The first trading day of Kevin Warsh’s tenure as Federal Reserve Chair is already being defined by rising Treasury yields, stronger Dollar demand, and market skepticism that the Trump-Xi summit will deliver meaningful relief from the global energy shock.

US Treasury yields surged again in Asian session, with the 10-year yield breaking decisively above the key 4.5% psychological level. The move extended a broader global bond selloff that has accelerated throughout the week following hotter-than-expected US inflation data and resilient consumer spending figures.

The market reaction suggests investors could be beginning to position for a structurally different Fed regime under Warsh.

While current Fed officials have generally maintained a cautious wait-and-see stance, bond markets appear focused on the possibility that Warsh may ultimately prove significantly less tolerant of persistent inflation than Jerome Powell. The incoming Fed Chair has repeatedly criticized the central bank’s post-pandemic policy framework, particularly its delayed response to inflation and its heavy reliance on balance-sheet expansion.

During Senate testimony in April, Warsh described the Fed’s failure to tighten policy sooner during 2021-2022 as a “fatal policy error.” He has also been among the strongest critics of the Fed’s multi-trillion-dollar balance sheet, arguing prolonged asset purchases distorted financial markets and weakened monetary discipline.

That backdrop is helping drive a broader repricing across global markets.

Higher US Treasury yields triggered weakness across Asian equity markets, especially in South Korea, as tighter global financial conditions pressured risk sentiment. The resulting risk-off tone fed back into stronger Dollar demand, particularly against higher-beta currencies such as Aussie and Kiwi.

Importantly, however, markets are still only cautiously pricing outright additional Fed tightening. Fed funds futures currently imply roughly a 40% probability of one more rate hike before year-end. But the more important shift may be broader expectations that rates could stay elevated for significantly longer under a more inflation-focused Fed leadership structure.

At the same time, energy markets continue signaling little confidence that geopolitical risks are meaningfully improving.

Despite the highly anticipated Trump-Xi summit in Beijing, Brent crude remains stuck near $107 rather than collapsing lower. For markets, that is interpreted as evidence that traders do not believe the Strait of Hormuz crisis is close to resolution.

Trump said today that both leaders “feel very similar” regarding Iran and that: “We want the straits open.” But the remarks offered little operational clarity on how shipping security would actually be restored.

China’s Foreign Ministry took a slightly firmer tone on Friday, calling for a “comprehensive and lasting” ceasefire while stating: “Shipping routes should be reopened as soon as possible.” The ministry also emphasized that “dialogue and negotiation are the right path” and said the two leaders reached “a series of new consensuses,” though Beijing again avoided providing specifics.

That ambiguity appears to be preventing oil traders from removing the substantial war premium embedded in crude markets. If anything, Brent remaining near $107 despite the summit likely reinforces investor belief that energy-driven inflation pressures could remain elevated well into the second half of the year.

That leaves markets entering the Warsh era facing a difficult combination:

- structurally higher yields,

- persistent inflation risk,

- elevated oil prices,

- and no convincing resolution to the Hormuz crisis.

In currency markets, Dollar led gains broadly during the Asian session. Yen also strengthened modestly on defensive positioning, while Euro outperformed most commodity-linked currencies. Kiwi was the weakest performer of the day, followed by Aussie and Swiss Franc, while Sterling and Loonie traded more mixed.

In Asia, at the time of writing, Nikkei is down -1.68%. Hong Kong HSI is down -0.87%. China Shanghai SSE is up 0.12%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield is up 0.097 at 2.732. Overnight, DOW rose 0.75%. S&P 500 rose 0.77%. NASDAQ rose 0.88%. 10-year yield fell -0.02 to 4.46.

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY climbed back toward the critical 160 level as surging US Treasury yields widened the US-Japan rate gap and intensified doubts over whether Japanese intervention can still effectively stabilize the Yen. Read More.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April as higher oil prices, chemical costs, and a weak Yen intensified imported inflation pressures, reinforcing expectations for further BoJ tightening. Read More.

New Zealand PMI Falls to 50.5 as New Orders Turn Negative

New Zealand’s manufacturing sector lost significant momentum in April as new orders fell into contraction territory and firms reported rising freight, fuel, and supply-chain pressures linked to the Iran war. Read More.

Fed’s Williams Sees No Need for Rate Changes Right Now

Fed’s John Williams said policymakers see no urgent need to change interest rates despite rising inflation pressures tied to the Middle East conflict, emphasizing that longer-term inflation expectations remain stable for now. Read More.

Fed’s Barr Says Shrinking Balance Sheet Should Not Trump Financial Stability

Fed Governor Michael Barr warned that proposals to shrink the Fed’s balance sheet by weakening bank liquidity requirements could make the financial system more fragile rather than safer. His remarks highlighted growing debate inside the Fed ahead of the Kevin Warsh era. Read More.

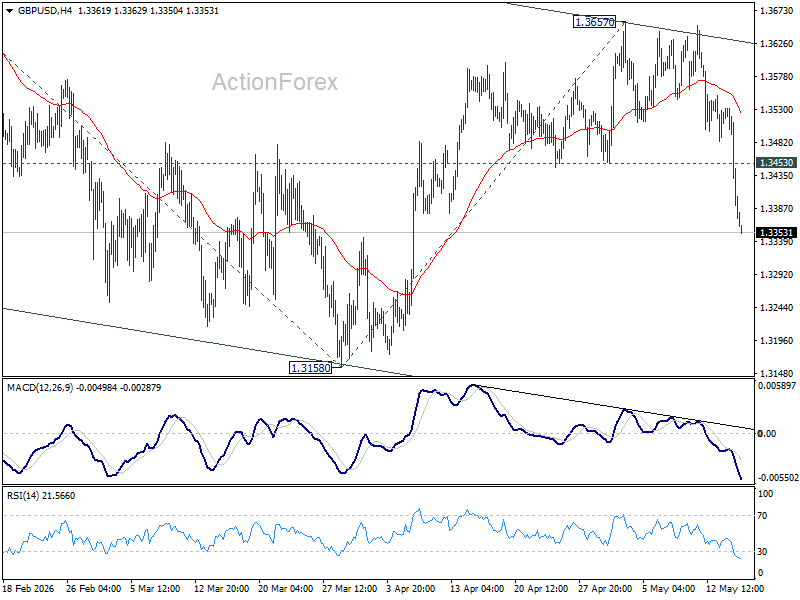

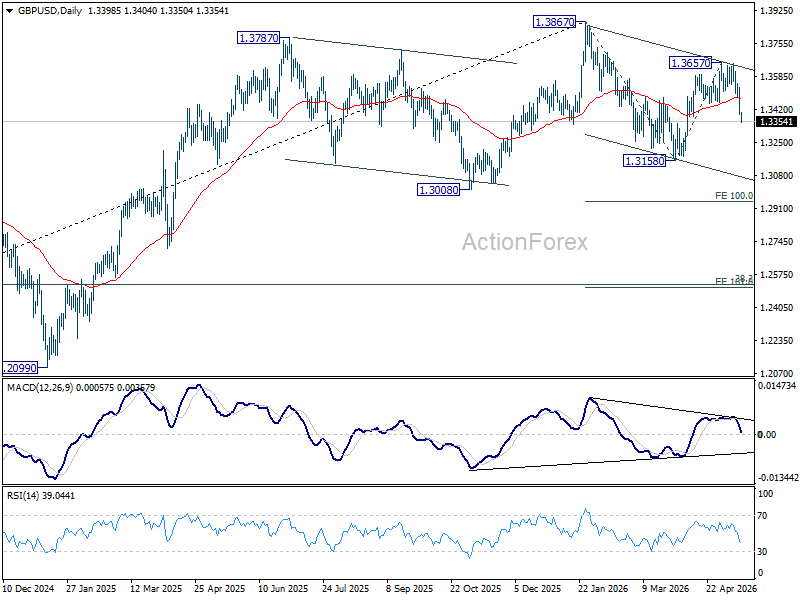

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3352; (P) 1.3442; (R1) 1.3490; More…

GBP/USD’s steep decline today suggests that rebound from 1.3158 has already completed at 1.3657. Intraday bias is back on the downside for retesting 1.3158. Decisive break there will target 100% projection of 1.3867 to 1.3158 from 1.3657 at 1.2948. For now, risk will stay on the downside as long as 1.3453 support turned resistance holds, in case of recovery.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

{kind=link}