EUR/GBP may have passed a turning point that extends well beyond this week’s inflation data. The sharp break below key technical support reflects more than a softer Eurozone CPI report—it signals that one of the market’s biggest policy trades of recent months is beginning to unwind, and intensifying. Investors are no longer betting that the ECB will continue closing the interest-rate gap with the BoE. Instead, that convergence story is rapidly losing momentum.

June’s inflation figures provided the catalyst. Headline CPI slowed from 3.2% yoy to 2.8% yoy, while core inflation eased from 2.6% yoy to 2.4% yoy, both undershooting expectations. Shortly afterwards at the ECB Forum, ECB President Christine Lagarde acknowledged that inflation and growth risks had become “more broadly balanced” following the sharp decline in oil prices after the US-Iran ceasefire. With energy prices back near pre-conflict levels, fears of persistent second-round inflation have eased substantially. Markets now see a July pause as virtually certain, while expectations for another ECB hike beyond that have become far less convincing.

That represents a meaningful shift in the EUR/GBP narrative. Earlier this year, the cross benefited as investors anticipated the ECB would tighten policy more aggressively, gradually narrowing the sizeable interest-rate gap with the BoE. That process has now stalled. The ECB has already delivered one hike, but lower inflation has reduced the urgency for additional moves. By contrast, BoE Governor Andrew Bailey made clear in Sintra that a rate cut is “off the table at the moment,” leaving UK policy broadly unchanged and preserving the existing yield advantage for Sterling, (2.25% vs 3.75%).

Political developments are adding extra support for the Pound. Following Keir Starmer’s resignation, markets expect the incoming administration under Andy Burnham to maintain a disciplined fiscal stance rather than pursue expansionary policies. While not the primary driver, that perception is helping underpin confidence in Sterling as monetary policy expectations increasingly move in its favour.

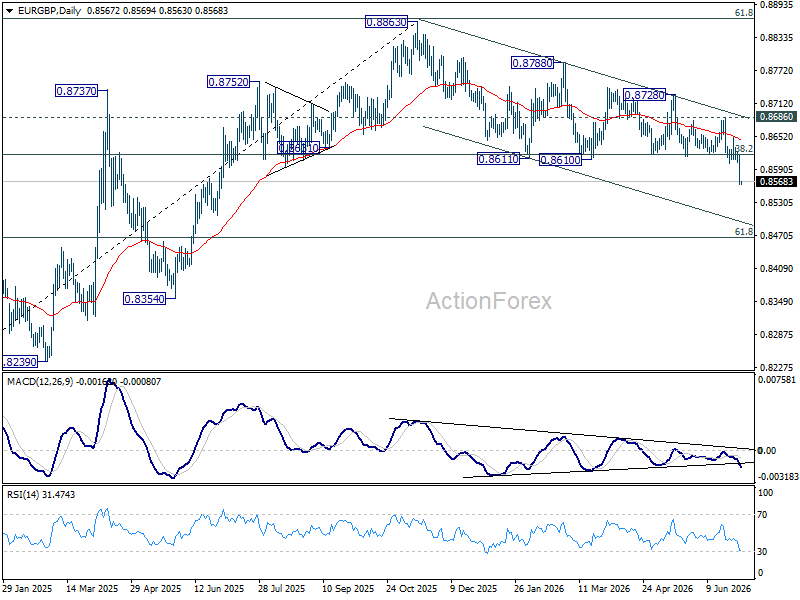

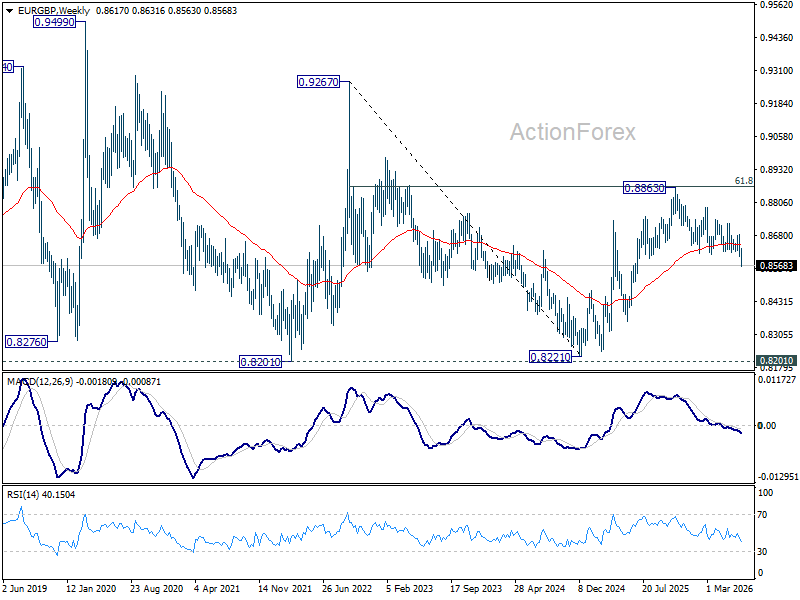

Technically, the latest decline carries much greater significance than a routine break of support. EUR/GBP has decisively fallen below the 38.2% retracement of 0.8221 (2024 low) to 0.8863 (2025 high) at 0.8618, while also slicing through 55 W EMA (now at 0.8645). These breaks came after the cross was firmly rejected by the 61.8% retracement of the broader 0.9267 (2022 high) to 0.8221 decline at 0.8867.

Taken together, these developments suggest the year-long uptrend from the December 2024 low at 0.8221 likely completed at the November 2025 high of 0.8863. As long as 0.8686, now immediate structural resistance, caps any rebound, the outlook should remain firmly tilted to the downside. The next objective is 61.8% retracement of 0.8221 to 0.8863 advance at 0.8466.

A sustained move below that level would strengthen the case that the entire rise from the 2024 low has been unwound, shifting attention toward a retest of 0.8221 over the medium term. Conversely, only a recovery back above 0.8686 would delay the bearish scenario and signal that a period of consolidation is developing instead.

{kind=link}