The sharp rise in US Treasury yields remains one of the dominant macro themes in global markets this week, with the 10-year yield climbing back to 4.62% after only a brief pullback yesterday, near its highest level in more than a year. While markets continue focusing on inflation concerns and expectations for prolonged restrictive Federal Reserve policy, a second and increasingly important driver is emerging beneath the surface: forced liquidation of Treasuries by foreign central banks facing mounting pressure from the global energy shock.

According to reports, foreign governments sharply reduced Treasury holdings in March as the Middle East conflict forced central banks to defend weakening local currencies against surging energy prices. China cut its holdings to USD 652.3B, the lowest level since September 2008, while Japan — the largest foreign holder of US debt — reduced holdings by roughly USD 47B to USD 1.191T. Overall foreign holdings declined from USD 9.49T in February to USD 9.25T in March. The liquidation created a significant supply-demand imbalance in the Treasury market, directly contributing to rising yields.

The mechanics of the move are creating what resembles a vicious feedback loop. Central banks sell Treasuries to raise Dollars and stabilize domestic currencies weakened by the oil shock. But higher Treasury yields simultaneously strengthen the Dollar further, increasing depreciation pressure on those same currencies and potentially forcing additional reserve liquidation. In effect, the Treasury market is no longer reacting solely to inflation expectations or Fed policy. It is increasingly reflecting global liquidity stress and balance sheet pressures across the international financial system.

Meanwhile, oil prices remain elevated despite temporary diplomatic relief headlines. Brent crude briefly pulled back after US President Donald Trump announced he was postponing a planned strike on Iran at the request of Gulf allies including Saudi Arabia, the UAE, and Qatar. However, the decline proved shallow because the underlying drivers keeping energy markets tight remain firmly in place. The Strait of Hormuz remains effectively blocked, commercial inventories are critically low, and the broader geopolitical standoff continues unresolved.

Reports also suggest the latest Iranian proposal sent to Washington through Pakistan did little to alter the underlying impasse. Iran reportedly focused its framework on separating the war and maritime blockade issues from the nuclear negotiations, prioritizing immediate economic and military relief while delaying the core nuclear questions. For Trump and his national security team, including Defense Secretary Pete Hegseth, sidelining the nuclear issue appears unacceptable, reinforcing market expectations that tensions may persist rather than de-escalate meaningfully.

In currency markets, Dollar is the strongest major currency of the day so far, supported by rising yields and persistent global uncertainty. Sterling and Yen also outperformed, while Aussie and Kiwi lagged amid weaker risk sentiment and renewed concerns about China’s slowdown. Swiss Franc underperformed as higher global yields reduced demand for low-yielding safe havens, while Euro and Canadian Dollar traded more neutrally in the middle of the pack.

Attention now turns to whether equity markets can continue absorbing the rise in global yields without a broader risk-off break. Ultimately, the next major move in stocks may depend more on geopolitics directly and less on whether corporate earnings can continue justifying valuations in a world where Treasury yields are rapidly moving back toward cycle highs.

Canada CPI Misses Forecasts at 2.8% in April, Core Inflation Pressures Ease

Canada’s inflation rate accelerated to 2.8% in April as gasoline prices surged nearly 29%, but softer core inflation measures suggest underlying price pressures remain more contained than headline data imply. Read More.

EUR/GBP: Weak UK Jobs Data Pushes BoE Toward Patience, but CPI Holds Key to Breakout

Sterling softened slighlty after payrolls fell sharply and unemployment rose to 5.0%, reinforcing case for BoE patience. But with oil prices climbing again, tomorrow’s UK inflation data could quickly reshape the outlook. Read More.

Eurozone Trade Surplus Shrinks Sharply to EUR 7.8B as Exports to US Collapse

The Eurozone’s trade surplus narrowed sharply in March as exports to the US collapsed and imports continued rising, reinforcing concerns that weakening global demand and higher energy costs are increasingly weighing on Europe’s economy. Read More.

UK Unemployment Rate Rises to 5.0% as Payroll Employment Continues to Decline

UK payroll employment fell again in April while unemployment rose to 5.0% in the three months to March, signaling softer labor market conditions. However, wage growth remained firm enough to keep inflation concerns alive for the Bank of England. Read More.

Japan Q1 GDP Beats Forecasts, Economy Entered Iran Conflict on Solid Footing

Japan’s economy expanded faster than expected in Q1, with exports, consumer spending, and business investment all contributing to stronger growth before the Middle East energy shock intensified. The data suggest Japan entered the Iran conflict period with some economic buffers already in place. Read More.

AUD/CAD Reverses Lower as China Slowdown, RBA Pause, and Oil Surge Shift Momentum to Loonie

AUD/CAD reversed lower this week as weak Chinese data, renewed risk-off sentiment, and fading expectations for a fourth straight RBA rate hike undermined Aussie, while rising oil prices continued boosting Canadian Dollar. Technical signals now suggest a possible medium-term top may already be forming near parity. Read More.

RBA’s Hunter Warns Existing Inflation Pressures Could Amplify Oil Shock Across Economy

RBA Chief Economist Sarah Hunter warned that the oil shock is hitting an economy already strained by elevated inflation pressures, raising the risk that higher fuel costs spread more rapidly across businesses and consumers. The RBA is increasingly concerned inflation expectations could become embedded. Read More.

RBA Minutes: Tactical Wait-and-See, Not End of Tightening Bias Yet

RBA minutes showed policymakers are shifting into a tactical wait-and-see phase after concluding rates are now likely restrictive, but the Board made clear the tightening bias has not been abandoned as inflation risks remain elevated. Read More.

Australian Westpac Consumer Confidence Ticks Higher, but Energy and RBA Rate Fears Still Dominate

Australian consumer sentiment recovered slightly in April after fuel prices eased, but households remained deeply pessimistic as higher interest rates and Strait of Hormuz-related energy risks continued weighing on confidence. Westpac expects the RBA to pause in June, though further rate hikes may still follow later this year. Read More.

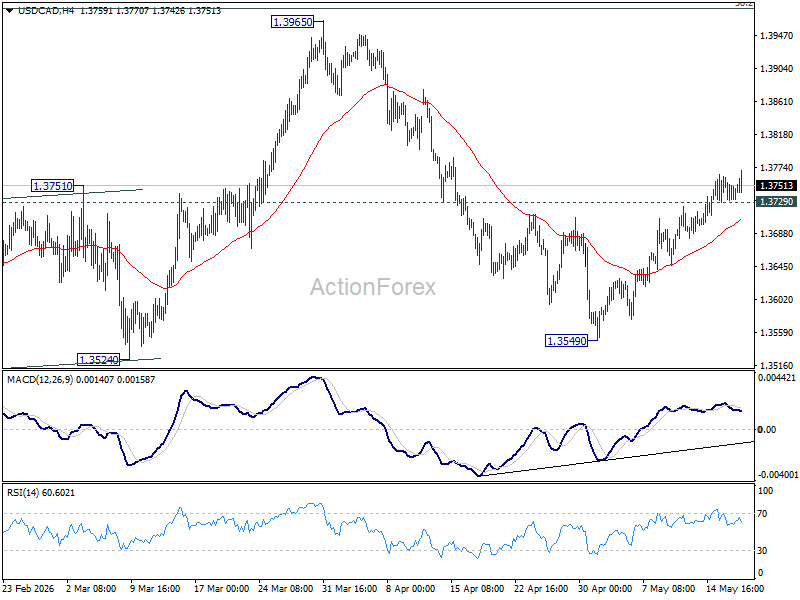

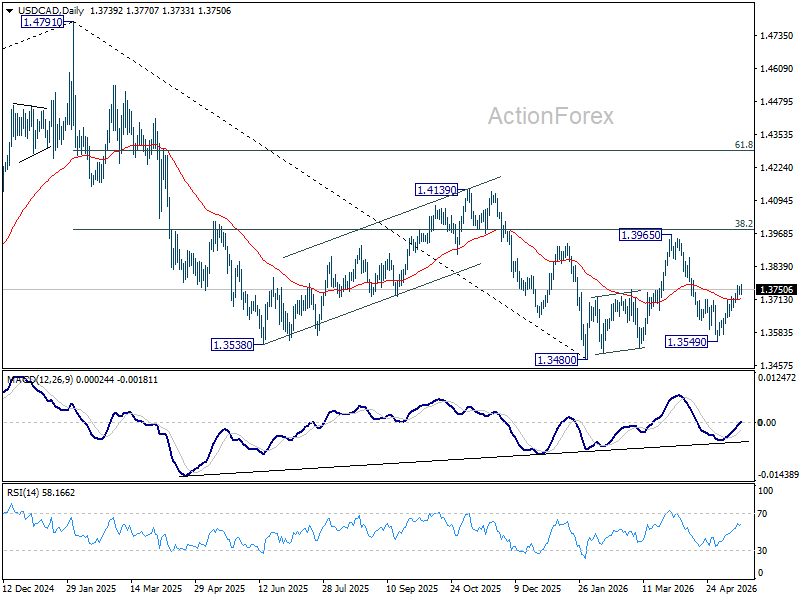

USD/CAD Daily Outlook

Intraday bias in USD/CAD stays mildly on the upside as rebound from 1.3549 is in progress. This rise is seen as the third leg of the corrective pattern from 1.3480. Further rise would be seen towards 1.3965 resistance. On the downside, below 1.3729 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

{kind=link}