The biggest move in global markets is still happening in oil. The most important move may come tomorrow.

Brent crude plunged below USD 80 today, extending a dramatic collapse that began after the United States and Iran reached a provisional peace agreement over the weekend. The decline accelerated after President Donald Trump arrived at the G7 summit and declared that the peace framework had already been signed, adding that the Strait of Hormuz would fully reopen on Friday and remain free of Iranian tolls. With a formal signing ceremony scheduled in Geneva later this week, traders are increasingly treating the normalization of oil supply as a certainty rather than a possibility.

That helps explain why Brent’s decline has become so relentless. Markets are no longer pricing a ceasefire. They are pricing ships moving freely through Hormuz again. They are pricing Iranian exports returning. They are pricing the gradual removal of a war premium that dominated energy markets for months. The peace trade is still alive, but at this stage it is largely concentrated in crude oil itself.

Elsewhere, the reaction has been surprisingly muted. US futures are little changed. European equities are modestly higher. Asian markets finished mixed. Currency markets have been even quieter, with most major pairs trapped within yesterday’s ranges. In other words, investors appear to believe that the geopolitical story is largely understood. The focus has already shifted to what comes next.

Even central-bank decisions in Asia Pacific are quickly fading from view. The Yen’s post-BoJ-hike rally evaporated almost as quickly as it appeared, while the Australian Dollar recovered after the RBA’s widely expected hold. Today’s currency rankings tell a story of hesitation rather than conviction. The Euro is narrowly leading gains, followed by Sterling and the New Zealand Dollar. The Swiss Franc sits at the bottom, while the Dollar and Yen occupy the middle ground. The differences between them are small, reflecting a market reluctant to take major positions ahead of Wednesday’s Federal Reserve decision.

That caution looks justified. Markets broadly expect the Fed to keep rates unchanged at 3.50%-3.75%, but there is far less certainty about the message accompanying the decision. According to CNBC’s latest survey, 88% of respondents expect policymakers to remove the easing bias that previously suggested the next move would likely be a rate cut. At the same time, 81% do not expect the Fed to go so far as to explicitly signal a future rate hike. That leaves investors bracing for a potentially hawkish shift in tone without a corresponding tightening signal.

The market spent the past three months asking whether peace would come to the Middle East. It increasingly believes that answer is yes. The next question is whether the Federal Reserve believes the inflation damage left behind by the conflict is beginning to fade. Brent crude is still trading the peace deal. By this time tomorrow, the rest of the market will likely be trading Kevin Warsh.

Bitcoin Rally Faces Two Major Hurdles Before Bullish Reversal Can Be Confirmed

Bitcoin has defended 60,000. Now it must prove the rebound is real. Improving risk sentiment and stronger ETF inflows have pushed prices back above 66,000, but two major resistance levels still stand between the current rally and a confirmed trend reversal. Read More.

AUD/JPY Weakens After BoJ Hike and RBA Hold, Risks Build Towards 112 and Below

The BoJ hiked. The RBA paused. AUD/JPY noticed. Neither decision surprised markets, but traders appear increasingly convinced that Japan’s tightening cycle still has room to run while Australia’s may be entering a pause. That shift is beginning to show up on the charts. Read More.

BoJ Reaches Key Milestone With First 1% Interest Rate Since 1995

A historic milestone, but not a policy surprise. The Bank of Japan raised rates to their highest level in 31 years, yet markets are paying closer attention to signs that future normalization could proceed more slowly. Read More.

RBA Holds at 4.35% but Keeps Tightening Bias Alive

The RBA paused, but it didn’t sound comfortable. Policymakers held rates at 4.35% while warning that fuel costs are feeding through to broader inflation and that price pressures are likely to stay high for some time. The door to further tightening remains open, but not wide enough to make an August hike the base case. Read More.

German ZEW Sentiment Jumps to 10.5 as Iran Peace Hopes Lift Outlook

Investors are looking past today’s weakness. ZEW sentiment surveys jumped back into positive territory as financial markets increasingly bet that the Middle East conflict is nearing an end and energy pressures will ease. Read More.

China’s Retail Sales Fall for First Time Since 2022 as Domestic Demand Slumps

China’s factories are producing more, but consumers are buying less. Industrial production beat expectations in May, yet retail sales fell for the first time since 2022 and investment weakened sharply. The gap between supply and demand is becoming harder to ignore. Read More.

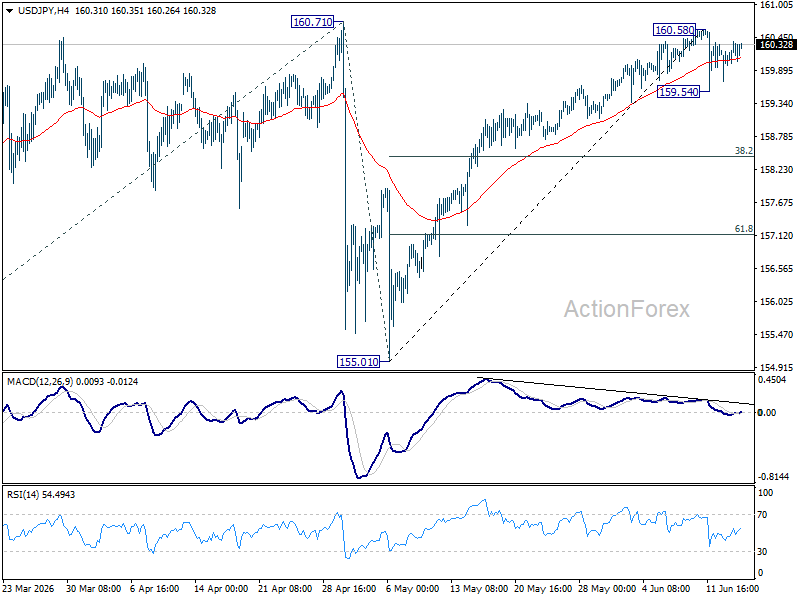

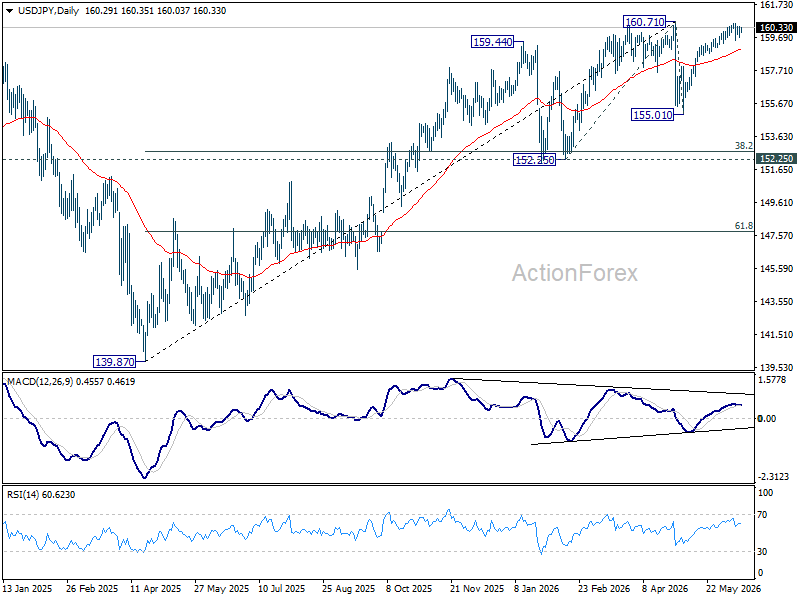

USD/JPY Daily Outlook

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, break of 159.54 will extend the fall from 160.58 short term top to 38.2% retracement of 155.01 to 160.58 at 158.45. However, decisive break of 160.71 will confirm up trend resumption. That should push USD/JPY through 161.94 to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 155.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

{kind=link}