- The futures market is mistaken in expecting 2–3 ECB rate hikes in 2026.

- Accelerating US inflation will prompt the Fed to adopt a more hawkish stance.

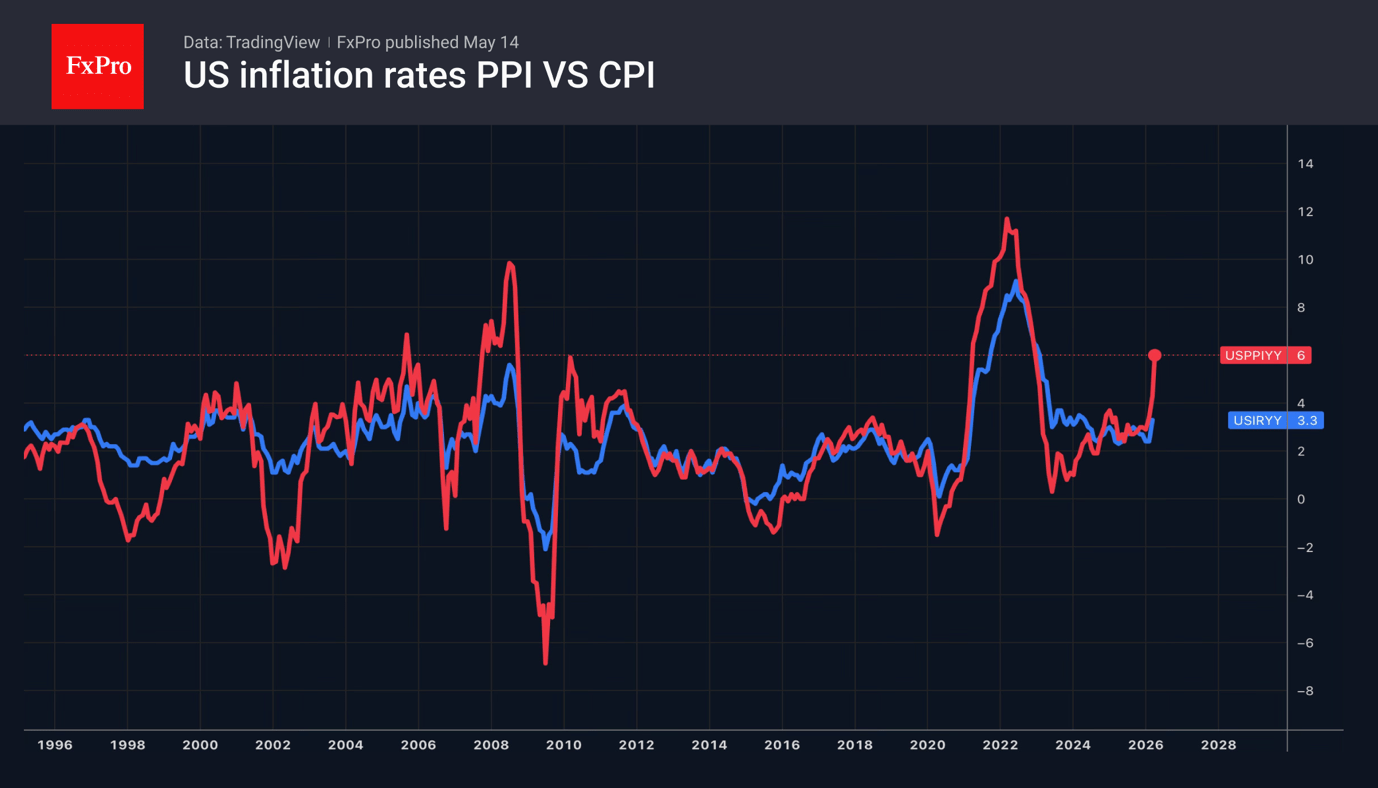

The US dollar took two steps forward and one back following another batch of hawkish macroeconomic data and new record highs for US indices. NVIDIA’s market capitalisation rising to $5.5 trillion triggered an S&P 500 rally, boosted global risk appetite and reduced demand for the greenback as a safe-haven asset. Bears on EURUSD were unable to fully capitalise on the sharpest PPI acceleration since 2022, up to 6% in April.

The Fed prefers to gauge inflation using the Personal Consumption Expenditures (PCE) index. Based on CPI and PPI data, core PCE could accelerate to 3.3% in April. Coupled with the stabilisation of the labour market, this gives CME derivatives a probability of over 30% of a rate hike in 2026, rising to 50% by March 2027.

Meanwhile, the ECB has signalled that it may not share the view of Bloomberg experts and the futures market that there will be 2–3 rate hikes of 0.25 percentage points this year. Executive Board member Olli Rehn stated that the eurozone is on the brink of a stagflationary shock, whilst Chief Economist Philip Lane believes that a contraction in domestic demand will make it difficult to adjust monetary policy.

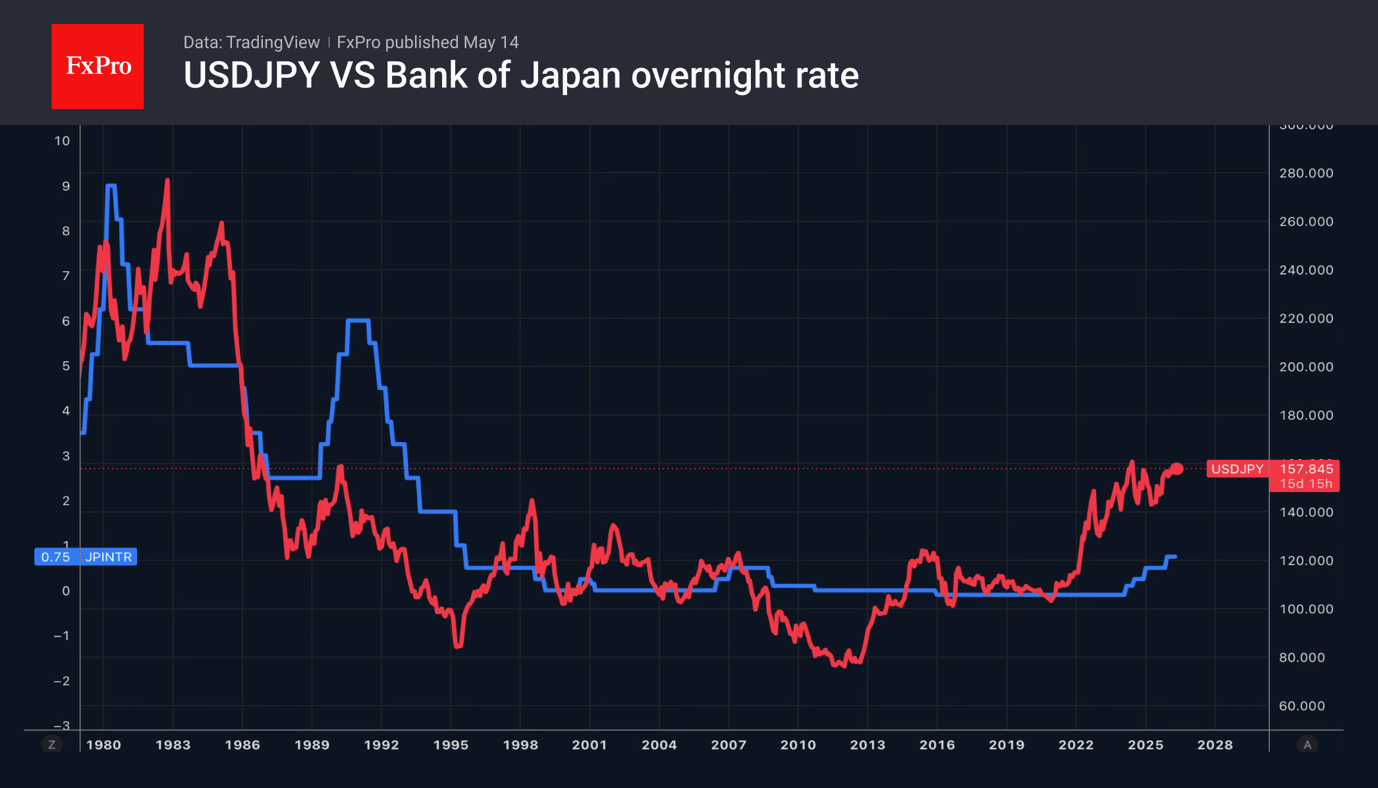

The yen found its footing after three days of selling following an OECD statement that the Bank of Japan would raise its overnight rate to 2% by the end of 2027. It must continue its cycle of monetary tightening to prevent the economy from overheating.

From the perspective of the bond yield spread, USDJPY looks overbought. This allows the government to argue that the pair has become detached from economic fundamentals. However, speculators are betting on high oil prices, carry trades and strong demand for the US dollar as a safe-haven asset.

The pound continued to fall amid comments from central bank officials. Sarah Breeden believes that the Bank of England cannot wait forever, but that monetary policy tightening is not required in either June or July. Previously, traders were buying GBPUSD on expectations of three rate hikes in 2026 but rising political risks and the BoE’s dovish rhetoric are forcing them to offload sterling.

{kind=link}