Optimism surrounding a US-Iran peace agreement faded slightly today. Fresh military activity and tougher negotiation rhetoric cooled some of the aggressive optimism that swept across markets earlier this week. Yet the broader market message remains surprisingly calm: traders still believe some form of deal is more likely than collapse.

That confidence is visible most clearly in oil markets. Brent crude recovered modestly today but remained near $96 a barrel — dramatically below last week’s panic highs above $110. US 10-year Treasury yields also continued slipping below 4.5%, while US equity futures pointed higher again. In other words, markets may have stopped aggressively adding to the peace trade, but they are not meaningfully reversing it either.

The latest headlines, however, exposed just how fragile the current ceasefire remains. U.S. Central Command confirmed “self-defense strikes” near Bandar Abbas targeting Iranian-linked vessels allegedly attempting to deploy mines as well as missile launch sites. Iran’s Revolutionary Guard responded by warning of retaliation after engaging U.S. drones and an F-35 jet fighter that entered Iranian airspace. The coexistence of active military operations and ongoing diplomacy is the defining feature of this conflict.

Negotiations themselves are also entering the harder implementation stage. Iran’s Tasnim agency described talks with Washington as “overall good,” but said the proposed memorandum of understanding depends on the release of USD 24 billion in frozen Iranian funds. Top negotiator Mohammad Baqr Qalibaf has reportedly traveled to Qatar to finalize that mechanism, with Tehran demanding half the funds upfront simply to sign the 14-point agreement. Meanwhile, US President Donald Trump warned there would either be “a Great Deal for all or, no Deal at all,” while U.S. Secretary of State Marco Rubio acknowledged the process could still “take a few days.”

Currency markets reflected that more cautious tone. Dollar rebounded as traders partially unwound aggressive anti-Dollar positioning tied to rapid Hormuz normalization hopes. Euro firmed up after ECB Chief Economist Philip Lane and Executive Board member Isabel Schnabel strongly reinforced expectations for a June rate hike. Schnabel’s warning that the economic damage from the conflict may already be irreversible even if peace is reached immediately reinforced the view that central banks may still need to tighten despite falling oil prices.

For now, markets are essentially defending the peace trade rather than expanding it. Oil prices, bond yields, and equities all continue suggesting investors still expect eventual normalization. But conviction is no longer as strong as it was at the start of the week.

USD/JPY Rising Again, Markets May Test Japan Before They Test Iran

The “peace dividend” trade that crushed oil prices and weakened Dollar earlier this week is starting to wobble. As optimism over a rapid US-Iran agreement fades and USD/JPY climbs, traders may soon test Tokyo’s intervention tolerance at 160 before negotiators even finalize a Hormuz deal. Read More.

ECB’s Lane Says Inflation Outlook Worsened as June Hike Expectations Build

ECB Chief Economist Philip Lane gave markets little reason to doubt that another rate hike is approaching in June. Lane said inflation forecasts will likely be revised higher again next month as the Iran conflict keeps oil prices elevated and adds “upward pressure on inflation” across the Eurozone economy. Read More

ECB’s Schnabel Says Iran Peace Deal May Already Be Too Late to Avoid June Hike

ECB Executive Board member Isabel Schnabel warned that even a US-Iran peace deal may no longer be enough to stop a June rate hike. Schnabel said the ECB can no longer “look through” the energy shock because inflation pressures are already spreading into the broader Eurozone economy through second-round effects and rising inflation expectations. Read More.

Euro Fights “Two-Front War” Against Sterling and Swiss Franc

Euro may be rising against Dollar this week, but it is quietly losing ground in the more important relative-value battles against Sterling and Swiss Franc. Weak Eurozone PMIs, falling bond yields, and collapsing oil prices are exposing growing vulnerabilities in EUR/GBP and EUR/CHF as traders increasingly favor UK manufacturing resilience and renewed CHF demand. Read More.

BoJ’s Himino Keeps Hawkish Tone but Signals Caution on Middle East Shock

Bank of Japan Deputy Governor Shinichi Himino reaffirmed that the BoJ will continue raising rates, but warned that Middle East tensions could still reshape Japan’s economic outlook. Himino said rising global bond yields reflect “global concerns about inflation” while emphasizing that policymakers are closely monitoring oil prices, market functionality, and geopolitical risks before deciding the pace of further tightening. Read More.

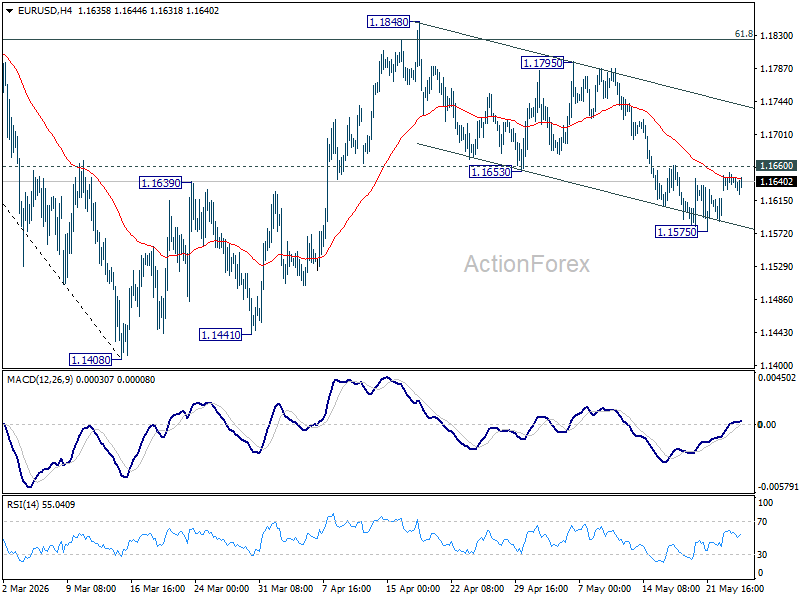

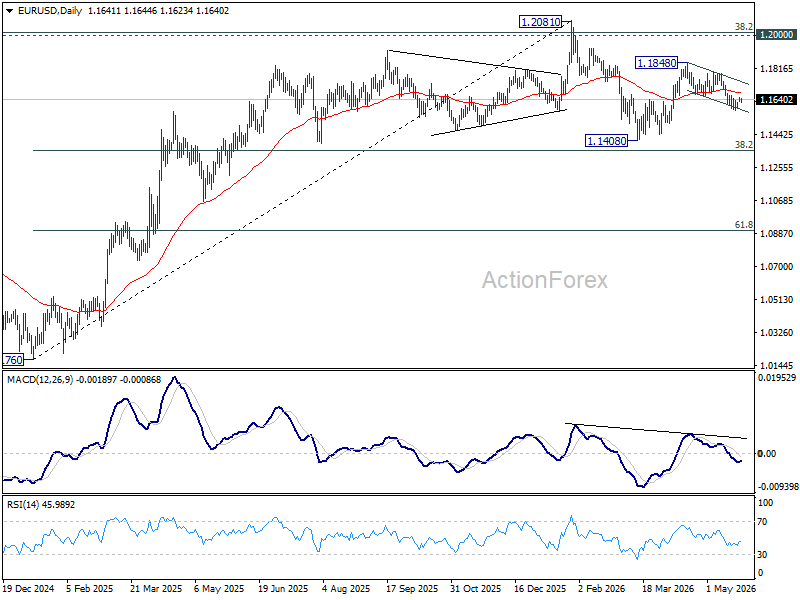

EUR/USD Daily Outlook

Range trading continues in EUR/USD and intraday bias stays neutral at this point. On the upside, firm break of 1.1660 resistance will argue that fall from 1.1848 has completed as a correction at 1.1575. Intraday bias will be back on the upside for 1.1795 resistance first. On the downside, break of 1.1575 will solidify the case that rebound from 1.1408 has completed at 1.1848, and bring deeper fall back to retest 1.1408 low.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1544). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}