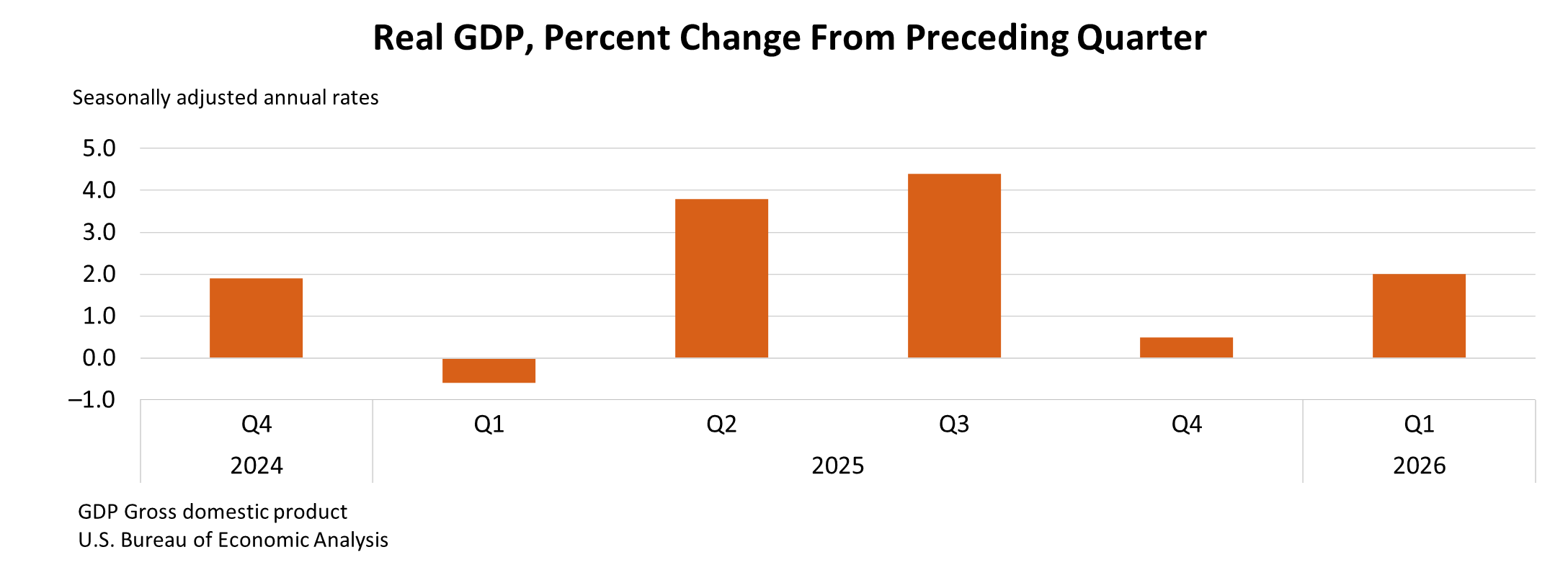

US economy expanded at an annualized pace of 2.0% in Q1, accelerating from 0.5% in Q4 2025 but falling short of expectations for 2.2% growth. The rebound was driven by stronger investment, exports, government spending, and continued consumer activity, although a rise in imports—subtracting from GDP—partly offset the overall gain.

The composition of growth points to a shift in momentum. Investment and exports provided a stronger contribution, while government spending also turned higher. However, consumer spending decelerated compared to the previous quarter, suggesting some moderation in household demand. Still, underlying domestic demand remained firm, with real final sales to private domestic purchasers rising 2.5%, up from 1.8% in Q4.

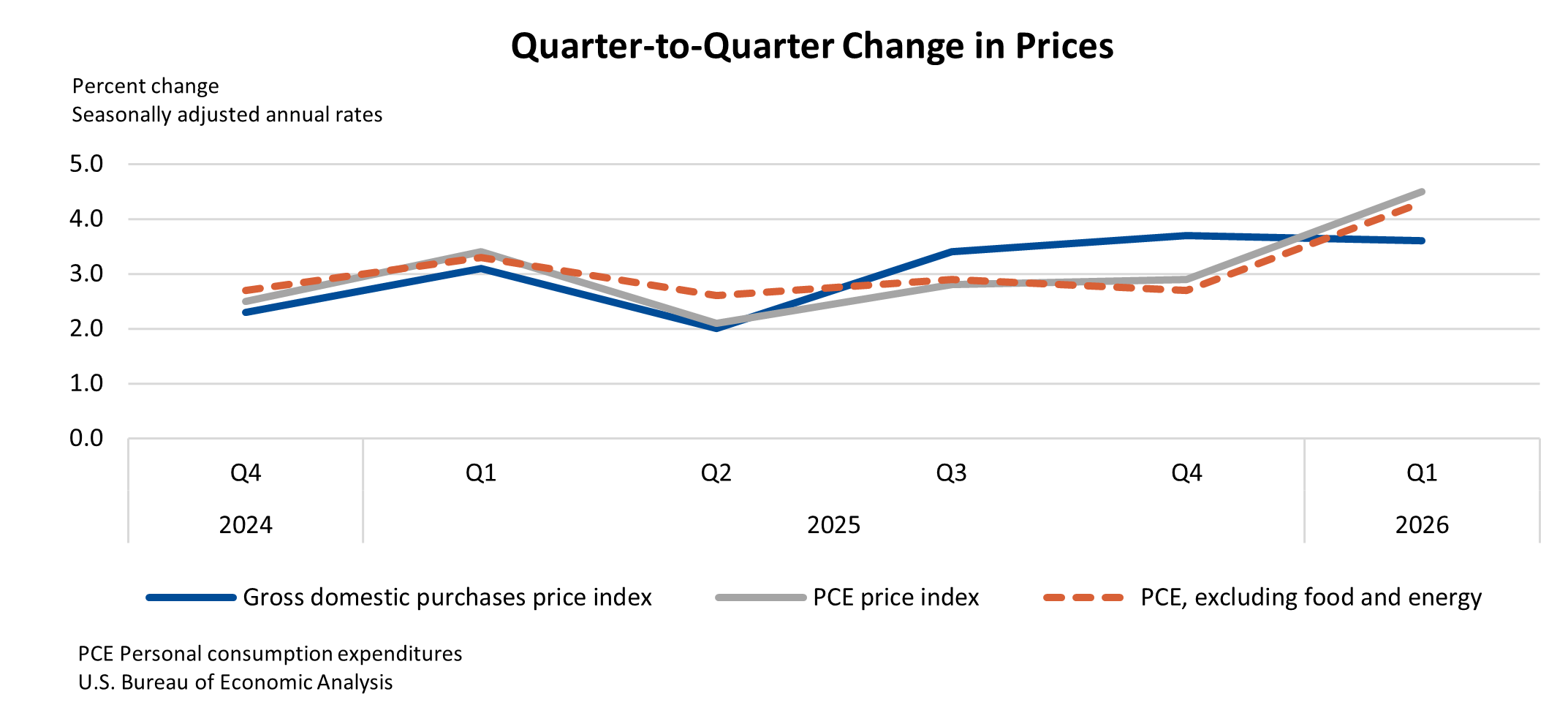

Inflation pressures, however, intensified sharply. The PCE price index jumped to 4.5% from 2.9%, while core PCE rose to 4.3% from 2.7%, signaling a significant pickup in underlying price pressures. Although the broader price index for domestic purchases eased slightly to 3.6%, the surge in PCE inflation underscores a challenging backdrop for policymakers, where growth remains resilient but inflation risks are rising again.

{kind=link}