USD/JPY soared to 162.78 in the middle of the week, reaching its highest level in nearly 40 years.

This sharp move has intensified expectations of possible currency intervention by Japanese authorities to support the national currency.

Particular attention is focused on Friday, when US markets will be closed in observance of Independence Day. Low liquidity during such periods traditionally increases the effectiveness of potential interventions, and it was during similar windows that the Bank of Japan previously acted.

Additional pressure on the yen comes from robust US macroeconomic data, which supports expectations of further Federal Reserve interest rate hikes. At the same time, investors remain doubtful that the Bank of Japan is prepared to accelerate monetary tightening, as the regulator favours a gradual normalisation approach.

The continued appeal of carry trade operations and strong demand for the dollar as a safe-haven asset are also weighing on the Japanese currency.

An additional risk factor is Japan’s reliance on oil imports from the Middle East, leaving the economy sensitive to potential disruptions in energy supplies from the region.

Technical Analysis

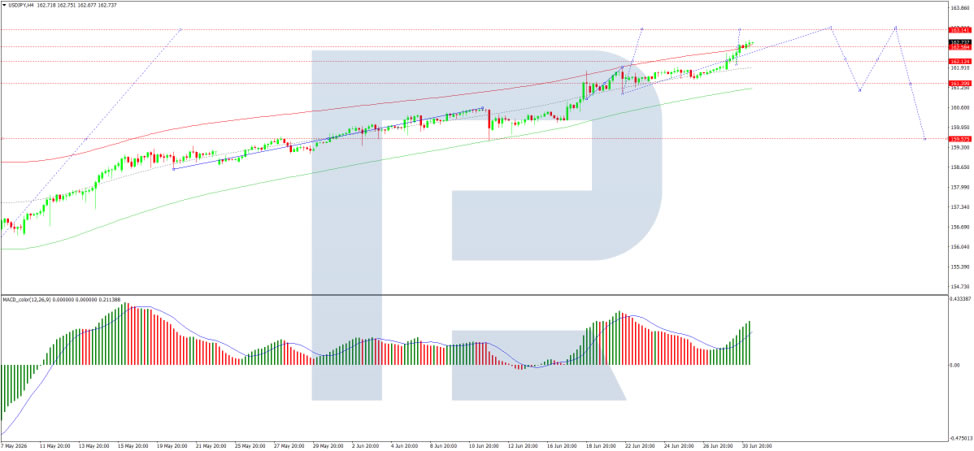

On the H4 chart, USD/JPY is trading within a consolidation range around the 162.55 level and, following an upside breakout, is developing an upward move towards 163.15. This target is expected to be reached today, followed by a decline towards 161.40. The MACD indicator confirms this scenario, with its signal line above zero and pointing firmly upwards, reflecting continued bullish momentum.

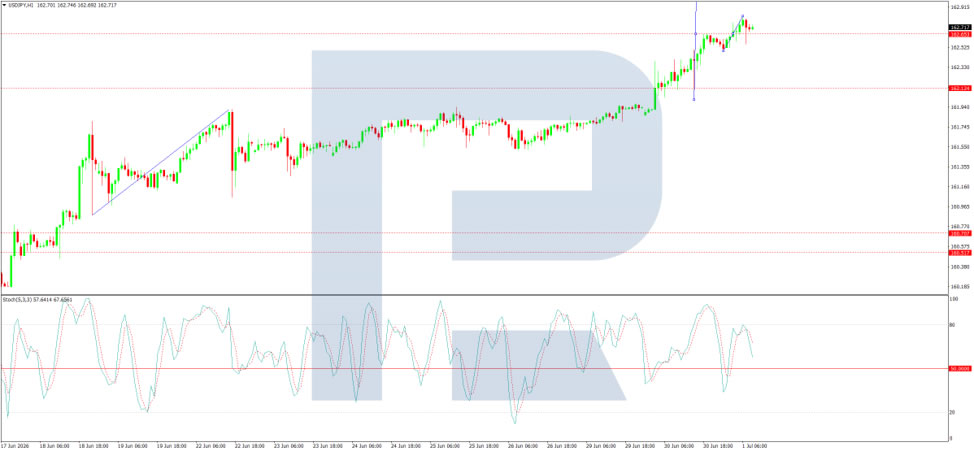

On the H1 chart, USD/JPY is forming an upward structure towards 163.15. A correction towards 162.60 may follow, before a further rise to 163.30, with scope for the trend to extend to 163.50. The Stochastic oscillator supports this scenario, with its signal line above 50 and pointing upwards towards 80, indicating that short-term upside potential remains.

Conclusion

USD/JPY has surged to a 40-year high as multiple factors align against the yen. Strong US data continues to support expectations of further Fed rate hikes, while the Bank of Japan remains cautious in its approach to policy normalisation, widening the interest rate differential. The persistent appeal of carry trades and safe-haven demand for the dollar add further pressure, while Japan’s dependence on Middle Eastern oil imports heightens vulnerability to supply disruptions. Markets are now on high alert for potential intervention, particularly with US markets closed on Friday – a period of low liquidity that has historically increased the likelihood of such actions. Technically, further upside towards 163.15–163.50 appears likely in the near term, although intervention risks remain elevated at these levels.

{kind=link}